by Jim Roemer | May 10, 2018 | Commodities, Forecast, Uncategorized

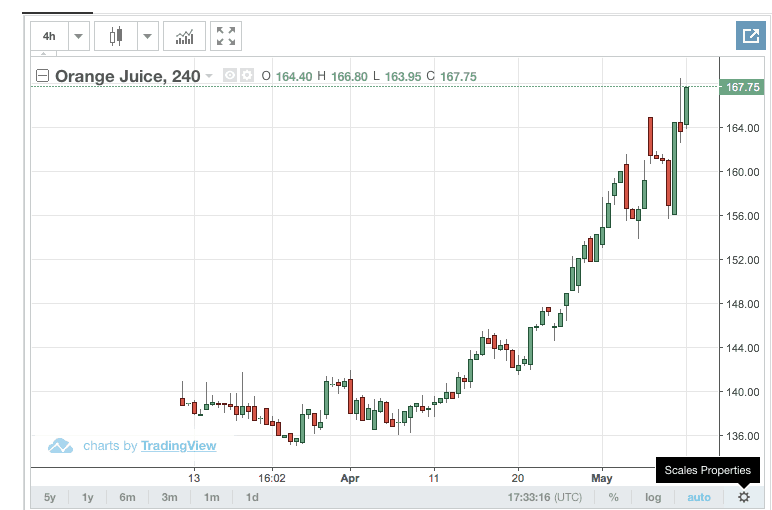

Orange juice futures are one of the most volatile commodity markets. “OJ” contracts are also quite illiquid. The chart below shows a 23% price increase since the end of March. This up move is in the face of reduced global demand for OJ, thanks to diet fads and alternative beverages (think coconut water), that have been in vogue in recent years. With demand fading, it takes a reduction in Brazilian orange production to get any semblance of a bull market underway. Citrus greening in Florida has practically destroyed the Sunshine State’s orange industry. While this has occasionally resulted in a sharp rally, I believe the current spike stems from last October’s dry weather. Despite Brazil’s record 2017 crop, production could fall sharply as new estimates flow in from the harvest’s progress.

For a recent report that likely influenced the run up in OJ futures, please click here

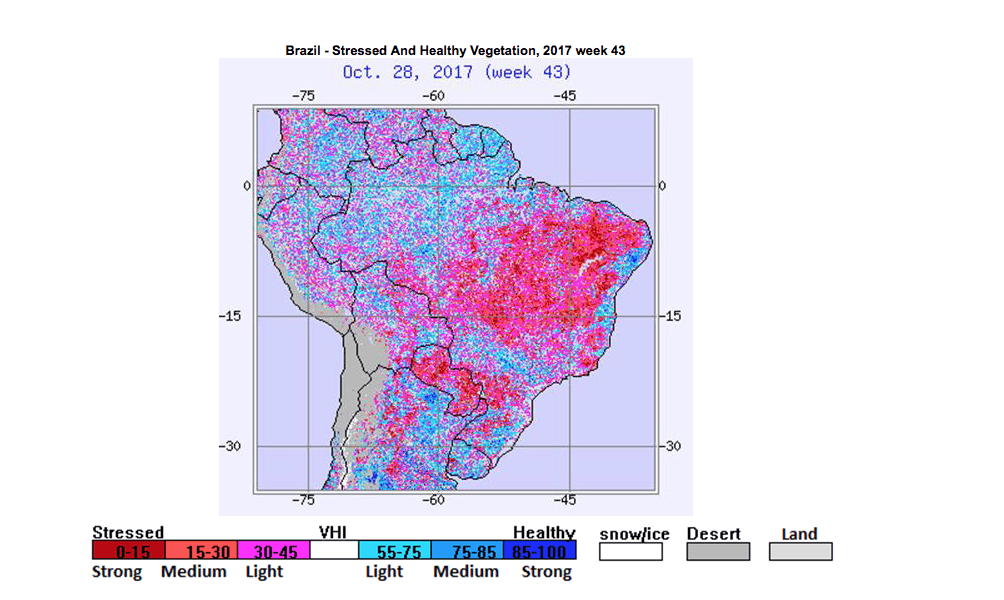

The map below shows last October’s heat and drought stress in Brazil. Certainly, coffee trees and buds have various growth cycles, thus affording them more opportunity to recover. This is not the case with oranges in years having a hot (and dry) October. Combine this with the above-mentioned citrus greening, now also affecting Brazil, and it is possible that OJ prices could rise even further. The price strength will be even more acute if Florida experiences an active hurricane season this year.

by Jim Roemer | Apr 30, 2018 | Commodities, Forecast, Uncategorized

Growing weather problems around the globe are adding a bullish spin on grain prices. But questions remain about a weakening La Nina and if May rainfall will increase in drought stricken areas of Texas to Kansas.

