Over the last 40 years, China’s sea levels have risen faster than the global average. In December, Premier Xi Jinping declared that the production of staples such as rice was a natural security issue.

China’s coastline is facing rising tides, so 2021’s production of 4.6 metric tons of “seawater rice” per acre must have pleased Chinese leaders. Earlier, China’s Minister of Agriculture had pronounced that the country would stabilize corn production and expand soybean production in 2022. After trade disruptions due to COVID, domestic agriculture production has a renewed policy focus in China.

A Surfeit of People, a Lack of Arable Land

China is home to around 20% of the world’s population but has only about 7% of the globe’s arable land. Crop-growing land in the country (currently around 120 million hectares) decreased by about 6% between 2009 and 2019. This was due to pollution and urbanization. Around 100 million hectares of China’s land are unusable due to salinity and alkaline issues. Chinese agronomists hope to turn 6-7 million of those hectares into “seawater rice” producing land by the end of the next decade. While not meeting China’s average of 6.5 tons of rice production per hectare, it would still boost domestic food supplies.

Terraced Rice fields in Yunan, China. Photo courtesy of Jialiang Gao, www.peace-on-earth.org.

Will Seawater Rice Impact Chinese Imports Soon?

With seawater rice growing in its early stages, Chinese imports of rice boomed in January-August 2021, with a record 3.2 million tons of rice imported. Half of this was broken rice, which is used for feed, snack, and liquor production.

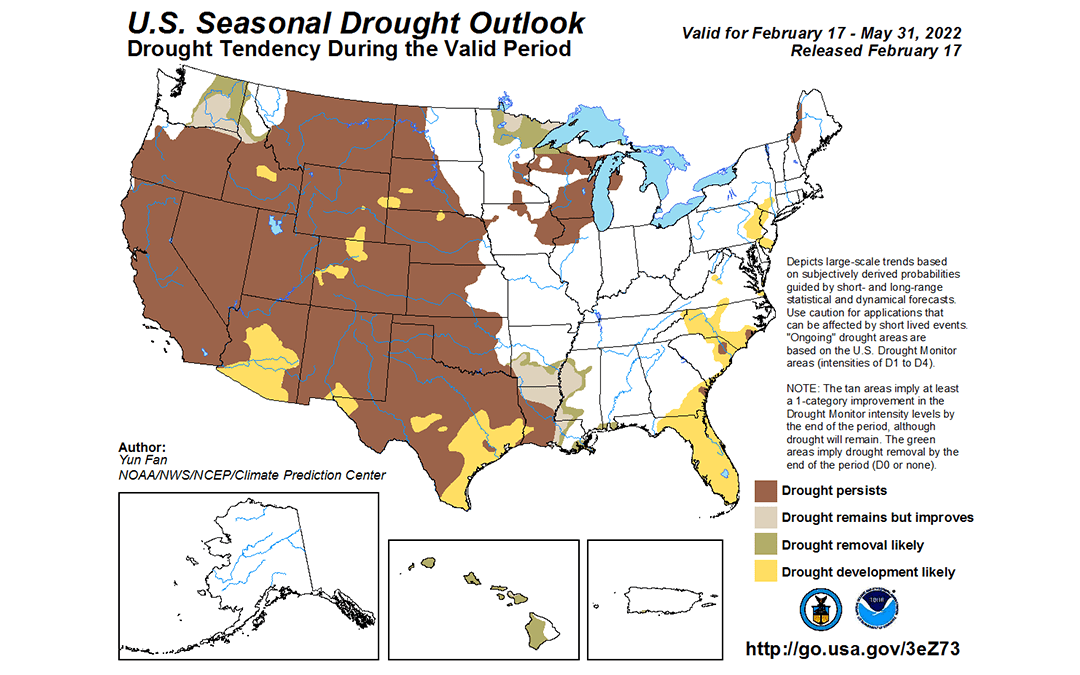

A drought in the western United States looks likely to continue through May, according to the outlook from the U.S. Drought Monitor. As of February 15, 2022, abnormally dry or drought conditions exist in 57% of the lower 48 states.

Researchers found that the 22 year drought period between 2000 and 2021 was the driest since 800 C.E., according to a study published this week at Nature.com. Anthropogenic (human-made) climate trends accounted for 42% of the southwestern North America soil moisture decrease in 2000–2021.

