Last week the European Commission announced it will end Europe’s dependence on Russian oil, natural gas, and coal by 2027. In 2019, Russia provided 29% of the EU’s crude oil imports, 41% of its imported natural gas, and 47% of the EU’s imported coal. Net imports accounted for more than half of the EU’s energy needs.

Domestic crude oil, natural gas, and coal sources are limited within the EU. Some member states (i.e, Malta & Luxembourg) import up to 90% of their energy.

The EU is unlikely to simply switch supplying countries, thus leaving energy supplies outside their control again. However, European manufacturers and service suppliers must all contend with a new set of unknowns. A continuing conflict in Ukraine is bringing changes in supplies of components and raw materials. The war is impacting not only wheat supplies but also Europe’s supplies of computer chips. There are also potential costs in so quickly abandoning fossil fuels.

That said, what companies might benefit from this rapid push away from Russia and toward what must be a greener future?

Europe’s New Green Deal Firmly Back on Track (for Now)

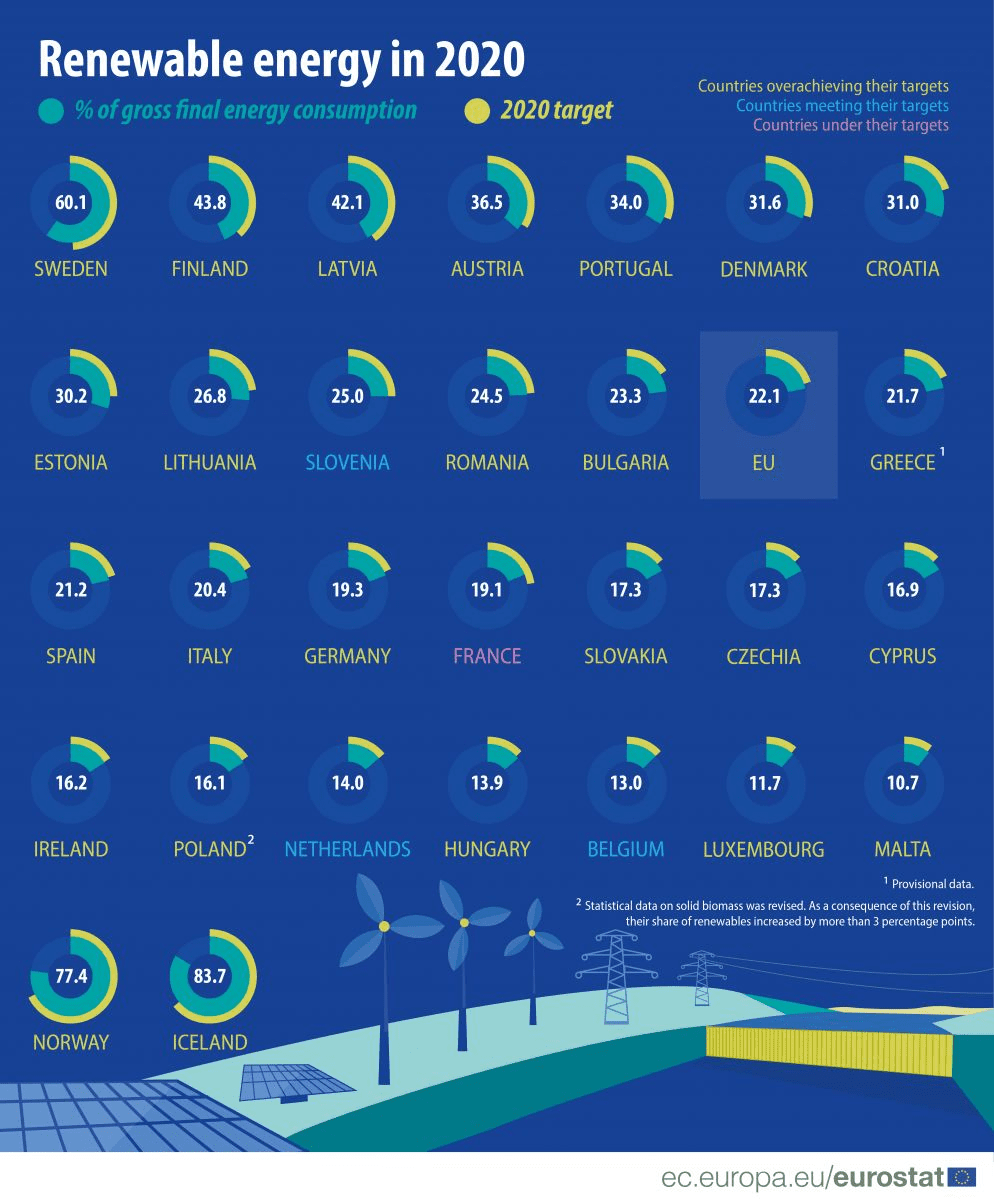

Renewables as percentage of energy by EU member country.

Friday, EU leaders agreed to spend the next two months drafting proposals for weaning Europe from dependency on Russian fossil fuels. Leaders set a deadline of 2027 to make Europe more energy independent. The replacement fuels will come from national and European sources, European Commission President Ursula von der Leyen said. EU climate policy chief, Frans Timmermans, stated that Europe could replace two-thirds Russian gas imports by the end of 2022

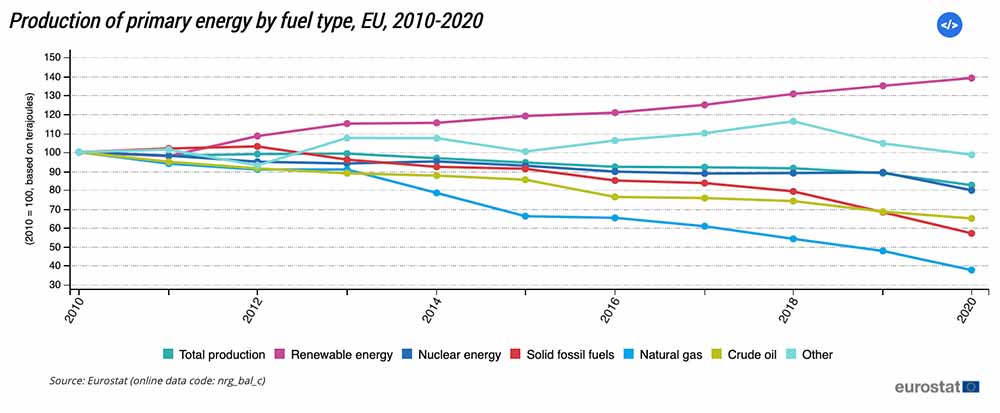

Coal and gas reserves vary wildly from country to country within the European Union. In 2020, EU production of primary energy was down by 17.7% from a decade before and 7.1% lower than in 2019. In the ten years up to 2020, European renewable energy use increased dramatically while uses of other sources declined. The EU’s recently agreed “Green New Deal” aims to make Europe carbon neutral by 2050. It included a €40bn fund to help coal-reliant regions, like Poland, move to cleaner alternatives

Primary energy production in Europe, 2010-2020.

In addition to emphasizing renewable energy, the Green New Deal also mandates a 20% reduction in agricultural fertilizer use. Russia’s invasion of Ukraine has helped send already high fertilizer prices soaring. Global fertilizer producer Yara recently reduced production at plants in Italy and France to 45% of capacity, citing rising gas prices. According to S&P Global Commodity Insights, Dutch natural gas prices have risen 1,100% from a year ago.

Which Companies May May Benefit From These Moves?

The EU’s Green New Deal focuses on transportation, energy production, agriculture sustainability, and improved energy efficiency in buildings. Some companies, like Baywa, work in several sectors that may see increased business because of Europe’s moves away from Russian energy reliance. Companies in energy production and transportation may be most likely to benefit quickly from the energy policy change.

