See my video above about how record warm oceans, brought on by El Niño and climate change are hurting West African cocoa crops

I wanted to provide you with insights into how high cocoa prices impact various equities, companies, and industries within the market. Understanding these dynamics can be essential for informed decision-making.

West Africa produces 70% of the world’s cocoa which is turned into Chocolate.

I mainly follow commodities but you may want to look into these equities. It has remainedvery wet with disease issues in parts of West Africa since summer and now some potential harvest delays. This is a major crop-impacting issue for cocoa and something I have been worried about and forecasting since June.

So how do you trade cocoa and other commodities based on the weather? Find out here.(click below)

Below is a list of some of the industries that can be affected by higher cocoa prices.

Chocolate Manufacturers – Companies like Hershey (HSY), Mars, Mondelez (MDLZ), Ferrero, and Nestle (NSRGY) are directly affected by high cocoa prices as they face increased input costs, which can put pressure on their profit margins.

Cocoa Processing Companies – Businesses like Cargill, Barry Callebaut, Blommer Chocolate, and Touton play a critical role in processing raw cocoa into ingredients for food companies. They, too, are impacted by the price fluctuations in cocoa.

Confectioners – Lindt, Godiva, Russell Stover, and Ghirardelli face higher costs for key ingredients, impacting the production of their confectionery products.

Bakeries – Companies such as Krispy Kreme (DNUT), Panera Bread (PNRA), and Dunkin Brands (DNKN) are affected as high cocoa prices influence the costs associated with cocoa-based products.

Frozen Desserts – Businesses like Unilever (UL), Nestle, and Blue Bell, known for their ice cream products, must contend with cocoa butter and cocoa powder price fluctuations.

Retailers – Giants like Walmart (WMT), Kroger (KR), and Costco (COST) may need to decide whether to absorb higher prices themselves or pass the increased costs on to consumers.

Cocoa Growers & Traders – Companies like Hershey, Cargill, Barry Callebaut, and Olam (OLAM: SP) are crucial in sourcing raw cocoa globally, and they experience the direct impact of cocoa price movements.

Cocoa ETFs – Notably, exchange-traded funds (ETFs) like NIB, used to track cocoa futures prices, and CHOC, which invests in cocoa companies, provide investment opportunities tied to the cocoa market. However, the ETF was retired last June.

In summary, rising cocoa prices have a cascading effect. While they can boost revenue for global cocoa suppliers and traders, they often squeeze the profit margins of manufacturers in the chocolate business, who probably constitute the hardest-hit links in the chain.

El Niño weather conditions can have varying impacts on different commodity sectors. Here are some of the sectors typically most adversely affected during El Niño years:

Agriculture – El Niño often brings heavy rains and flooding to parts of South America, which can damage crops like soybeans, corn, wheat, rice, coffee and sugarcane. Food production and crop yields tend to decline in affected regions.

Energy – El Niño winters tend to be warmer than average in the US, decreasing demand for heating oil and natural gas. Milder winters can also reduce electricity demand. This drop in energy demand can negatively impact the oil, natural gas and power sectors.

Metals & Mining – Heavy rains from El Niño can disrupt mining operations for commodities like coal, copper, iron ore and gold in countries like Indonesia, Chile, Peru and Australia. This can constrain output and drive prices higher.

Palm Oil – Production of palm oil in Southeast Asia, especially in Malaysia and Indonesia, tends to fall during El Niño events due to reduced rainfall and drought conditions. Supply disruptions can lead to higher prices.

Fishmeal – El Niño conditions often drive anchovy populations away from the coast of Peru, resulting in reduced catches of this fish that is processed into fishmeal and fish oil. This can impact the global supply of fishmeal for animal feed.

Presently, this is what I have been watching for my WeatherWealth newsletter clients with various futures, ETFs and option trade ideas. Climate change is also having a major global effect.