La Nina conditions have impacted snowfalls in the Canadian and U.S. Rocky Mountains and there are already concerns over water for irrigation and other needs in California, Colorado, and other areas. The Bureau of Reclamation’s February forecast predicts that the April-July runoff for the North Platte project will be only 80% of the 30-year average. As a result, the Bureau does not expect water allocations to be released to its contractors. The North Platte project feeds full irrigation to 226,000 acres and provides supplemental irrigation to 109,000 acres in Wyoming and Nebraska.

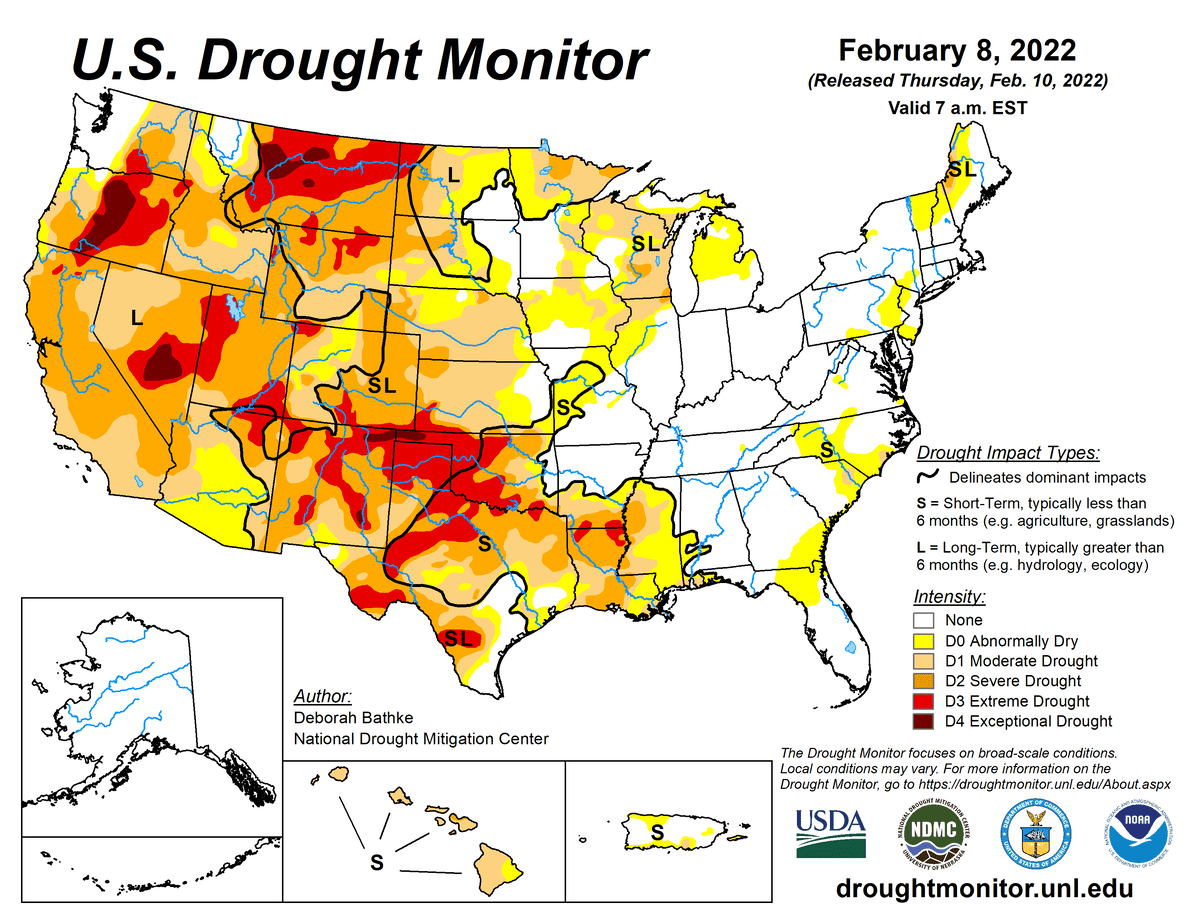

This week’s drought map for the United States.

How Could this Mega Drought Impact Crops?

Over 70% of the winter wheat-producing areas in Kansas, Texas, and Oklahoma are in drought conditions. Meanwhile, Eastern Europe also is experiencing relatively low precipitation. Wheat comes out of dormancy in the spring and moisture is key, so continuing dryness could impact the wheat market. As seen in the map below, dry conditions also have plagued the Canadian plains for the last month.

