A “monsoon on steroids.” That’s how the UN Secretary-General described the weather bringing the climate-related floods to Pakistan and its crops. Most importantly for international markets, these include cotton and possibly wheat. Since June, over 1,100 people have died and one-seventh of the country’s population has been impacted by floods. The storms damaged around a million houses. Monsoon rains are over 400 per cent heavier than normal in some key agricultural provinces. The most Indus River flood damage is occurring in Sindh province, Pakistan’s second-largest producer of wheat and cotton.

The monsoon’s impact in Sindh province in August 2021 versus August 2022. Source: NASA.

Kharif (Monsoon) Crops Had a Hard Start This Year

Pakistan has two main growing seasons, winter and monsoon, also called kharif. Kharif crops include cotton, rice, sugarcane, and corn, as well as staples like dates, chilis, and onions. The main concern for planting this year’s kharif crops was drought, at first, as 21.6 per cent less rainfall than normal fell nationwide from January to April. High temperatures also plagued Sindh, Balochistan, south Khyber Pakhtunkhwa, and southern Punjab, which, in the main, are the areas now flooded.

Even before the catastrophic floods this monsoon season, drought impacted Sindh province’s agriculture. Sindh Agriculture Extension Department data showed 2022’s wheat production to be 17 per cent below the government’s targeted amount. The government target for cotton planting was 19 per cent higher than Sindh’s actual acreage.

The Monsoon Rains Pummel Cotton

Planning Minister Ahsan Iqbal told Reuters that almost half the country’s cotton crop had been destroyed. While Punjab provides the majority of Pakistan’s cotton crop, the monsoon destroyed almost all of Sindh’s crop.

By August 23rd, the outlook for cotton production in Sindh province already looked grim. “So far there is 45 per cent loss in cotton, 85 per cent loss in dates, and 31 per cent loss in rice in Sindh due to the ongoing monsoon. The standing sugarcane crop has also suffered damage up to 7 per cent due to floods, despite it being a high water-consuming crop, [which shows] the intensity of the disaster we are facing,” said Ali Nawaz Channar, technical director at Sindh’s Agriculture Extension service.

Within days, others estimated that continuing rains increased the losses. “The crop of cotton is almost 90-100 per cent damaged,” said the chair of the Sindh chapter of the Pakistan Businesses Forum. The Chief Minister of Sindh said 90 per cent of the province’s farmers had damaged or completely destroyed crops.

Many Pakistanis Work in Ag; Cotton Drives Pakistan’s Exports

Around 37 per cent of Pakistan’s population works in agriculture, a sector that provides 22.4 per cent of the country’s GDP. Textile products and cotton make up around 60 per cent of the country’s exports. Cotton prices have already risen and Pakistan needs to increase imports to keep its mills spinning in the coming months.

Wheat: Even After Rain Stops, Monsoon’s Damage Will Be Ongoing

“Now there is so much water that no future cultivation can be made. It would be impossible to grow wheat and sugarcane in Oct/Nov,” the Sindh Chamber of Agriculture President told a national newspaper. Predictions are that monsoon waters are unlikely to recede to allow timely wheat planting in October and November in many places. There also will be the need to repair irrigation systems and the more than 20 dams already breached or destroyed. Sindh province is home to the world’s largest barrage-based irrigation system.