Energy Production

Europe’s moves may not benefit nuclear power development, given rising concerns about potential accidents at Ukraine’s nuclear facilities. Energy companies that could benefit include Brookfield Renewable (NYSE: BEP; TSX: BEP.UN) and Spain’s Iberdrola (OTC: IBDRY), one of the world’s largest renewable energy producers.

Another company that may benefit is Switzerland’s Meyer Burger Technology AG (OTC: MYBUF), which has a focus on solar cells and photovoltaic equipment. Germany’s Baywa (ETR: BYW6) has a focus on agriculture, renewable energy, and construction, all sectors which will be impacted by Europe’s move away from imported fuels. Baywa’s agrovoltaic development center is already working with farmers on pilot projects.

Transportation

Companies providing goods and services to the public transportation sector and those with increasing production of electric vehicles have growth opportunities from this change. Alstom (EPA: ALO), the French company focused on rail infrastructure, recently acquired the rail division of Canada’s Bombardier. A renewed focus on public transportation could improve Alstom’s fortunes.

Many companies that produce electric vehicles already have long waitlists for their cars, SUVs, and trucks. Volkswagen (OTC: VWAGY) is increasing its electric vehicle production substantially in Europe, while also providing the technology for the seven new electric models that Ford (NYSE: F) will introduce in Europe by 2024.

Any of these stocks that might benefit from the EU’s decision to be independent of Russian energy will, of course, be subject to the whims of market movements. They also are dependent on the availability of raw materials and specific components. Battery improvement and production will underpin both energy and transport improvements.

Mercedes’s (OTC: DDAIF) corporate plan has been to produce only electric vehicles by 2030. To that end, the company has recently opened a battery plant in Alabama, while also taking an equity stake in European battery cell manufacturer Automotive Cells Company. Mercedes is partnering with Total Energy and Stellanis (NYSE: STLA), owner of Peugeot, in that venture.

Three commodities that have been in the “dog house” for years are wheat (WEAT), corn (CORN) and soybeans (SOYB). The collapse in grains, of course, has been because of record global grain crops and mostly ideal weather in several countries. These include the Midwest grain belt, Brazil, and Argentina.

Global wheat weather mostly has been ideal. Drought eased rains in Australia three months ago. There also was a big improvement in the important wheat crops in Europe and Ukraine, two of the world’s top exporters.

For corn, Midwest soil moisture is presently ideal. There are no signs of any hot weather that would stress crops for a while.

Soybean prices may get a short term boost in potential exports to China. However, I cannot say by any means that we are going into a major bull market. The trade war with China certainly has been an added heartache for farmers and global grain traders.

The all-grain commodity ETF (DBA) has been in a long tailspin. This started when the 2012 midwest drought resulted in the last true bear market in grains.

Following the herd in trading often does not work

Very often in markets, following the “herd” is not advisable. I am a contrarian by nature. This does not mean, however, that I would blindly give a buy recommendation in corn, wheat, or soybeans just because everyone seems to be short these markets right now (especially corn).

Take the stock market rally in the last couple of weeks. Everyone and their dog (or should I say sheep) was buying. This rally came from ideas that the US economy is re-opening and an apparent bullish job report number last week. However, I have been of the opinion that this was, indeed, “herd mentality.” The world is still in a state of hurt and there is no guarantee that COVID-19 will end anytime soon.

Following the herd in trading is often not advisable. Unfortuneatly, in the case of grains the last few years, it has been.

What will it take to see a Midwest summer grain rally?

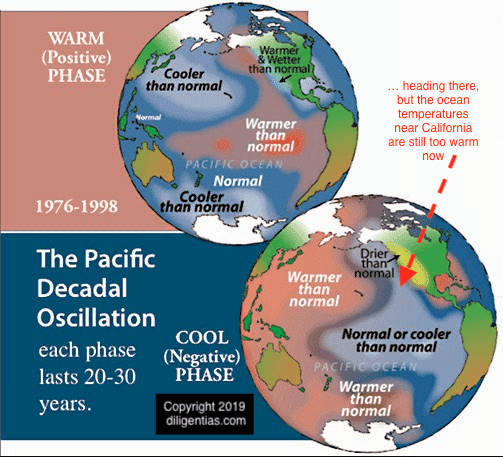

La Nina is presently forming in the Pacific ending the El Nino event. El Nino inspired back-to-back droughts in Australia and incessant snows to the western United States two winters ago (replenishing water supplies). It also brought generally ideal global grain crops. This cooling (La Nina) in the equatorial Pacific can sometimes bring hot weather for Midwest grain crops and for some natural gas regions. However, this weather scenario is much more common when we simultaneously have a negative (cool) Pacific Decadal Index (PDO).

When I say PDO, I’m not talking about prescription drug overdoses or about past due financial obligations. In climatology, PDO refers to Pacific Decadal Oscillation. What does that have to do with commodity markets? Specifically: the Midwest corn belt weather can be adversely impacted by PDO.

We are entering the most important time of the year for the North American domestic corn crop. If you are a farmer, you are trying to figure out how low corn prices may go. Should you hedge at these cheap levels, or is there a chance for a Midwest hot, dry spell? If you are a trader, you are looking for opportunities to ride the coattails of a potential bull market in agricultural commodities. Will there be any?

The Pacific Decadal Oscillation

The Pacific Decadal Oscillation is a pattern of change in the ocean’s climate. The PDO is detected as warm, or cool, surface waters in latitudes above 20 degrees North. During a warm, or positive, phase, the west Pacific becomes cool and part of the eastern ocean warms. During a cool or negative phase, the opposite pattern occurs. It shifts phases on at least an inter-decadal time scale, usually about 20 to 30 years. However, there can be some short term variations in this index that can drive Midwest corn belt weather.

There are several weather criteria that can affect Midwestern grain markets this coming summer. The PDO is a very critical teleconnection. When it is in its negative phase (cool in eastern Pacific near California), this yields the greatest chances for Midwest summer dryness that can hurt crops. There are some signs that the PDO is turning slightly negative, as ocean temperatures east of Asia are warmer than normal. However, we generally have to see the eastern Pacific cool near California to classify the PDO as in its negative phase.

The other climatic teleconnections in the hopper are La Nina (which is slowly forming) and the NAO/AO relationship and what happens with the weakened summer Polar Vortex. The weakened vortex I predicted last December was very responsible or the winter and spring collapse in natural gas prices (UNG).

The Key Point of this article is that buying the commodity ETF (DBA), just because it looks oversold and could be a “bargain hunting” play is not advisable at this point. While being a contrarian can often work in certain markets, unfortunately, following the herd has made the most sense in grains for years. If and when the PDO turns more negative and ocean temperatures cool in the eastern Pacific near California, then the potential may occur for late summer heat and dryness that could lift both natural gas and grains out of the doldrums. Stay tuned at bestweatherinc.com if the PDO goes more negative.

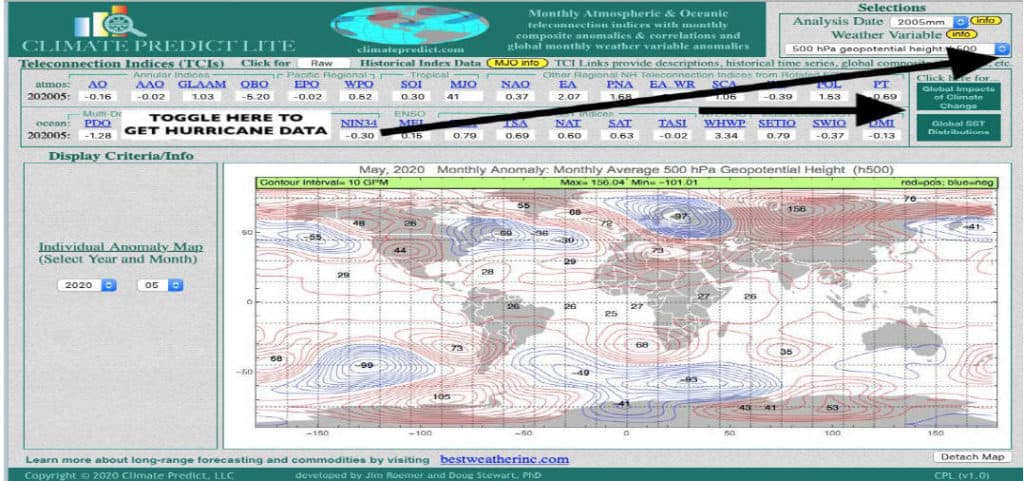

The hurricane season officially began this week and the season’s second storm could be headed toward the Gulf this weekend. What are the reasons for such an early start to the hurricane season? What are the factors that go into making a longer range forecast? How can you have free access to 70 years of historical hurricane data? This report discusses it all.