What happens in weather in April through June in the West and Midwest is important for corn and soybeans, too. Planting on the Plains starts as early as mid-April. Drought conditions in Argentina and Brazil have pushed soybean prices higher recently. Is a repeat in store for the U.S. crop?

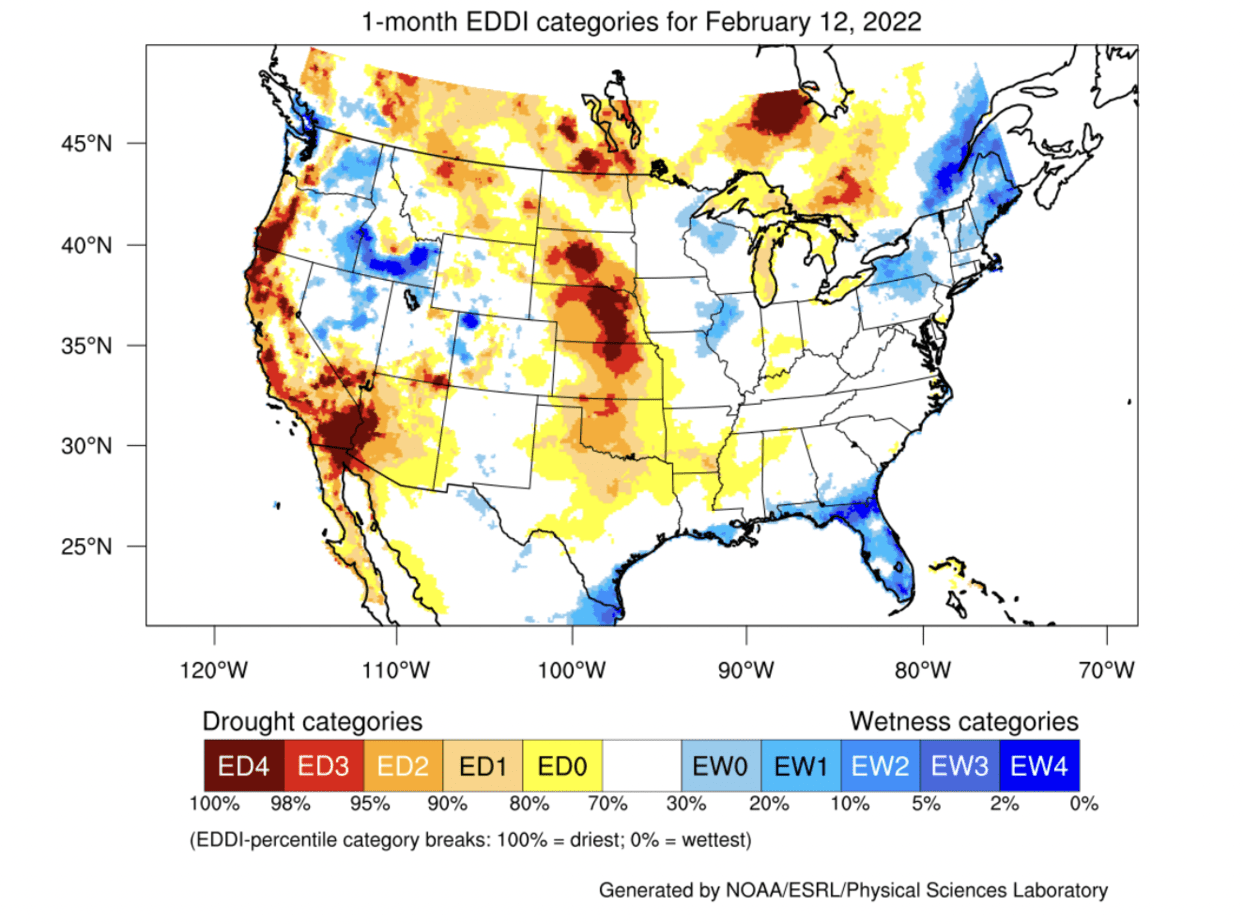

Evaporative Demand Drought Index for the last month from NOAA. An ED4 category signifies that similar conditions are expected in only 2% of this time period.