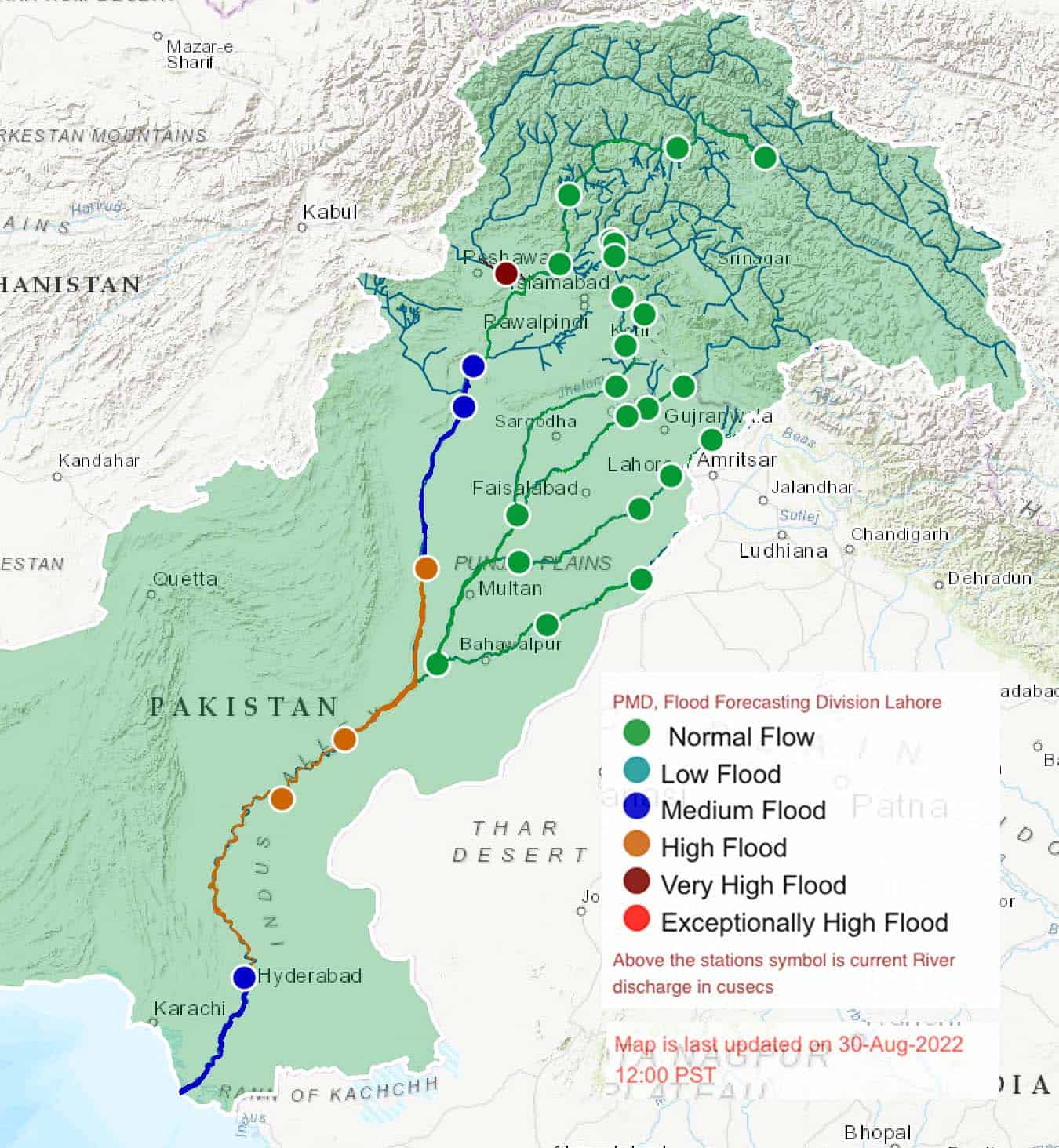

Map of areas flooded by the Indus River 2022. Source: Pakistan Meteorology Department.

Any decline in wheat production will only add to Pakistan’s humanitarian needs. While cotton fuels exports, it is wheat that fuels the country. Wheat makes up 70 per cent of Pakistan’s grain production and it is the country’s main food source. Even before the ravages of the COVID epidemic and the current flooding, approximately 40 per cent of Pakistanis were food insecure.

How Pakistan Got Here and What Comes Next

Many Pakistani commentators online blame the extent of the current crisis on the failure of the country’s government to make strategic infrastructure upgrades after 2010’s devastating flooding.

Pakistan is the 8th most affected country on the Long-Term Climate Risk Index. Increased temperatures and melting glaciers in Pakistan’s northern mountain region are the causes of the monsoon’s heavy rainfall, according to many analysts. The country has over 7,000 glaciers, more than anywhere on the planet outside the Poles. Neither increased global temperatures nor the melting glaciers are likely to end soon.

It’s not like Pakistan doesn’t have enough long-term woes. The IMF this week provided a new tranche to help the country stave off default and to address its ongoing economic crisis. And the heavy monsoon may also be seeding another problem for the country’s agriculture. FAO posits that the unexpected volume of rain may lead to increased locust breeding along both sides of the Indo-Pakistan border.

When the UK’s Met Office made a long-range forecast for British and European weather in 2020, no one foresaw that its extreme 2050 heat forecast would arrive in 2022. Tuesday, the UK recorded its highest temperature ever, 40.2 degrees Centigrade (104.4 F).

Across Europe, temperature records have been broken all week. Over 2,000 people have died in Portugal and Spain alone because of heat and wildfires rage from Turkey to Spain and north to the Arctic Circle. Agriculture is suffering, with corn yields predicted to go down by 30% in Italy and 16% in Spain.

The complete social and economic damage has yet to be calculated for this summer’s wild weather in the Northern Hemisphere but the European Environment Agency estimates that the continent has lost up to $552 billion in the last forty years from extreme weather events.

At a climate summit in Berlin this week, António Guterres, the United Nations Secretary-General, declared, “We have a choice. Collective action or collective suicide.”

WIth European temperatures reaching up to 115 Fahrenheit and London thirty Fahrenheit degrees higher than average, is it any wonder the UN Secretary-General despairs?