Much of the information below is quite detailed, but most meteorologists will understand the terms I use.

Anyone can access CLIMATEPREDICT software for free and receive hundreds of color maps showing hurricane tracks, snowfall, and much more. See a description toward the bottom of the page on how to use it.

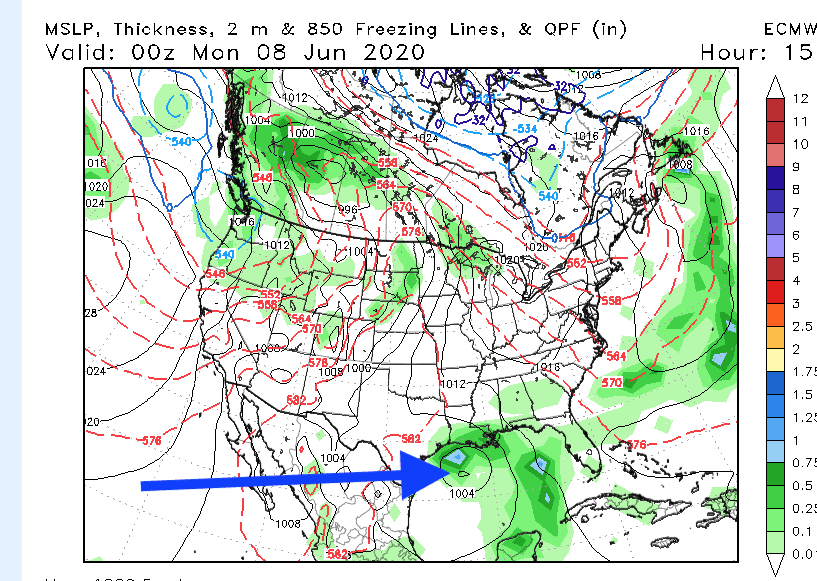

Potential Tropical Storm or Weak Hurricane in the Gulf This Weekend

Cooling ocean waters in the eastern Pacific are tell-tale signs that a weak La Nina may be forming. When the Atlantic is as warm as it is now and the Pacific is cooling, this reduces wind shear and often allows hurricane formation to develop.

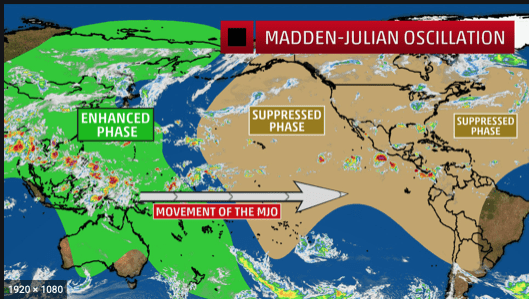

Not all active early starts to the hurricane season are excellent predictors of what may happen during the heart of the season (September/October). Nevertheless, another climatic variable called the Madden Julian Oscillation (MJO) is also in a favorable position for development to occur this weekend.

This weekend’s storm (above) will originate near the Yucatan Peninsula and could be stronger than forecasted because of the MJO.

Here is an interesting video about what the MJO is and how it influences hurricane activity. The MJO is not always in a favorable position to reduce wind shear but will be later this weekend.

Access Historical Hurricane Tracks And Data For FREE

Whether you are a meteorologist, college student studying Atmospheric Science, a commodity trader or just weather enthusiast, you can access FREE historical global ocean temperature data and Atlantic and Gulf hurricane tracks going back to 1948.

Tons of other information related to teleconnections.

We use this data and our proprietary software, ClimatePredict, to forecast the weather. Feel free to try out our lite version.

What Links Teleconnections and Hurricanes?

Teleconnections are recurring, large-scale patterns of pressure and circulation anomalies spanning large geographical areas. They are often responsible for unusual weather anomalies happening at the same time in different areas far apart around the globe.

ClimatePredict.com connects different datasets on factors that impact teleconnections. Understanding teleconnections helps predict hurricanes.

Here are the “short version” instructions for using ClimatePredict.

A) Access historical hurricane information and a database of ocean temperatures from around the world

Click on Global SST (sea surface temperature) distributions to access a huge database of historical ocean temperatures.

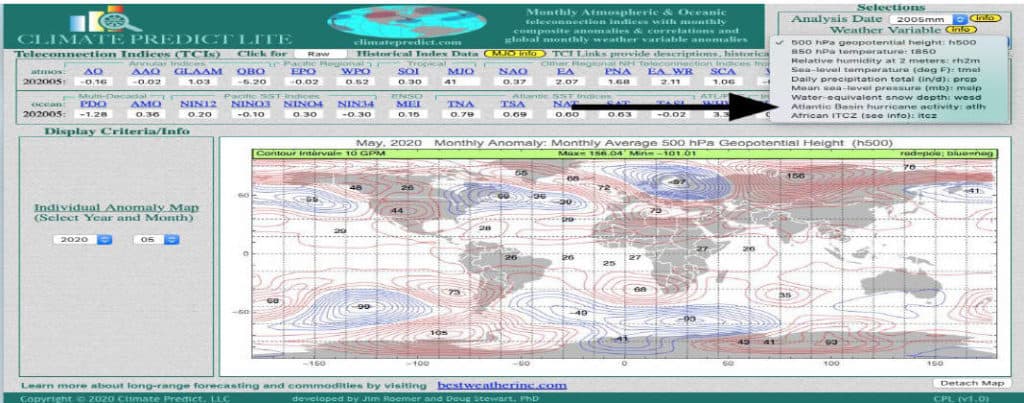

B) Access Historical Hurricane Tracks, ACE Data and More

Toggle to get hurricane data. Set the parameter to “Atlantic Basin Hurricane Activity.”