Faced with numerous challenges globally, this week the ICE Cotton No 2 futures contract bounced off the $0.60 level. In its latest outlook, the USDA estimated that global consumption of U.S. agricultural production dropped 15% in 2019-20. The collapse in cotton exports was bigger than that for other major agricultural commodities overall. Perhaps this is because cotton has no food industry support. People may change their diets, but they still must eat. Consumers can, however, stop buying clothes and new household textiles. Meanwhile, China’s recent US purchases are more than it needs for current operations and may be moved into the country’s reserve system. These bales could then be used to offset future purchases.

As with everything in 2020, many factors are playing into U.S. and global cotton prices. Let’s look at a country-by-country breakdown.

The Overall Market

While China and India are the world’s biggest cotton growers, the United States is the biggest exporter. China is by far the biggest cotton user (although not the largest importer), with India coming a distant second. US prices have rebounded from March lows, but its export sales have been flaccid. For the week of July 23, US cotton was sold to only 6 countries, with Vietnam the leading buyer.

Like many commodities, this market is dictated, to some degree, by Chinese concerns and actions. U.S. cotton is gripped by drought in key growing areas, but global circumstances make prices. Even low oil prices globally can impact cotton. Lower oil prices mean lower prices for the synthetic yarns that can replace cotton in a garment or other textile. In July 2019, cotton and Chinese polyester were only a few cents apart in price. This month, cotton cost almost twice as much. Three-quarters of Americans say that COVID-19 has to some degree impacted their finances. Final retail prices are now even more likely to dictate what yarns consumer fashion and textile brands use. Shoppers everywhere are more price-conscious, not just in the U.S.

India

With a 5% government increase in its minimum support price for cotton, India looks set for a bumper crop both this year and next. The Cotton Association of India increased its crop estimates for 2019-20 to 335 lakh bales, a jump of 8% on the previous year. (A lakh is a South Asian measurement denoting 100,000 of an item.) As of the end of July, government ministries held the planting area nationwide had increased by over 11% for 2020-21. USDA projections, however, see India’s production falling by around 7%.

At the same time, India’s estimated domestic consumption may be only 280 lakh, a fall of 15% from the previous year thanks to COVID-19. Prices in the open market have plummeted since the start of the epidemic and India’s spinning sector faces a contraction of 25% this year. The Cotton Corporation of India (CCI), a government entity, has bought approximately 1/3rd of the year’s production. CCI is looking to increase India’s exports to Bangladesh, the world’s largest cotton importer. It also is building a warehouse in Vietnam for Indian cotton to increase sales in that country. Vietnam is the world’s second-largest importer and India’s third-largest cotton market.

Locusts in Cotton Areas on the India-Pakistan Border

Pakistan is the world’s fourth-largest producer but production no longer meets the country’s manufacturing demand. Brazil, Spain, the United States, and India take up the slack. Issues with seeds and the inability to hedge crops successfully are some of the issues impeding Pakistan’s cotton expansion. Raw cotton exports for the first 11 months of FY20 decreased by 9.93% while yarn exports declined by 13.12%. Because prices have fallen and other crops are easier to grow, Pakistani acreage has declined by 1.3% this year, according to the Cotton Commissioner.

Pakistani cotton is grown in provinces along the border with India. It is here that the locust swarms that started in Africa have made their roost and continue to breed. In India, over a million acres have been sprayed to control the flying insects. So far, the Indian government says, there has been no major damage in Gujarat and Rajastan, the primary cotton areas. Because of incentives to abandon rice, India’s Rajastani farmers have increased cotton acreage this year.

In July, locusts were swarming in Pakistan and India’s cotton areas. Source: FAO.

Pakistan’s locust efforts have not been as co-ordinated, at times, and there are worries that the insect plague could lead to severe food insecurity. This month, China donated 12 agricultural spraying drones to Pakistan, along with technical assistance to operate them. A previous plan by a Chinese company to send 100,000 ducks to eat the Pakistani locusts was axed as unrealistic. The Himalayas separate India and Pakistan from Chinese territory and the mountains’ altitude and climate are not hospitable to locusts. The only locust route to China’s cotton-producing Xinjiang Uygur Autonomous Region would be through Kazakhstan.