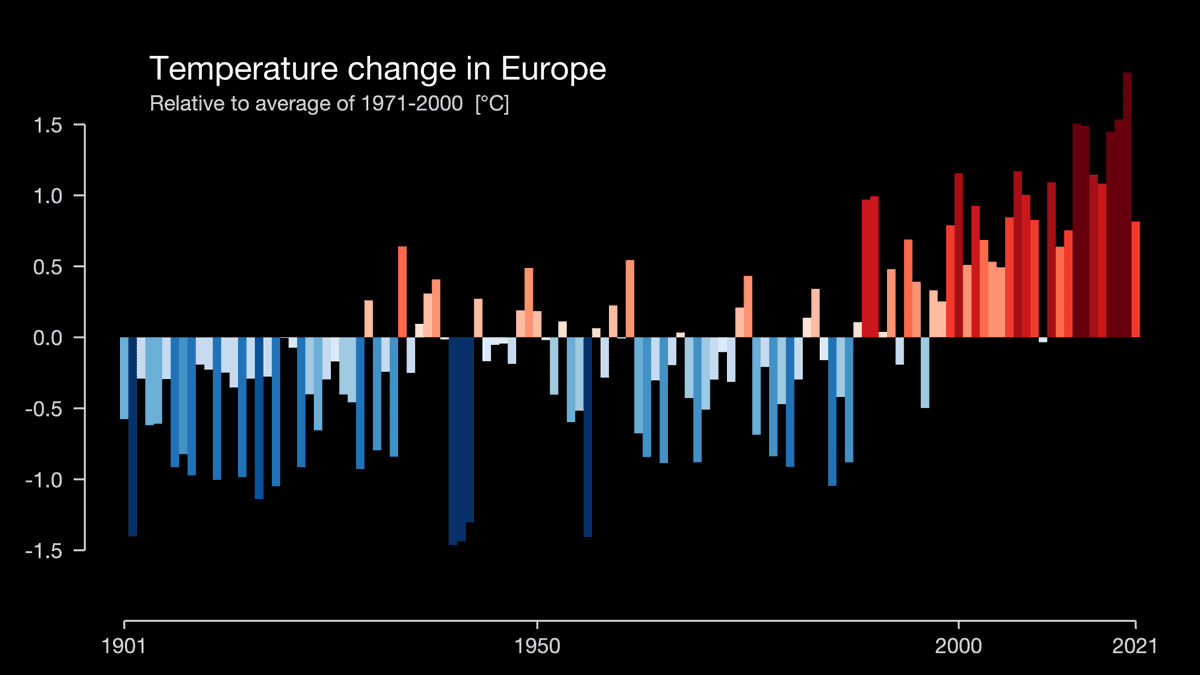

Temperature change in Europe since 1900. Source: UNFCC.

First Cold, Now Heat: Euro Agriculture Has Taken A Big Weather Hit This Year

This is Europe’s second heatwave this year and forecasts call for more. Heat has not been the only concern for European agriculture this year, however. A record-setting cold snap in April came after higher than normal spring temperatures. Late frosts impacted almond and fruit trees in Spain and wine-growing regions in France. Impacts on grain-producing regions in Germany and other countries were small. however.

The current heat wave has led to early harvest in some soft wheat-producing areas. France’s Ministry of Agriculture forecast that 2022 soft wheat production would decline by 7.2% thanks to drought and heat. France is the largest wheat exporter in the European Union and the world’s fourth-largest.

Heat Defeats Italian Farmers, Already in a World of Climate Hurt

Minster of Agriculture Stefano Patuanelli announced last week that as much as 30% of Italian agriculture will be lost this year due to drought and heat. The government declared a heat and drought emergency in five provinces and Italy’s main farm lobby, Coldiretti, estimates that Italian farmers have lost up to US$3 billion.

The Po Valley Drought Is the Worst in 70 Years

In the Po Valley, the heartland of Italy’s rice growing area, heat and drought have decimated crops. The Po Valley includes the provinces of Lombardy, Emilia-Romagna, Friuli Venezia Giulia, and Piedmonte, some of the most productive land in the country. A farmer there estimated that up to 70% of their crops were already gone. Saline water from the sea normally reaches three miles up the Po. This year, it has intruded up to 18 miles inland, damaging crops irrigated with river water.

The Po River is seeing the worst drought in 70 years thanks to reduced winter-spring precipitation and summer heat waves. Source: SciTechDaily. Contains modified Copernicus Sentinel data (2020-22), processed by ESA, CC BY-SA 3.0 IGO.

Over 50% of Europe and UK on Drought Alert or Warnings

Yesterday, the European Commission published its report “Drought in Europe July 2022“, which found that an unprecedented 44% of land in Europe and the UK is at a drought warning stage, with 9% at the alert level. Winter-spring precipitation deficit was up to 22% more than in 2021 and this is stressing vegetation, especially in the south of the continent. Water Europe estimates that 59% of freshwater use in Europe is for agriculture, with a significant amount used to keep agriculture going in parched Southern Europe.