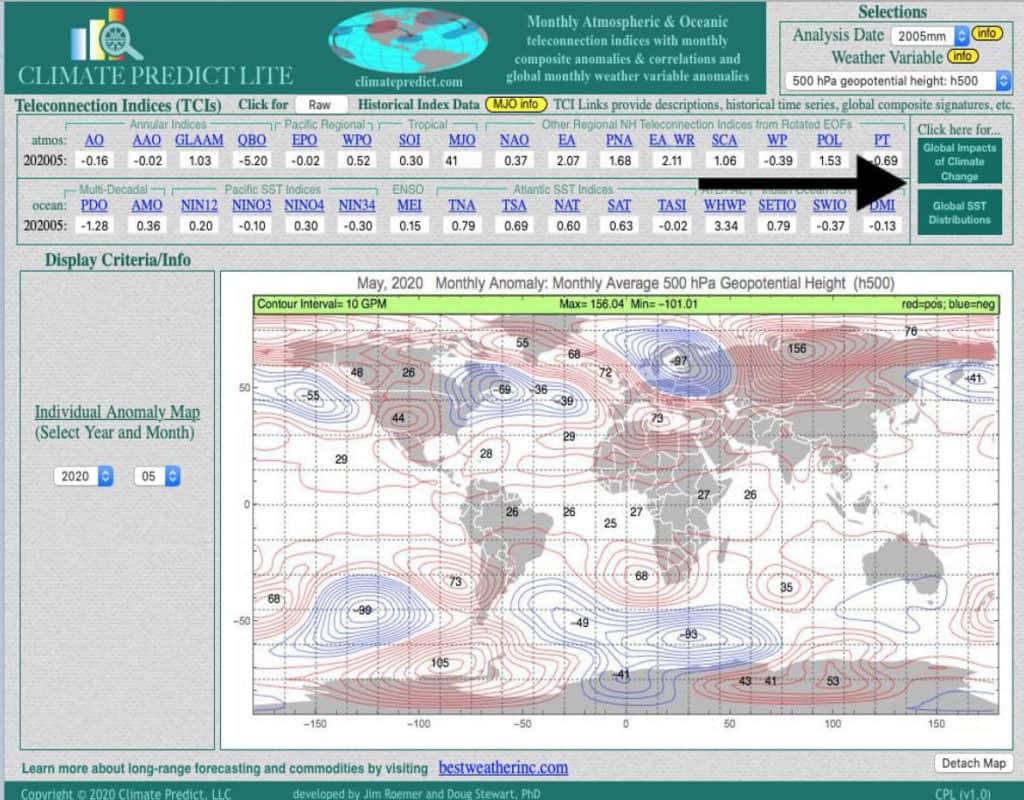

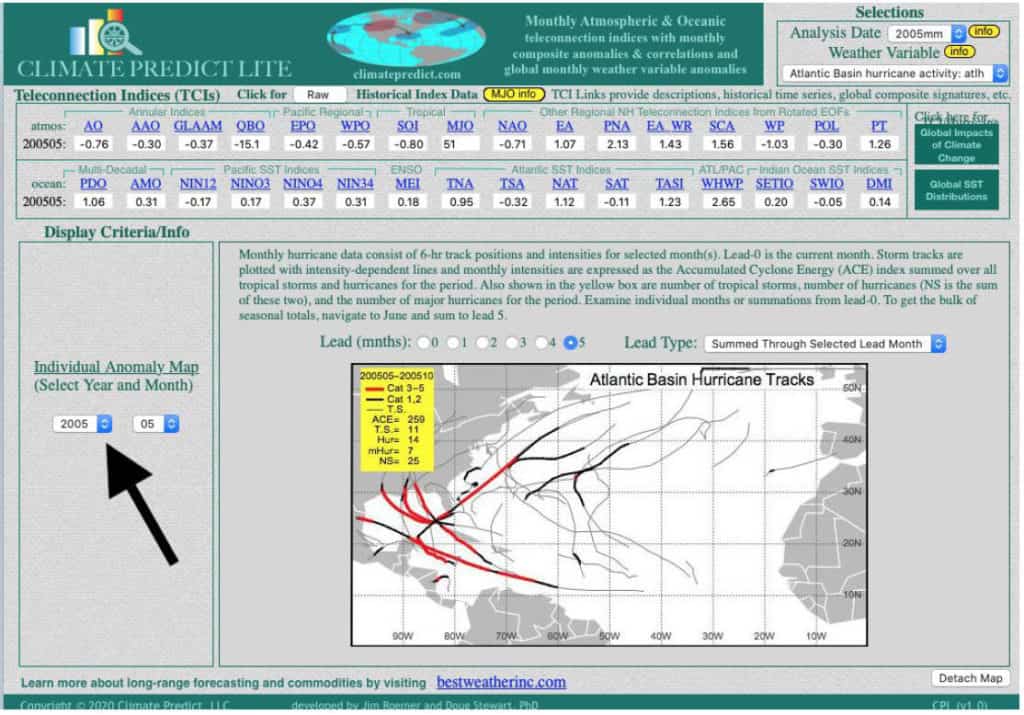

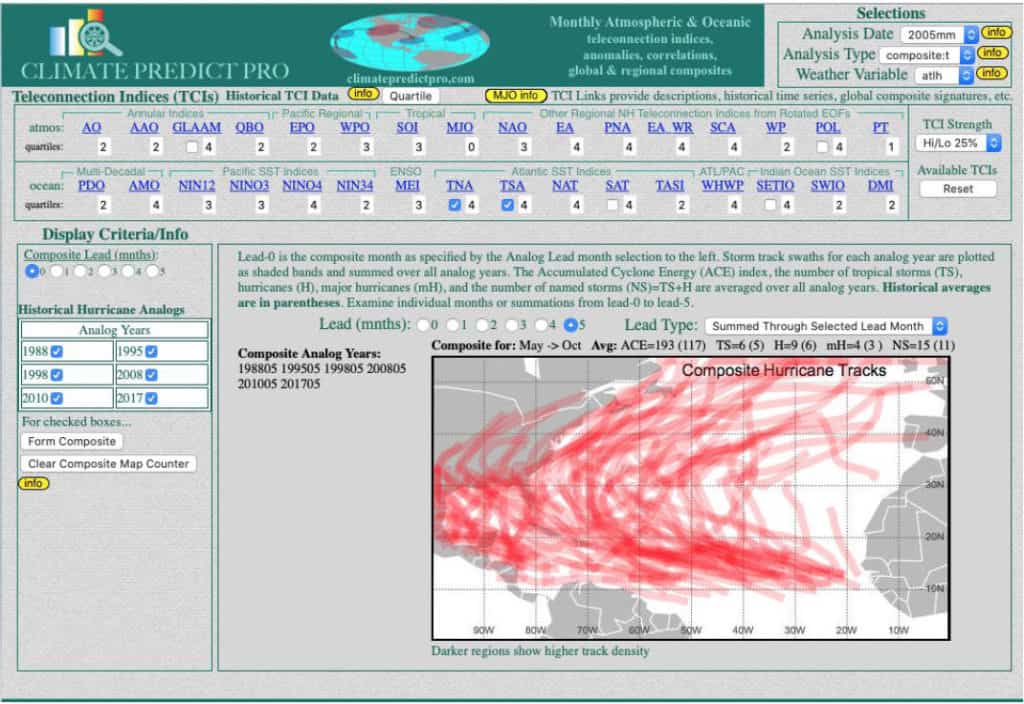

Set the year and month. You can see hurricane tracks, teleconnection relationships, and ACE historical data:

The example above is the Atlantic hurricane season from 2005. You can scroll to 1948. In this case, we are looking at May 2005 teleconnections. The lead time is 5 months (through October) and the “lead type” is ” all hurricanes summed (total)”.

You will see tropical storm, overall hurricane, and major hurricane numbers and cumulative seasonal ACE for that year.