Xinjiang, Uighur Rights, and the Chinese Cotton Supply

To those who follow current affairs, there may be no commodity as politically charged right now as Chinese cotton. The world’s second-largest cotton producer, China grows about two-thirds of what it needs to supply its textile and garment industries. Xinjiang province, in China’s west, now produces about 85% of the country’s crop, a substantial increase over the 52% Xinjiang produced in 2012. Since 2014/15, China has increased agricultural subsidies to Xingjiang, while cutting them to more populated provinces in the east, which had seen labor costs spike. Workers there prefer higher-paying manufacturing jobs over farming. Xinjiang’s dryer climate also had the advantage of fewer pest problems.

Xinjiang’s growing dominance is not just an agriculture story, however. The region’s growth is a prime example of politics and economics colliding or colluding, depending on your point of view. The Xinjiang Production and Construction Corps (XPCC), a quasi-state, quasi-military entity, was set up by Mao Tse Tung to “stabilize” the area. Xinjiang is peopled primarily by the Turkic-speaking, Muslim Uighurs, not Han Chinese, like most of the country. The XPCC serves as the equivalent of the regional government but it also runs businesses. XPCC brings in Han migrants to pick cotton, at rates higher than the local population, and sometimes gives them their own plots of land. It is in some ways the same economic strategy as that used to increase the Han population in Tibet.

All this means that more pressure is being put on garment and textile companies globally to ensure that forced labor is not used anywhere in their supply chain. That includes the production of cotton. The U.S. State Department was stark in its July 1 Xinjiang Supply Chain Business Advisory. “In addition to the forced labor present in the province, there is evidence of forced prison labor in the cotton, apparel, and agricultural sectors.”

THE US-CHINA TRADE WAR BOOSTED BRAZIL and AUSTRALIA

The new Australian dependence on cotton exports to China, however, recently took a nasty turn. Bankruptcy by a cotton importer in China has left the Australian cotton market reeling. Privately held Weilin Trade, which also had a cotton farm in Australia and processed cotton, had committed to buy up to half the Australian cotton crop for the 2019-2020 season. Plagued by drought for several years, this year’s crop was the country’s smallest in four decades. However, some analysts had predicted that next year’s crop would triple, thanks to increased rains.

What caused the firm’s collapse was both Covid-19 and Chinese textile companies’ belief that Australian cotton was too expensive after the drought. They switched to Xinjiang cotton instead. Australia is heavily dependent on exports to China, and policy, such as the development of Xinjiang, and politics have impacted the agriculture sector. Australian farming had been hit with Chinese export restrictions on beef and barley earlier this year. This came after the government called for an inquiry into the origins COVID-19. Unsurprisingly, after Weilin’s collapse, Australian cotton prices have tumbled.