Water Europe also reports that annual renewable freshwater resources per inhabitant decreased across much of Europe during 1990-2017. The greatest decreases were seen in Spain (-65 %), the greenhouse for Europe, and Malta (-54 %).

In Italy, Minister Patuanelli said that the latest government research showed that Italy had lost 19% of its available water resources from 1991-2020 compared to 1921-1950. He added that the coming decades could see further decreases of up to 40%. Coldretti said that northern Italy has seen half the average rainfall for the last few years. To combat this year’s drought, water rationing has been instituted in cities across Italy.

Too Much of Europe is Burning

This summer’s heat waves have lead to record numbers of fires in forest and agriculture areas. The state of Brandenburg in Germany already has experienced over 260 wildfires this year. Forests in Southwest Europe have been hit unusually hard. Across Spain, over 70,000 hectares (173,000 acres) have burned, around twice the average area in a year. Meanwhile, a record number of hectares have burned in France for this time of year; the fire season has not hit its traditional height.

Hectares burned in France in 2022 heat waves compared to previous years. Source: Dr. Serge Zaka, Asso Infoclimat.

What Might Be Causing Europe’s Disasterous Heat and Drought?

A recent study in Nature posited that Western Europe has been a heat wave hotspot for four decades, with heat events increasing in both frequency and intensity. The study found that there was an increased frequency of and intensity when the phenomenon of the upper atmosphere’s jet stream splitting into two occurred. Heat waves would then develop between the two flanks of the jet stream, leading to the rise in European temperatures. What caused this divide was not clear to researchers.

For most of Europe, the extreme weather impacts from climate change are already easily seen, no matter what the cause. “The moment of real climate crisis is 2022,” Rudolfo Laurenti, Deputy Director of the Bonifaca Po Delta Authority, told CNN.

Jim’s latest Market to Market interview covers grain market volatility, the possible future for currently good-looking crops, impacts of the continuing La Nina that few people besides Jim saw, and how beef cow operations are suffering.

He also touches on Brazil’s possible future weather for the rest of the year versus the Midwest’s outlook. What are the odds for an early Midwest frost and what can bring great weather for Midwest farmers next year? Why are crop yields hitting trendlines despite weather problems like 2020s Midwest derecho?

Over the course of three days this week, unprecedented rains and early snowmelt combined to close Yellowstone National Park and change its landscape forever. Rivers in Montana, Idaho, and Wyoming burst their banks.

The Park’s worst flood before those three days occurred in 1978. Experts called it a 1 in 100 years event. The US Geological Survey considered this month’s flooding to be a 1 in 500 years event.

Some forecasts see more precipitation in Yellowstone this weekend. Park administrators say they are watching the weather closely but park plans to rebuild ruined infrastructure are already underway. This time, however, they will take into account climate change.

The National Park sits in the middle of the Greater Yellowstone ecosystem, which runs from the Canadian border to Wyoming. Source: National Park Service.

The Greater Yellowstone Area includes parts of six major rivers: the Missouri, Upper Yellowstone, Big Horn, Upper Green, Snake Headwaters, and Upper Snake. It is one of the few remaining large and nearly intact temperate ecosystems on Earth. As the 2021 Greater Yellowstone Climate Assessment (GYCA) noted, climate change impacts on the area often push the bounds of historical trends. What happens in this area also impacts agricultural areas in the Northern High Plains.

Yellowstone Faces Major Climate Challenges

The 2021 GYCA predicted significant changes in precipitation timing and type. More spring rain and less winter snow are foreseen. Precipitation for June 2022 is already over 400% of normal in parts of the Yellowstone area.