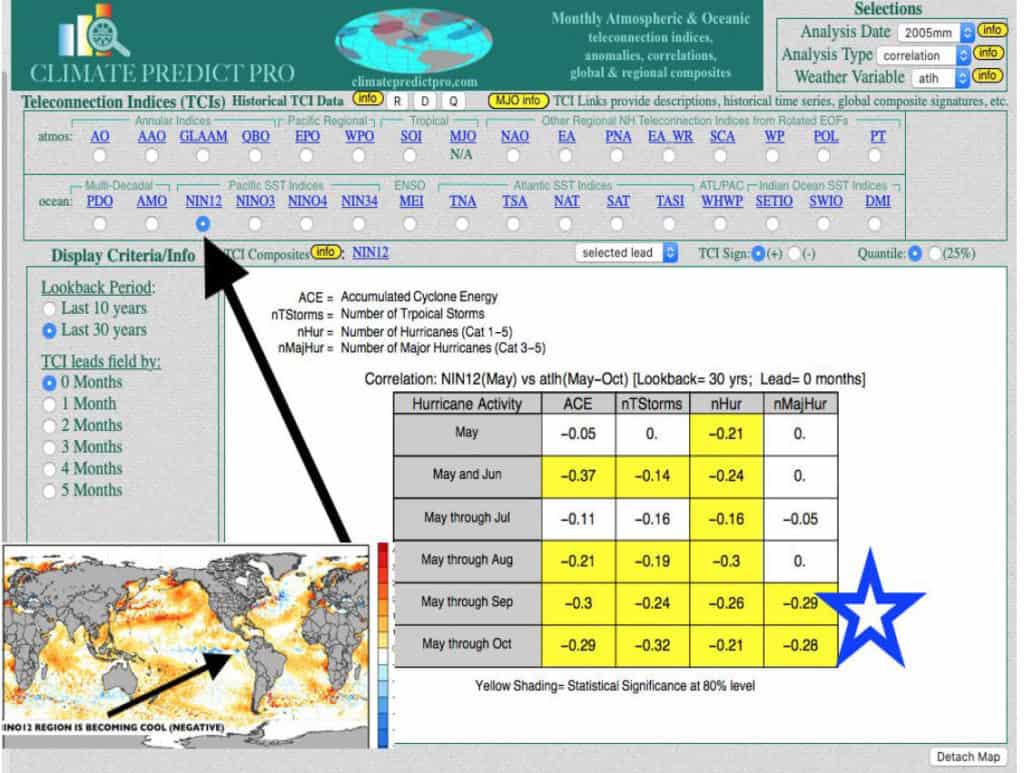

C) Using Teleconnections To Predict Hurricane Tracks and Intensities

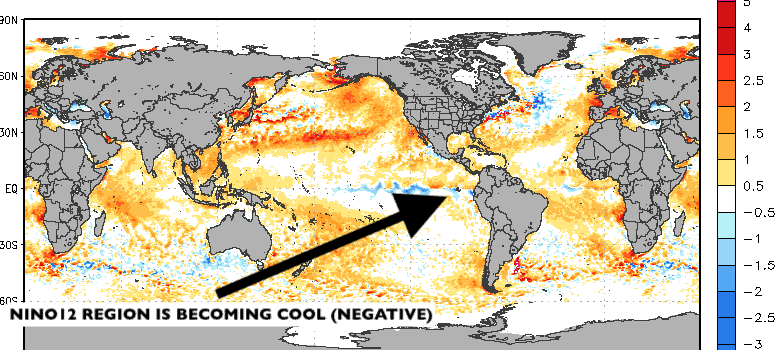

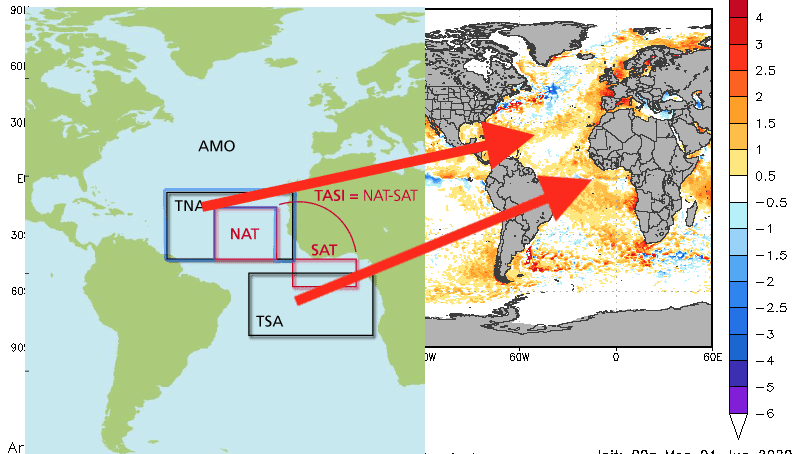

Here we are Looking at cooling at NINO12 in the Pacific and the warm Atlantic.

One of the most important teleconnections (other than Atlantic SST’s) in relation to major hurricanes is the NINO12 region. Notice the negative correlation with hurricane activity and ACE. In other words, cooling (negative NINO12) has a negative correlation with ACE and hurricane activity= + hurricanes, active season, and the strongest correlation of any teleconnection (-.29).

The cooling at NINO12 is critical for there to be an active hurricane season in the Atlantic or Gulf. It reduces wind shear and is a possible precursor to a La Nina.

Shown above is the location of the Tropical North Atlantic (TNA) and Tropical South Atlantic (TSA) ocean temperature regions. The region is generally warm right now, so these values are positive and have will have a positive effect on a potentially active hurricane season later this summer and fall.

D) How to Use Teleconnections to Predict Hurricane activity

Warm TSA/TNA regions in the Atlantic in May suggest these analogs. You can see how the checked boxes appear automatically. They represent all the warm ocean temperatures in the tropical regions since late winter and early spring.

Out of these 2 years (above), 1995 had a very warm previous winter (like this past winter) and many other similar teleconnections, such as a weak El Nino. This could be our best fit analog.

We CHOOSE 1995 and 1998 as the best analogs.This is because these 2 years were most similar with respect to a weakening El Nino. But remember, climate change and warming oceans have to be factored into the equation. These analogs are only a guide.

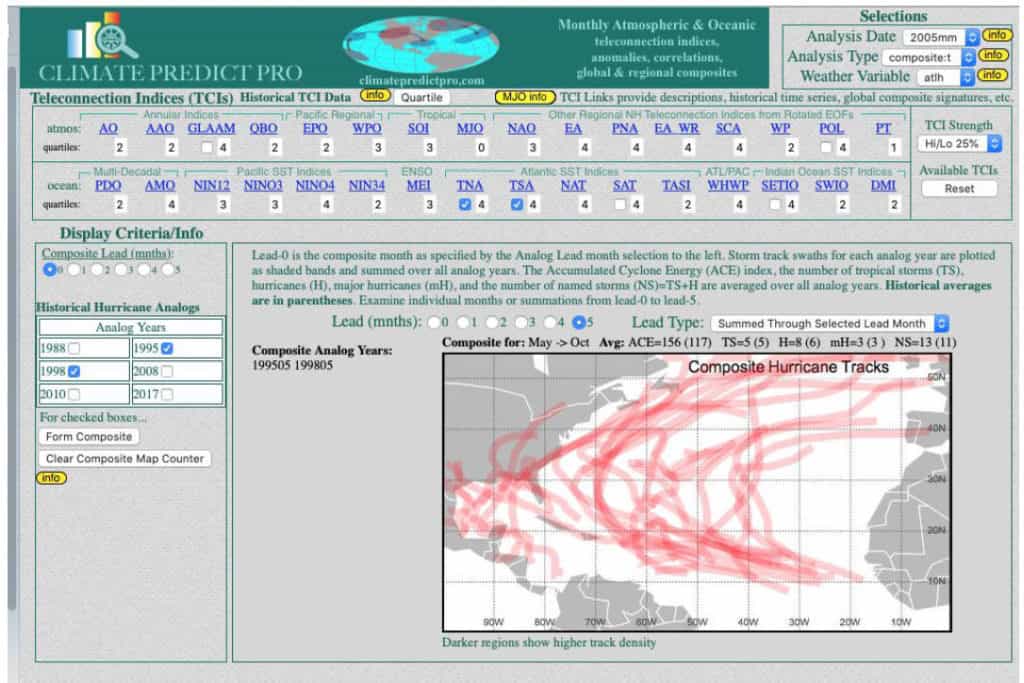

I took the year 1995 as the best possible analog. It was a warm NAO/AO winter with the polar vortex remaining over the North Pole and a weakened El Nino.

E) CONCLUSION: 1995 storms could be a good fit, with at least 19 named storms. 5 were category 4 or 5’s and had high ACE.

The 1995 analog: An active hurricane season likely, ahead

Please remember that analogs are only a guide. Climate change, warming oceans, and a host of other factors influence global weather, climate, and, of course, hurricane activity.