United States

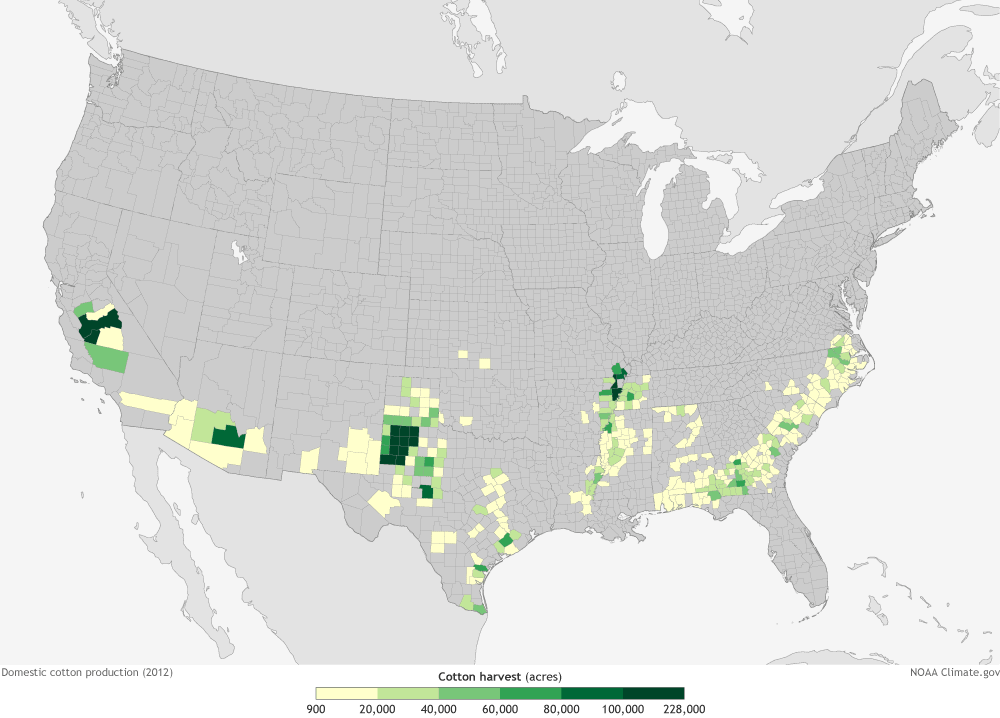

USDA 2020 cotton harvest predictions are now 12% below production for 2019, possibly with lower quality. The highest producing United States cotton counties are now primarily in the Southwest: Texas and Arizona. As previous Best Weather posts have pointed out, there has been a serious drought in the high producing West Texas areas.

Counties producing cotton in the United States.

As the world’s biggest exporting country, U.S. markets have been hit hard by COVID-19 related losses. California cotton farmers are planting an estimated 20% less land for 2021 harvest due to pandemic related losses. The Southeast is expected to sow 17% less acreage and the Delta region 22% fewer acres than in 2019. In the West, farmers are expected to plant 19% fewer acres than in 2019. This would be the lowest acreage in five years.

Which Way Will Cotton Go?

While US cotton farmers are decreasing acreage in light of 2020’s calumnies, Indian and Brazilian farmers have expanded. COVID-19 is continuing and most countries are unlikely to recover lost GDP for a while. With old stocks high and the expansion of foreign cotton acreage, U.S. and other cotton producers need luck to break out of the present trading ranges. Recently languishing in the upper-50s to mid-60s, ICE cotton seems unlikely to recover the summer of 2019 heights of 94.21 anytime soon. The one bright spot for non-Xinjiang cotton is the push for supply that can easily meet human rights production standards.

Xinhua, the Chinese state news agency, reported on Tuesday June 21st that non-structural, peripheral parts of China’s Three Gorges dam had buckled during the weekend’s severe flooding. Controlling the country’s might Yangtze River, which crested from flooding on Saturday, the Three Gorges Dam is the world’s longest.

On Sunday, authorities in China’s central Anhui province blasted a dam on the 100-mile long Chu River, a tributary of the Yangtze, in hopes of easing floodwaters. The Chu flows into the Yangtze near Nanjing, 150 miles northwest of Shanghai and the nation’s capital during part of the Ming Dynasty. Meanwhile, flood warnings were also raised for the Huai River, in the eastern part of the country. In 1911, flooding in both the Huai basin and along the Yangtze caused major flooding. An estimated 70% of the rice crop was destroyed and famine followed.

Summer is Flood Season

China’s flood season runs from April through September, when monsoon season hits the southern part of the country. While this year’s flooding has been concentrated, so far, in July, other river disasters have come later in the year. The 1887 Yellow River flood, which killed as many as 2 million people, crested at the end of September. The famine-bearing 1911 Yangtze flood hit its height in August. Up to 4 million people lost their lives.