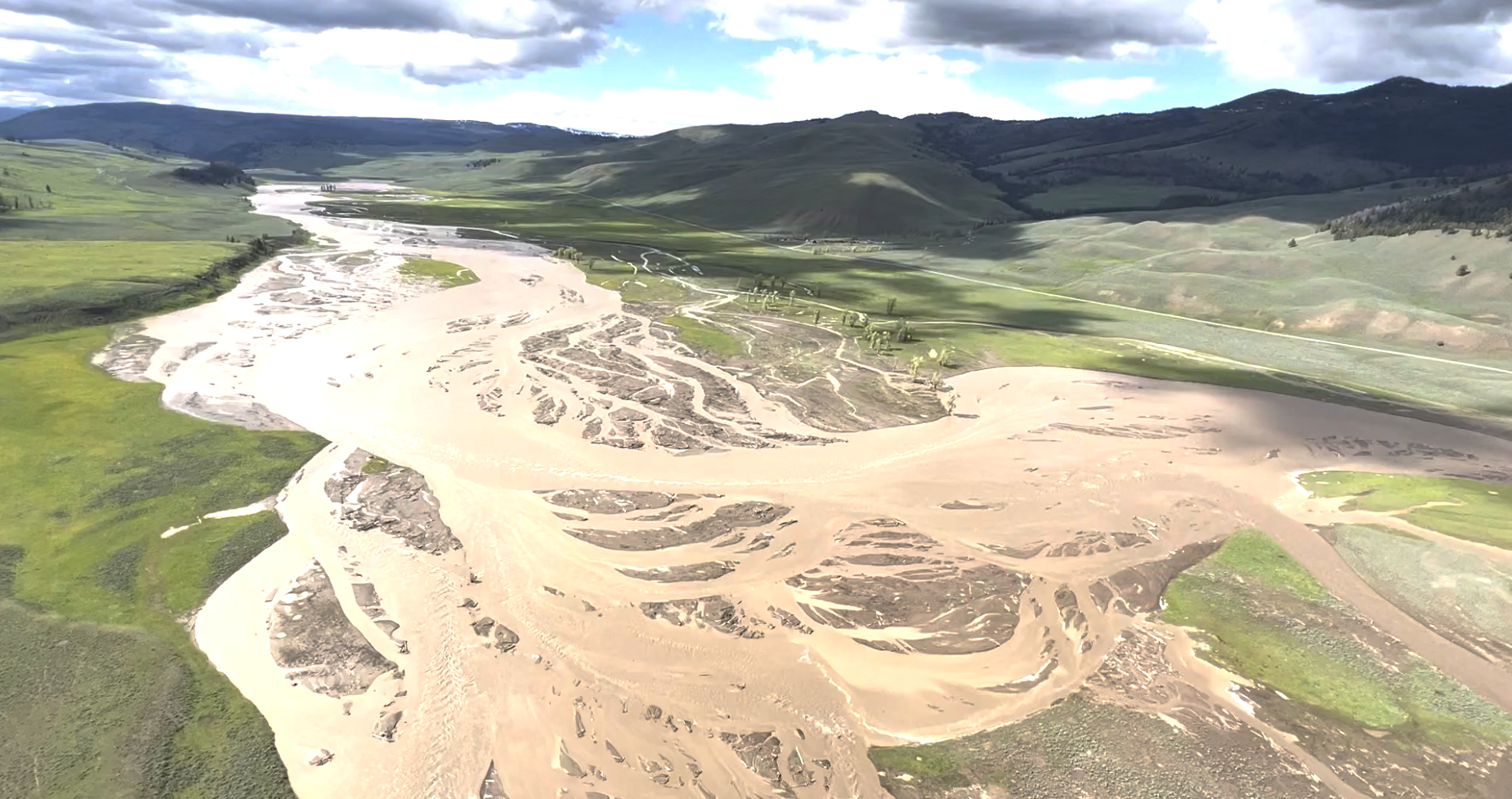

Flooded Lamar River in Yellowstone National Park. Source: National Park Service.

The timing of peak streamflows have already changed. Water amounts have not changed significantly in most of the area but there have been increases in the Yellowstone, Gallatin, and Madison rivers. All are tributaries of the Missouri River.

The GYCA showed peak flows have shifted 1 to 15 days earlier, lengthening the hot season when water is limited. In some areas, spring flows have increased by 30 to 80 percent. For other areas, minimum flows have declined by 10 to 40 percent in the summer and winter.

In the Greater Yellowstone Area, potential evapotranspiration is less than precipitation on an annual basis. At lower elevations in summer, the reverse is true. This brings an increasing seasonal water deficit.