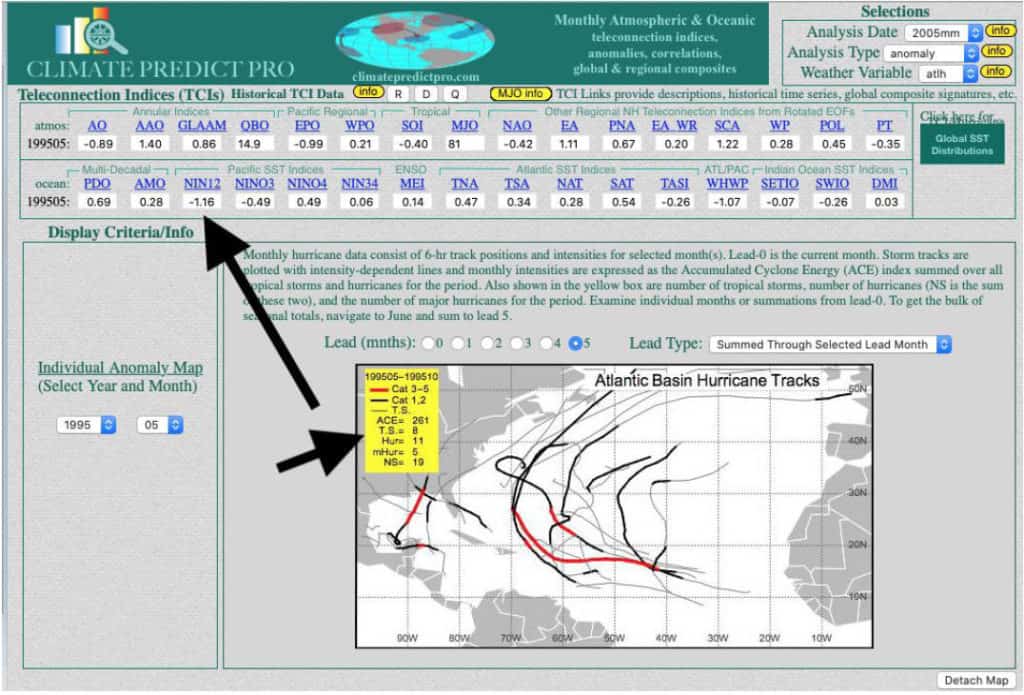

1995 had a previous warm winter and a positive NAO/AO index. It also had a weakening El Nino. Notice how, by the spring, NINO12 was cooling off, as it is now (-1.16 value).

Looking at the 5-month total hurricane activity from May 1995 on Climate Predict (above), one can see the active hurricane season with ACE at 261. There were roughly 18 named storms of which 5 were major hurricanes. One can see the associated hurricane tracks. A couple hit Florida and the Gulf of Mexico, although the majority were out in the Atlantic. This year there is a 261 ACE value. The analogy would suggest that many hurricanes will be of at least category 2-3 status later this summer and fall.

How the 2020 hurricane season could be weaker than normal

It should be pointed out, however, that due to global warming since 1995, the loop current, and other factors, this is only a rough estimate of how active the season could be.

Could the hurricane season be weaker than forecast? After all, many weather forecast firms are predicting an active season and I often “hate” agreeing with the crowd. The hurricane season would be weaker than expected if A) La Nina fails to materialize by the fall and Nino12 regions do not continue to cool off; B) The Atlantic Ocean cools off suddenly, which is very unlikely; or C) Africa dust comes into the Atlantic, which can often disrupt storm formations.

I have received hundreds of requests from around the world for me to start a weekly or monthly long range weather subscription forecast service. This would be “SECOND TO NONE”‘ , given my 35 years experience forecasting for dozens of ski resorts, farmers and some hedge funds and investors. Of course, weather forecasting can be difficult and due to “chaos theory”, “global warming” and “solar activity”, things can change on a dime.

This is why I will be offering such a newsletter in the weeks or months ahead. It will focus on forecasting for many industries from skiing to commodities with some generic trading and investing ideas.

Coming sometime this winter, a new weather newsletter with occasional updates, (WEATHER-WEALTH) So check back frequently for details.

In the meantime, if you email me at subscriptionbestweather@gmail.com I would be happy enough to send you my preliminary winter outlook for 2019-2020.

While many weather forecasters try their hand at these long range predictions, I am lucky enough to also incorporate a special program called CLIMATECH, which I developed with an alum from MIT. It uses teleconnections such as El Nino, ocean temperatures thousands of miles away, what is happening over the North and South Poles, etc. to help make predictions.

IN THIS FREE REPORT I WILL SEND YOU:

*Why late November will feature more cold and snow for the Midwest and East and is putting a floor in natural gas prices and heating oil spreads. What may December be like?

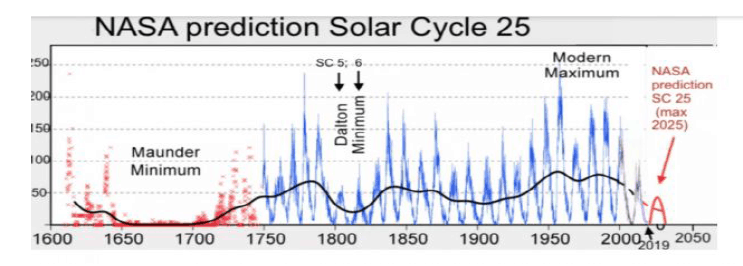

*Low solar activity; El Nino Modoki; Stratospheric Warming; Weather Weirdos, CLIMATECH ™ what this means for winter and the energy markets.

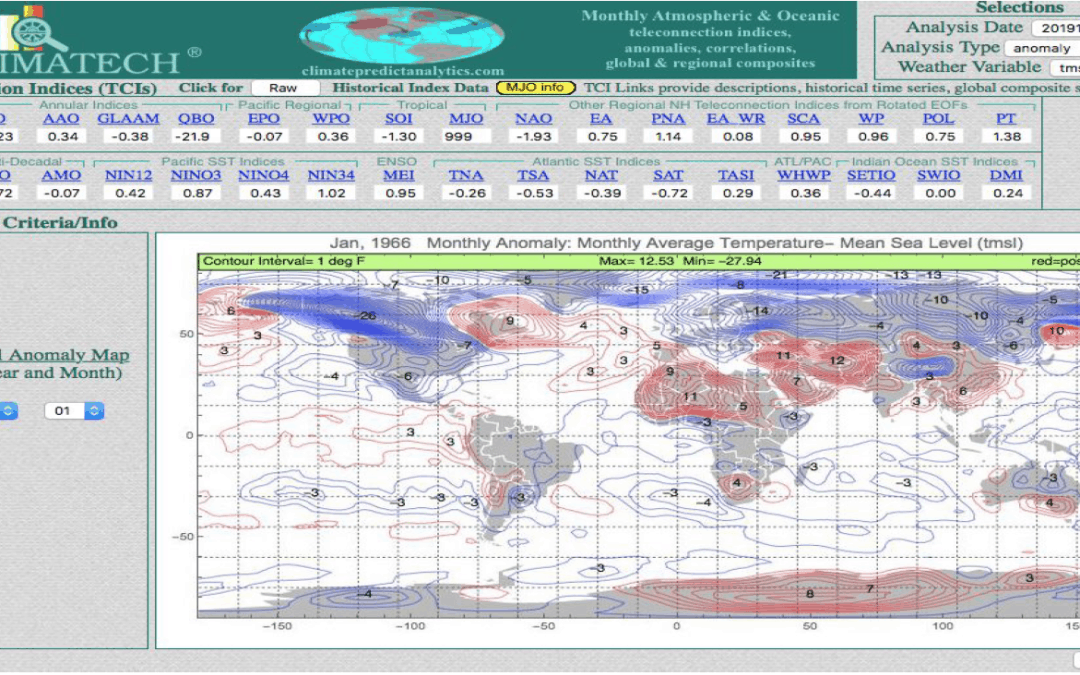

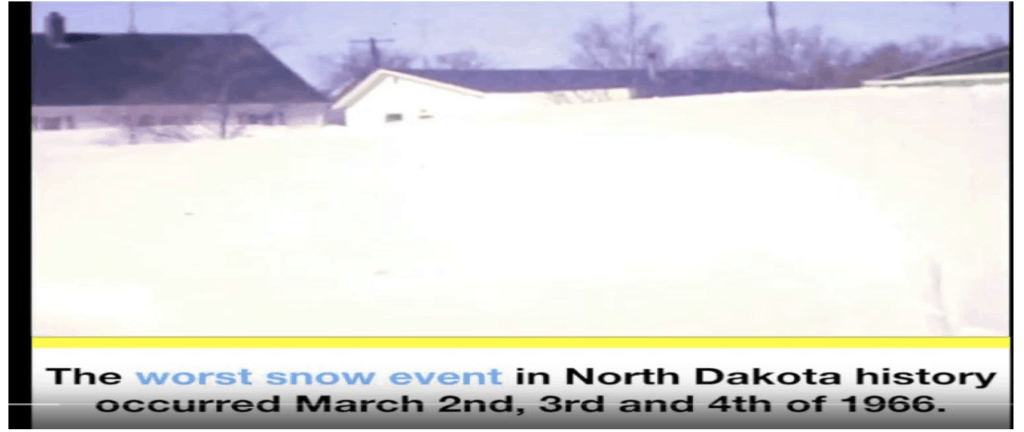

Why does the current global climate support a weather situation similar to 1966 sometime in early to mid 2020? A severe 2nd half of winter in the US.