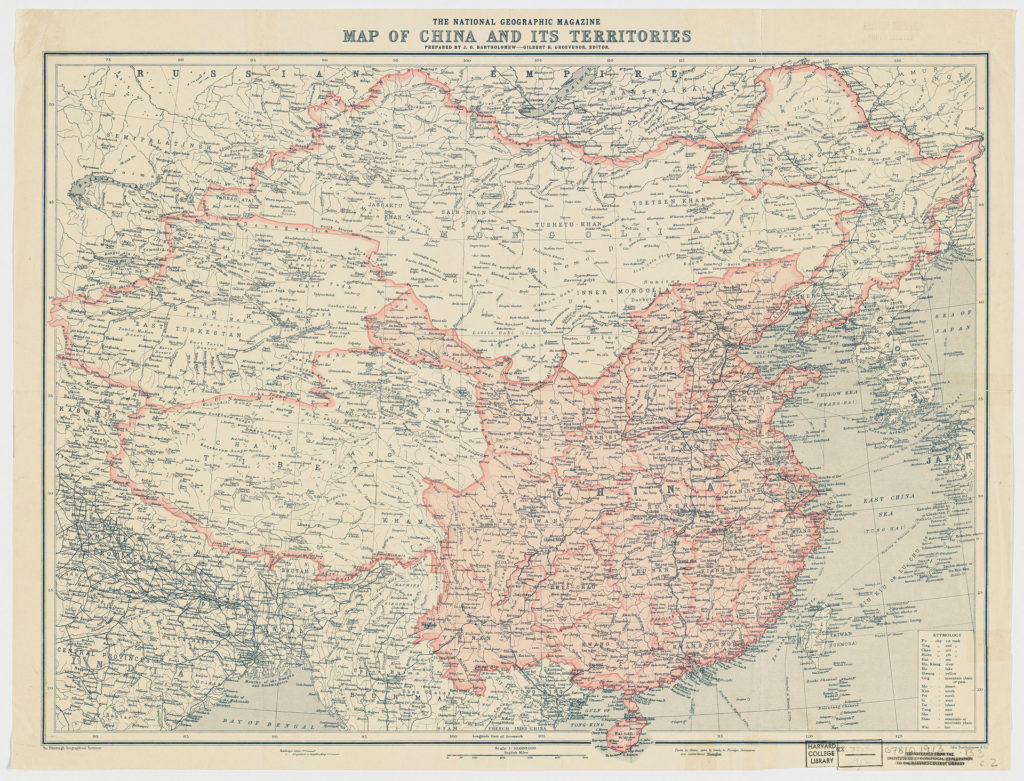

Map of China from 1912, a year of famine brought on by floods in 1911. Source: National Geographic.

Will China’s Agriculture Planning Blunt Flooding’s Crop Impact?

The long-term goal of Chinese agricultural policy is to make the country as food-sufficient as possible.

By 1949, when the Communist Party of China took control, almost all of China’s arable land was farmed. The country since often had national agricultural planning, prescribing what can be planted where. This led to improvements in some areas, but also to disasters such as the 1959-61 famines during the The Great Leap Forward.

Liberalization in the 1980s lifted controls on farm prices and led to small farmers being able choose what they planted. However, little could be done about the lack of arable land. Today, only about 14% (134 million hectares) of China’s land can produce crops. Urbanization and polluion have decreased arable land available in the traditional southeastern and central agricultural heartland.

In 2017 and again in 2019, new policy documents advocated pooling of land resources to encourage larger-scale agriculture. As part of the plan, China’s agricultural bank offered support for larger scale agricultural infrastructure. A subsidy of up to 30% of the cost of large agriculture machine also became available. This helped support agricultural development in “less populated” parts of the country.

Subsidies by Province Encourage Production in the North and West

These policy documents also proposed that certain regions be designated for the growing of specific crops. The areas would then be targeted for subsidies and technical assistance. An example of this is northeastern Heilongjiang province’s support for soybean growing. To encorage the switch from corn to soybeans in 2018, farmers received 75% more in subsidies than farmers in traditional soybean growing areas.

Rice production has also shown a dramatic shift north, thanks to government encouragement. As industrialization grew, rice production in water-abundant coastal provinces like Guandong decreased. In 1995, the northern provinces of China only produced 7.5% of the country’s rice crop. By 2018, northern Heilongjiang province alone produced over 12.5% of China’s homegrown rice. Hunan, watered by tributaries to the Yangtze, is traditionally the most productive province for rice. In 2018 Hunan’s harvest was beaten in size by Heilongjiang’s abundance.

Cotton production, too, has moved according to government supports. In 2000, the western province of Xinjiang produced 32% of China’s cotton, today it’s around 80%. Henan and Shandong, on the Yellow River, and Hubei, Anhui and Jiangsu, on the Yangtze, were responsible for over 43% of cotton in 2000. In 2018, together they produced less than 10%.

Western China’s new bug fighters. Source: Radoslaw Ziomber, licensed under the Creative Commons.

What Else Can Hit Chinese Agriculture This Summer?

The main Chinese cotton areas are outside the flood zones. The geographic shifts in production may have helped ameliorate some of the flooding’s agricultural impact on cotton and other crops, but there is still ten weeks until the end of September. The weather may hold the key to both production levels and commodity prices.

Drought has prevailed from Myanmar through Vietnam for months. With the Mekong River at some of its lowest levels in decades, monsoon rains began in parts of SE Asia in June.

Starting in Tibet, the Mekong winds through six countries: China, Myanmar, Lao PDR, Thailand, Cambodia, and Vietnam. 60% of the population along the Lower Mekong make a living from agriculture. Over 70% of the water that is used from the lower reaches of the Mekong is for agricultural irrigation.