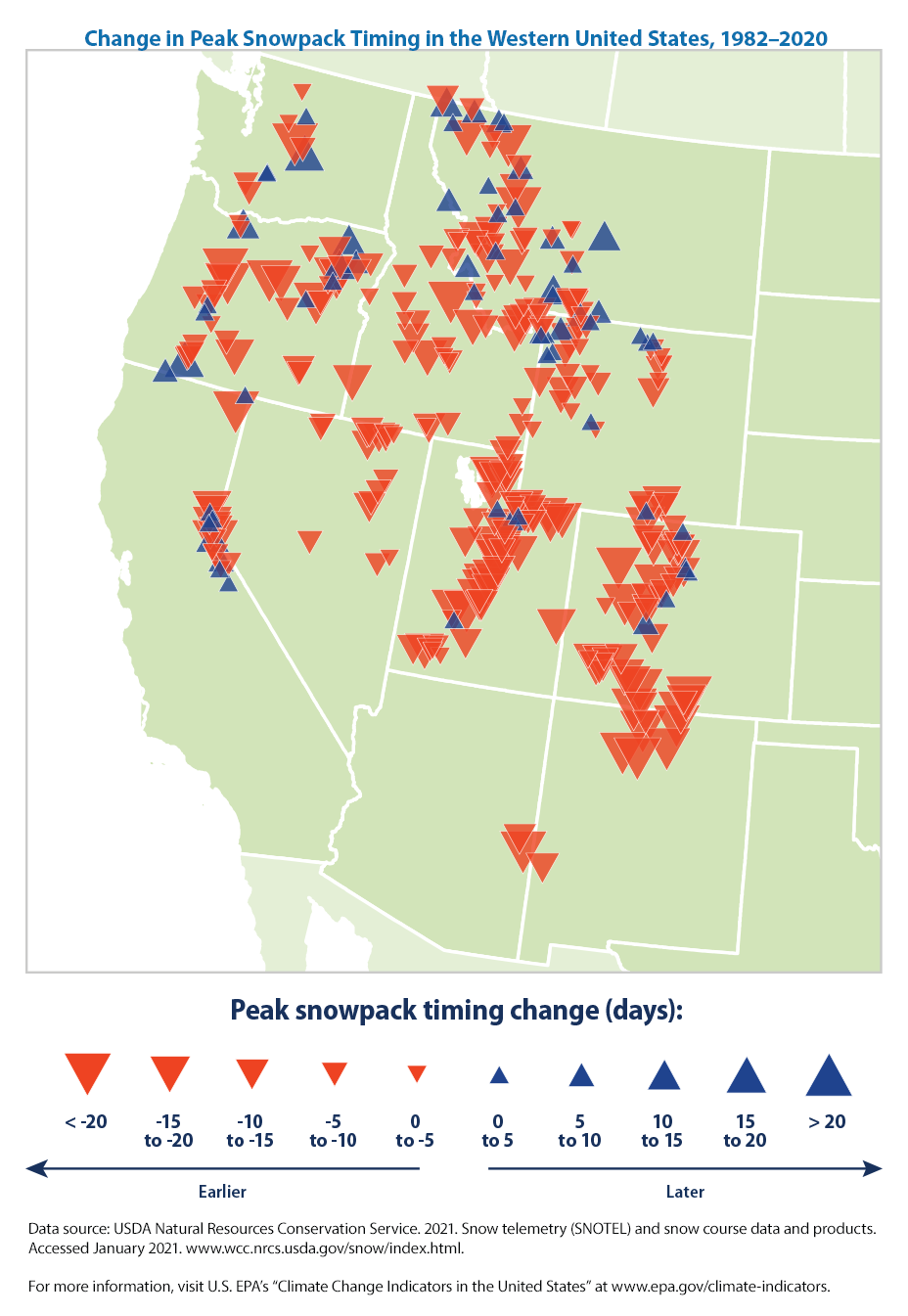

Snowpack Issues Are at the Heart of Water Flow Issues

Warming winters are bringing earlier snowmelt and a loss of snowpack across the West, including in Yellowstone. Warmer winters bring a longer growing season because of longer summers but reduce water availability. They also increase fire risks. Both snowpack and soil moisture impact stream flow. The amount of annual streamflow can vary by up to 300 percent between years because of all these factors.

With Headwaters in Yellowstone, the Missouri River Feeds Plains Agriculture

Yellowstone area climate change impacts the Missouri River headwaters and its tributaries. Some studies indicate that rainfall and water access are already changing in the Northern Great Plains and Central Midwest due to agricultural intensification. Models in the Fourth National Climate Assessment saw annual decreases of 30 days or more in the number of days with temperatures under 28 degrees by 2050. This would have serious implications for the region’s snowpack, streamflow, and water use.

Missouri River basin. Source: Army Corps of Engineers.

Parts of the Northern Great Plains are among the most arid in the United States. Because they are far from the coasts, the Northern Great Plains’ climate is not modulated by the oceans. Extreme drought or extreme flooding tends to happen every ten years or so. With less than ten percent of regional precipitation reaching the Missouri River, large changes in flooding can be brought about by small changes in precipitation. A good example of the region’s unpredictable weather is the severe flooding of 2011. It was followed by a drought in 2012.

The Northern Great Plains

Northern Great Plains. Source: Fourth National Climate Assessment, U.S. Global Change Research Program.

Yellowstone’s Changes Has Similarities/Differences to Dust Bowl Weather

Changes in peak streamflow timing since 1970 look similar to the peak timing during the 1930s Dust Bowl drought but the difference is that a year-round decline in precipitation caused the Dust Bowl. As the Greater Yellowstone Climate Assessment points out, the recent change in peak streamflow times is caused by spring temperatures rising sooner. Earlier spring warmth causes earlier snow melting.

Last week the European Commission announced it will end Europe’s dependence on Russian oil, natural gas, and coal by 2027. In 2019, Russia provided 29% of the EU’s crude oil imports, 41% of its imported natural gas, and 47% of the EU’s imported coal. Net imports accounted for more than half of the EU’s energy needs.