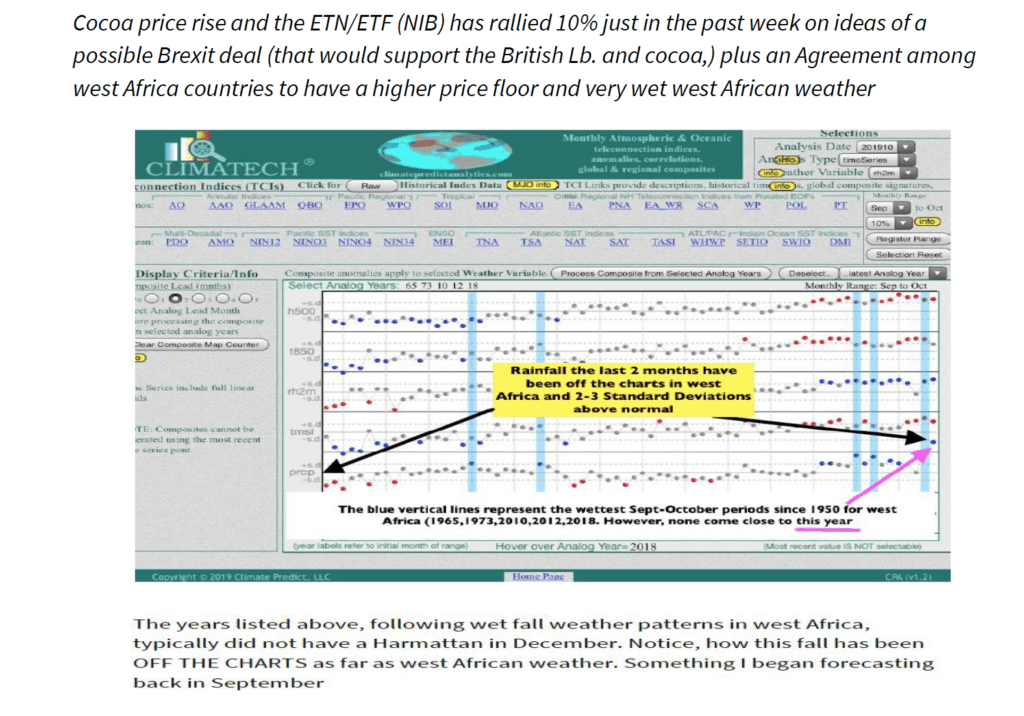

The rally in coffee the last few weeks has been inspired by massive short covering in the face of recent dry Brazil weather and the fact that Brazil producers/hedgers ran out of much of their coffee. Over the last year, a weaker Brazil Real inspired producers to take advantage of what were higher coffee prices in Brazil Real terms, ( priced in dollar, coffee prices fell to 90 cents just a month ago.) In other words, major hedge fund selling and exports helped to pressure the market until recently.

Rains are starting to hit Brazil coffee areas otherwise a massive rally would ensure in coming weeks or months.

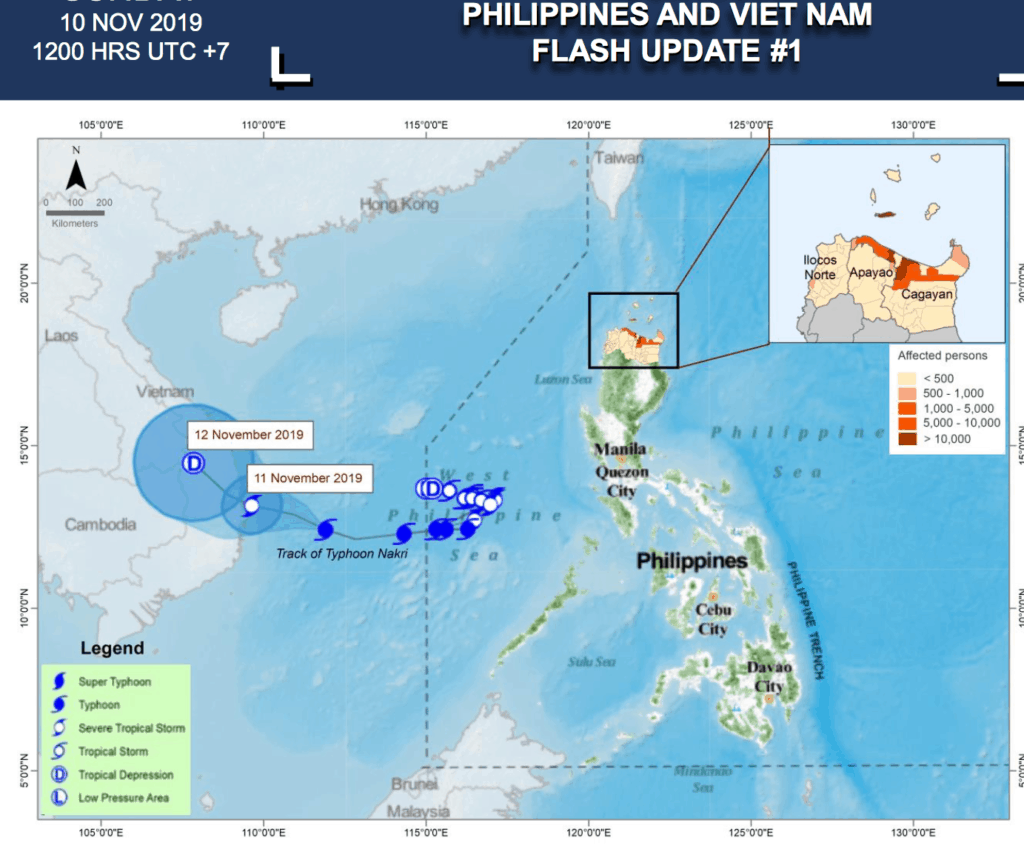

There have been some bullish developments from a weather stand-point–A) Several tropical systems that impacted the beginning of the Vietnam harvest; B) Climate change and a positive Indian Dipole that may pose a threat to the 2020 Indonesia coffee crop. Already, farmers in Indonesia have reported a greater number of fires and some problems could develop if rains do not pick up by the next rainy season this spring; C) A dry-hot October in N. Brazil, which may have nipped some of the developing coffee bloom. (However, critical rains will fall in November)

A tropical system last weekend in Vietnam has delayed the coffee harvest. Traders will be watching weather it drys out or not. This will be an important factor, as well as Indonesia’s 2020 crop to the Robusta coffee market. Robusta coffee is lower quality coffee (instant coffee), which is grown in Indonesia, Philippines and NE, Brazil.