The 2020 Drought for Mekong Countries

This year the river’s water has been scarce, making the drought worse for agricultural commodities and life in general. Called the worst in 40 years, this year’s drought comes after the 2018-19 season was marred by drought, low Mekong levels, and a truncated monsoon season.

The Thai Meteorological Department declared that 2020’s rainy season officially began May 15, but expects water for the first two months to be insufficient for farmers. Irrigation water is scarce. The Thai government has started projects to tap groundwater for irrigation and household use.

While the drought led to seawater incursions in Thailand, and saltiness in Bangkok’s drinking water, in Vietnam’s Mekong Delta, one of the country’s “rice bowls”, saltwater incursion has reached record levels. Vietnam has directed farmers to switch to other crops from rice in some parts of the Mekong Delta since freshwater is so scarce.

By May, 27 of Thailand’s 77 provinces had been declared disaster zones. The drought has been blamed on El Nino, but this did not explain the extent of low water levels in the Mekong.

Perhaps the country that will be most impacted by drought and low water levels is Cambodia. Its Tonle Sap lake is a unique environmental wonder. In the dry season (October to March) its river provides 50% of the water flow into the Mekong Delta.

At the monsoon’s heights, waters from the Mekong make the Tonle Sap River flow backward, into the lake. Fish caught from the lake make up 70% of the protein intake for Cambodians. In 2019, the fish catch was 80-90% lower than normal. What that catch will be this year is anybody’s guess.

Sugar, Rice, Rubber, Coffee: Mekong Farming Supports Many Global Markets

Weather along the Mekong, and the waters of the river itself, plays a large role in several global commodities markets. Thailand is the world’s largest rubber exporter and the second largest exporter of cane sugar and rice.

Vietnam produces 36% of the world’s robusta crop, more than twice that of its nearest competitor, Brazil. Vietnam also is the third-largest rice exporter and fourth-largest rubber exporter. Myanmar and Cambodia also contribute to the global rubber and rice trade.

Farmers use a hose to get water for fields in Cambodia. Source: Khmer Times.

The monsoon waters didn’t come soon enough for Thailand’s sugar cane growers. This month, the Thai cabinet okayed a relief package for the country’s 300,000 sugar cane growers. Thailand’s sugar cane harvest will be about 25% lower than expected, mainly due to drought. Meanwhile, drought caused rubber tapping to decrease, with annual production expected to be down about 5%.

Vietnam has seen up to 30,000 hectares impacted by the drought in the Central Highlands, the country’s largest coffee-producing region. Last year’s drought led to a 14% drop in coffee exports. Saltwater intrusion and low water supplies in the Delta also likely will impact rice harvests. However, the country expects to export more than last year due to existing stocks.

Water Is Traditionally a Shared Resource

What China, which controls the upper Mekong, seeks from the river, however, is not increased agriculture production. It wants electric power. Eleven hydropower dams now operate on the upper Mekong.

Many observers feel that China views the Mekong as a “sovereign” water source, one which they should control since it begins in Tibet. Other Mekong countries have been developing shared plans for its use, with varying degrees of success, since 1957, with the formation of the Mekong River Commission. As part of its Belt and Roads initiative, China started the Lancang-Mekong Cooperation mechanism in 2015. (Lancang is the Chinese name for the Mekong). A key goal of the mechanism was creating a five-year development plan for the river, which included more dams. It also included destroying rapids on the Laos-Cambodia border. This would enable China to ship goods from inland Yunnan all the way to the Pacific.

The current dams meet China’s power needs, but some commentators posit it is holding water back for future power and agriculture needs. A recent study held that China withheld water from the lower Mekong for six months in 2019, even though it had abnormally high rain and snowfall that year. By January this year, normally turbulent stretches of the Mekong were dry in Laos and Thailand.

The lower Mekong region’s current water problems are a combination of climate change, weather, and damming the river. The Lancang-Mekong development plan has been only partially successful. China has agreed to share data on the river with downstream countries, and at least one dam, in Cambodia, has been put on hold. The region will have to wait through the rainy season to see if the river starts flowing again at its normal levels.

HELPING YOU MAKE THE BEST INVESTMENT DECISIONS BASED ON THE WEATHER

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.OkPrivacy policy