Domestic crude oil, natural gas, and coal sources are limited within the EU. Some member states (i.e, Malta & Luxembourg) import up to 90% of their energy.

The EU is unlikely to simply switch supplying countries, thus leaving energy supplies outside their control again. However, European manufacturers and service suppliers must all contend with a new set of unknowns. A continuing conflict in Ukraine is bringing changes in supplies of components and raw materials. The war is impacting not only wheat supplies but also Europe’s supplies of computer chips. There are also potential costs in so quickly abandoning fossil fuels.

That said, what companies might benefit from this rapid push away from Russia and toward what must be a greener future?

Europe’s New Green Deal Firmly Back on Track (for Now)

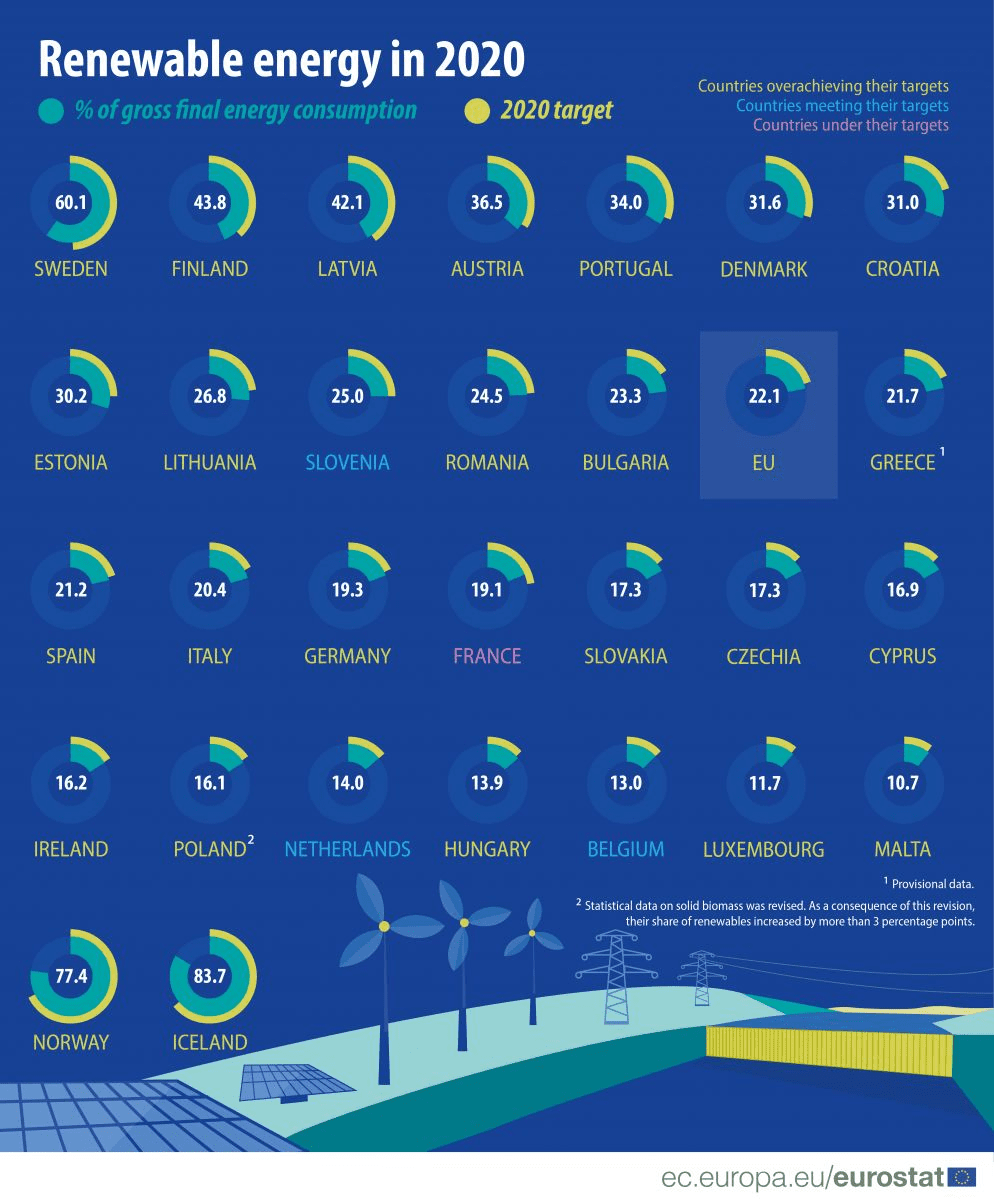

Renewables as percentage of energy by EU member country.