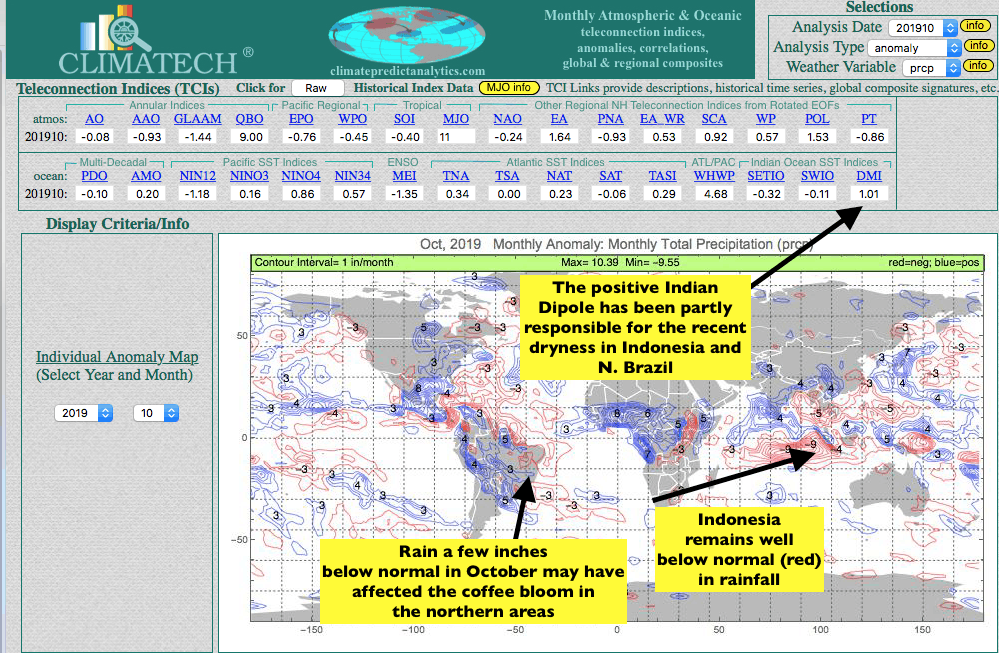

Climatech and global October rainfall trends

In the meantime, Climatech (above), my in house long range weather forecast program, has some interesting and important predictions about the long range for global coffee areas. If you are interested in finding out my feeling of what coffee prices may do in the months ahead and how teleconnections, such as El Nino, La Nina, arctic sea ice and the Indian Dipole will play an important critical role in global coffee weather and other commodities. Please sign up here for occasional free reports.

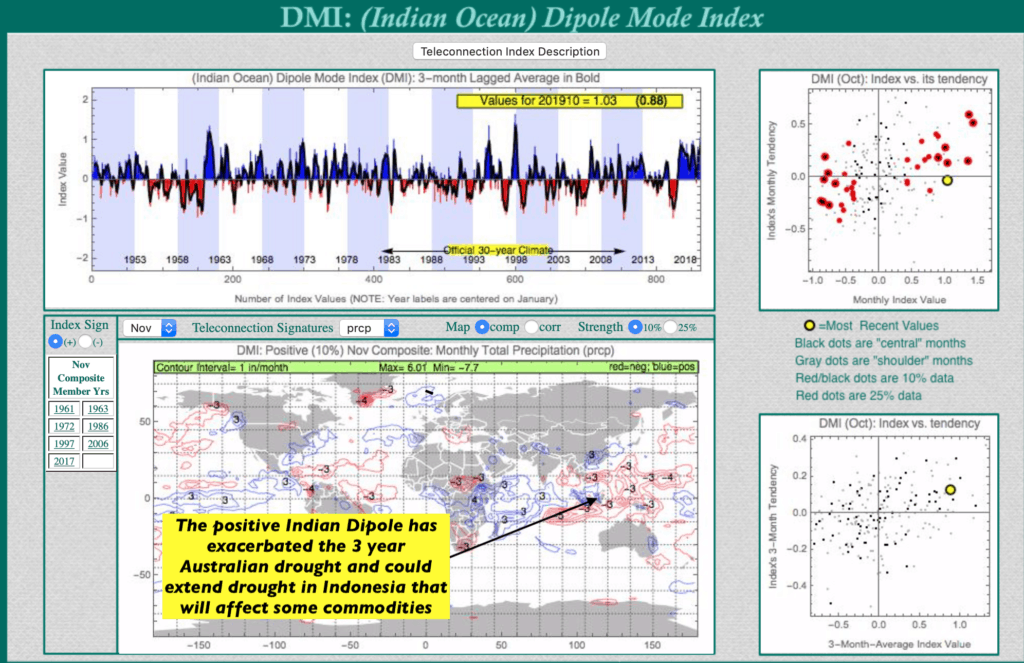

The world’s weather is going haywire right now and there are several reasons to blame this on. First of all, there are some extreme global ocean temperatures with cool waters over Indonesia and warm waters over the Indian Ocean and what we call a near record “positive Indian Dipole”.

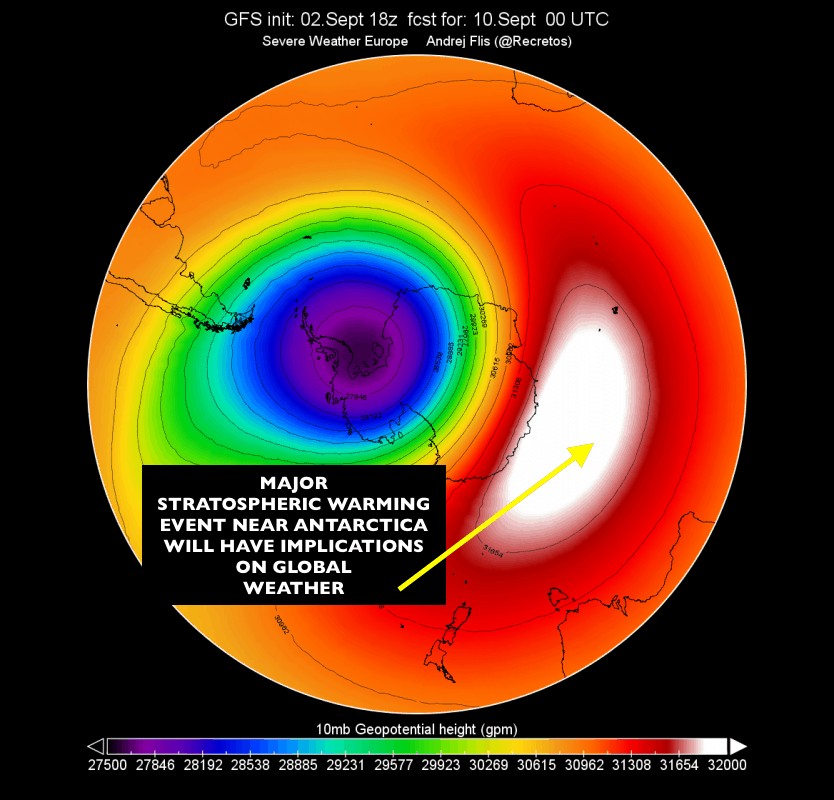

In addition, while El Nino has been pronounced dead, warming in the western Pacific east of Australia still suggests a west based ( El Nino Modoki exists). Combine this with the strongest stratospheric warming event since 2002 (some 50,000 feet above Antarctica) and we are seeing everything from flooding rains in India, to the first big late fall cold blast for U.S natural gas to forest fires out west. Australia’s drought is now in its third year, in which cotton planted will be adversely affected once again and the Aussie wheat crop sees another crop failure. Japan and India are seeing an unusual fall cyclone/typhoon season. See an old article here how the unusual cyclone activity over India caused crop problems and flooding.

The warming oceans are definitely partly due to climate change. I also feel the return of historical fires in California are at least partly to blame from a warming planet.

The stratospheric warming event you see here will have a big impact on South American weather and coffee and grain prices the next few months. This unusual warming, some 10-20 miles above Antarctica could be due, in part, to the lowest solar activity in many years. This causes the AAO index to go negative and the Polar Vortex over Antarctica to move north. However, the AAO index can also have implications on US weather, as my in house program CLIMATECH reveals.

HELPING YOU MAKE THE BEST INVESTMENT DECISIONS BASED ON THE WEATHER

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.OkPrivacy policy