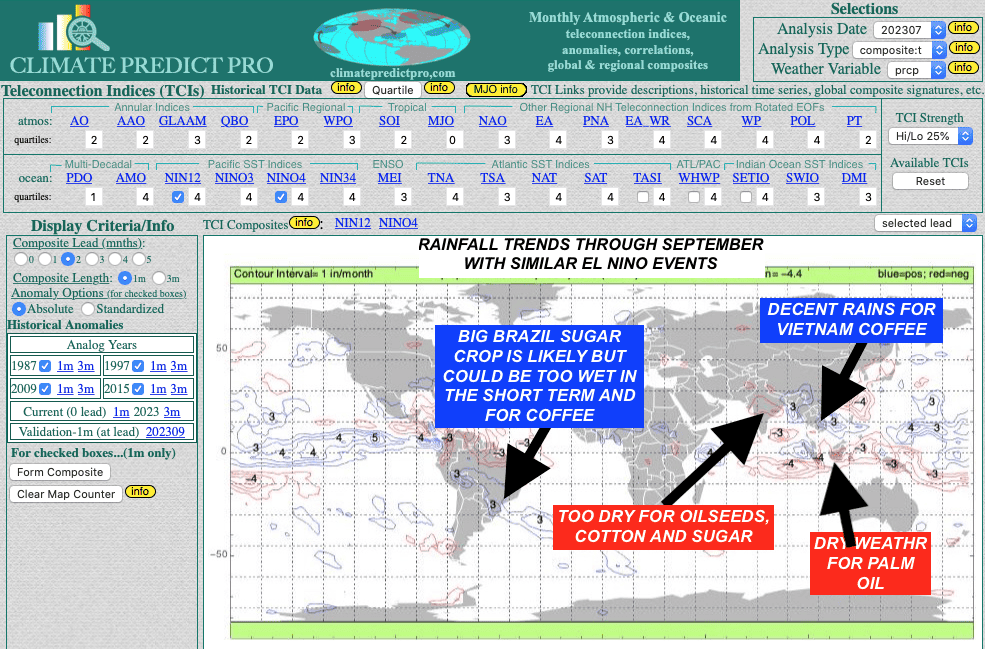

A) Weak Indian Monsoon for oilseeds, sugar, wheat, oilseeds, rice, and possibly cotton

B) Australia’s and Argentina’s developing drought for wheat

C) China’s historical heat waves and mixed floods and droughts may have damaged some of the corn and especially cotton crops.

D)Record warm oceans creating too much rain for the West African cocoa crop where disease issues have helped prices rally 10% more in the last 2 months.

E) Wet September weather in northern Brazil could cause some harvest delays or sucrose dilution to the sugar crop and cause an early bloom for coffee that is not wanted

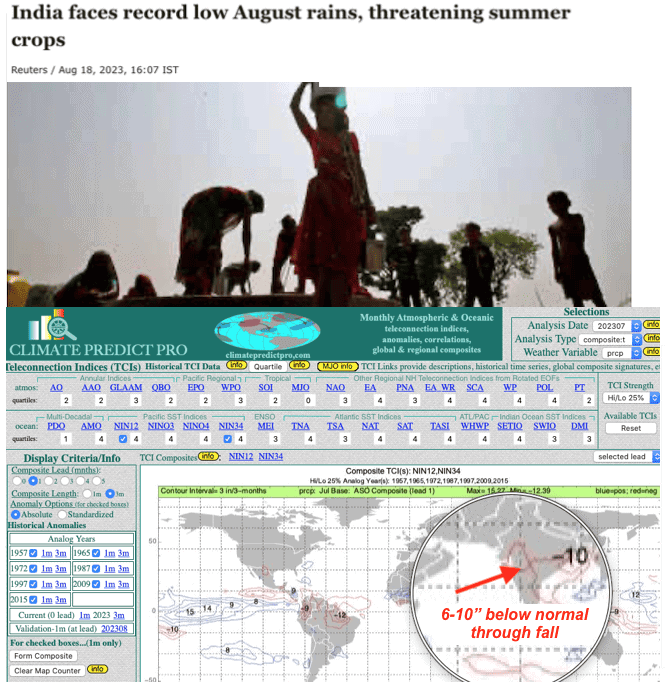

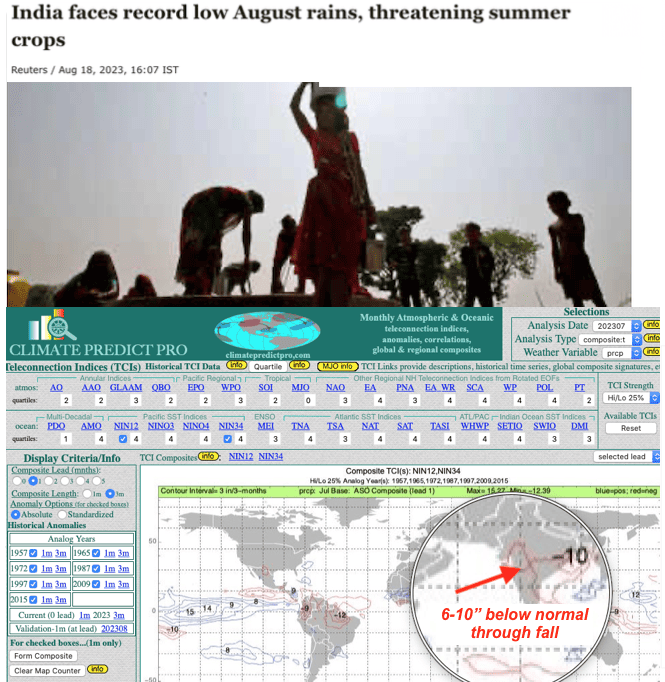

India’s August rainfall may be the lowest since 1901

El Niño often disrupts the Indian Monsoon. The monsoon is very important to India’s economy and has a $3 trillion annual effect on agriculture. Presently, it is the driest since 1901 and I do not see that trend changing, following excellent July rains. This will have a “lag” effect on markets such as soybean oil, sugar, rice, wheat, and possibly cotton and be one partially bullish factor in these markets.

HELPING YOU MAKE THE BEST INVESTMENT DECISIONS BASED ON THE WEATHER

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.OkPrivacy policy

{kind=link}