Friday, EU leaders agreed to spend the next two months drafting proposals for weaning Europe from dependency on Russian fossil fuels. Leaders set a deadline of 2027 to make Europe more energy independent. The replacement fuels will come from national and European sources, European Commission President Ursula von der Leyen said. EU climate policy chief, Frans Timmermans, stated that Europe could replace two-thirds Russian gas imports by the end of 2022

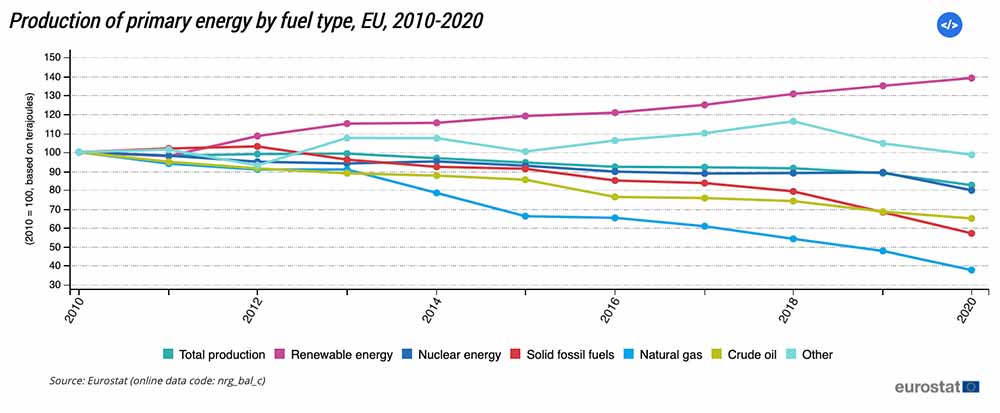

Coal and gas reserves vary wildly from country to country within the European Union. In 2020, EU production of primary energy was down by 17.7% from a decade before and 7.1% lower than in 2019. In the ten years up to 2020, European renewable energy use increased dramatically while uses of other sources declined. The EU’s recently agreed “Green New Deal” aims to make Europe carbon neutral by 2050. It included a €40bn fund to help coal-reliant regions, like Poland, move to cleaner alternatives

Primary energy production in Europe, 2010-2020.

In addition to emphasizing renewable energy, the Green New Deal also mandates a 20% reduction in agricultural fertilizer use. Russia’s invasion of Ukraine has helped send already high fertilizer prices soaring. Global fertilizer producer Yara recently reduced production at plants in Italy and France to 45% of capacity, citing rising gas prices. According to S&P Global Commodity Insights, Dutch natural gas prices have risen 1,100% from a year ago.

Which Companies May May Benefit From These Moves?

The EU’s Green New Deal focuses on transportation, energy production, agriculture sustainability, and improved energy efficiency in buildings. Some companies, like Baywa, work in several sectors that may see increased business because of Europe’s moves away from Russian energy reliance. Companies in energy production and transportation may be most likely to benefit quickly from the energy policy change.

Energy Production

Europe’s moves may not benefit nuclear power development, given rising concerns about potential accidents at Ukraine’s nuclear facilities. Energy companies that could benefit include Brookfield Renewable (NYSE: BEP; TSX: BEP.UN) and Spain’s Iberdrola (OTC: IBDRY), one of the world’s largest renewable energy producers.

Another company that may benefit is Switzerland’s Meyer Burger Technology AG (OTC: MYBUF), which has a focus on solar cells and photovoltaic equipment. Germany’s Baywa (ETR: BYW6) has a focus on agriculture, renewable energy, and construction, all sectors which will be impacted by Europe’s move away from imported fuels. Baywa’s agrovoltaic development center is already working with farmers on pilot projects.

Transportation

Companies providing goods and services to the public transportation sector and those with increasing production of electric vehicles have growth opportunities from this change. Alstom (EPA: ALO), the French company focused on rail infrastructure, recently acquired the rail division of Canada’s Bombardier. A renewed focus on public transportation could improve Alstom’s fortunes.

Many companies that produce electric vehicles already have long waitlists for their cars, SUVs, and trucks. Volkswagen (OTC: VWAGY) is increasing its electric vehicle production substantially in Europe, while also providing the technology for the seven new electric models that Ford (NYSE: F) will introduce in Europe by 2024.

Any of these stocks that might benefit from the EU’s decision to be independent of Russian energy will, of course, be subject to the whims of market movements. They also are dependent on the availability of raw materials and specific components. Battery improvement and production will underpin both energy and transport improvements.

Mercedes’s (OTC: DDAIF) corporate plan has been to produce only electric vehicles by 2030. To that end, the company has recently opened a battery plant in Alabama, while also taking an equity stake in European battery cell manufacturer Automotive Cells Company. Mercedes is partnering with Total Energy and Stellanis (NYSE: STLA), owner of Peugeot, in that venture.

HELPING YOU MAKE THE BEST INVESTMENT DECISIONS BASED ON THE WEATHER

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.OkPrivacy policy