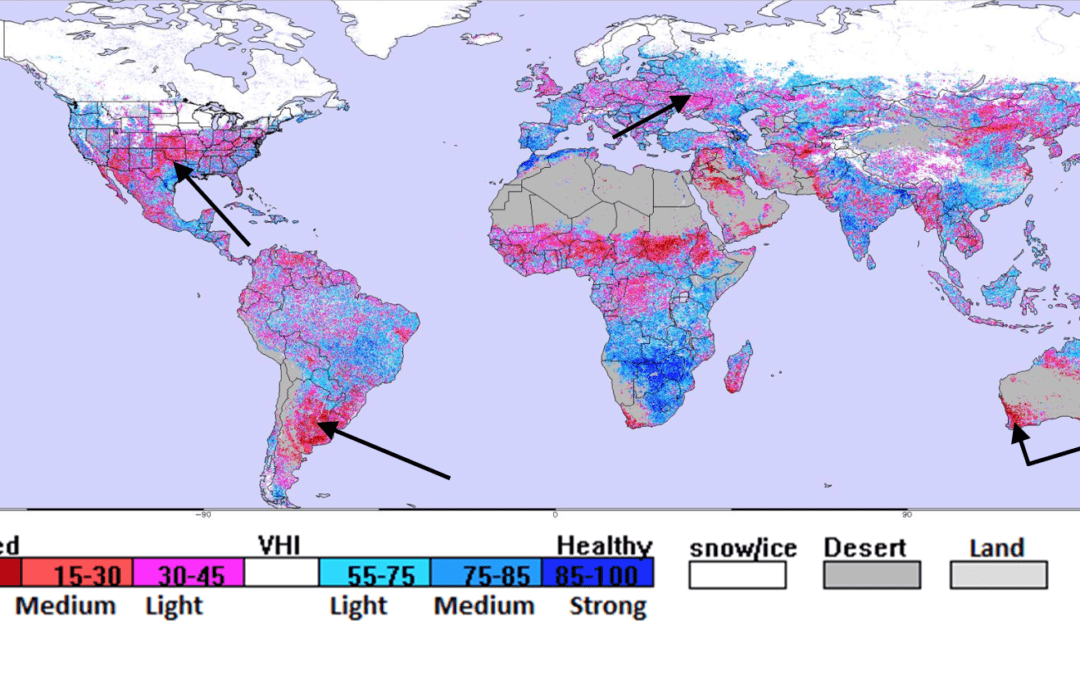

Wheat, in particular, has been in a major down trend for several years. With global stocks still near historical high levels, it will take reduced crops in other parts of the world (not just the drought stricken U.S. plains crop), to stimulate an authentic bull market in wheat. This may happening, finally. The the Climatech screen shot below (Figure 3.) addresses ‘stressed-versus-favorable’ wheat crop conditions. It illustrates problem areas (arrows) not only for the U.S. plains, but for planting in Australia and the developing crop in parts of Ukraine and western Russia. Some important rains may fall in Russia in a week or two and it is possible traders will focus on this, unless weather problems worsen.

For U.S. corn and soybeans, however, wet warm weather through May could cause a bearish spin on prices, after our bullish attitude all winter on strong demand and the worst Argentina drought in years.

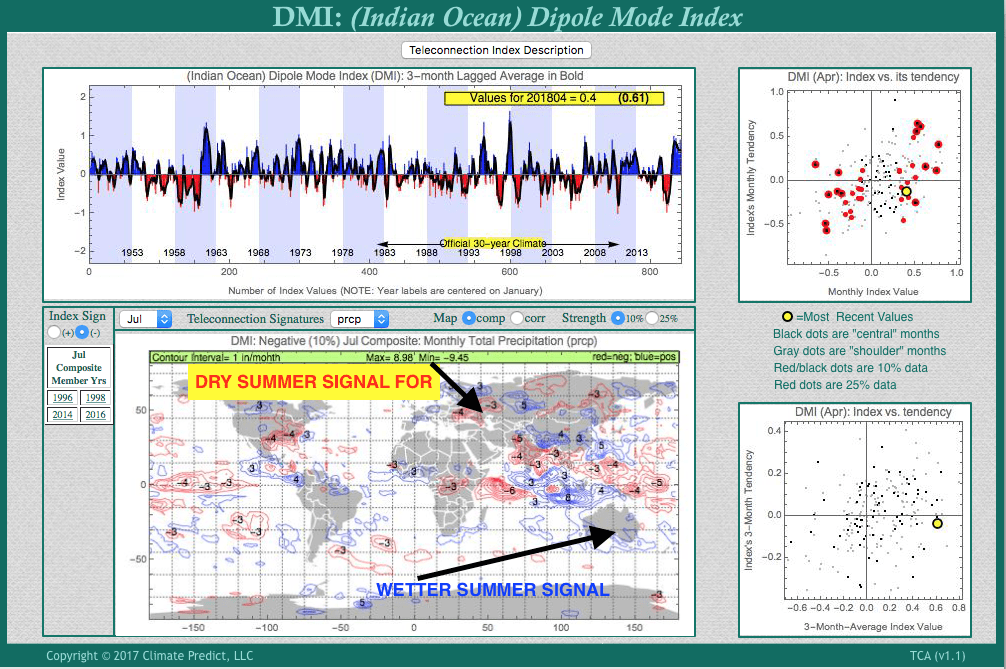

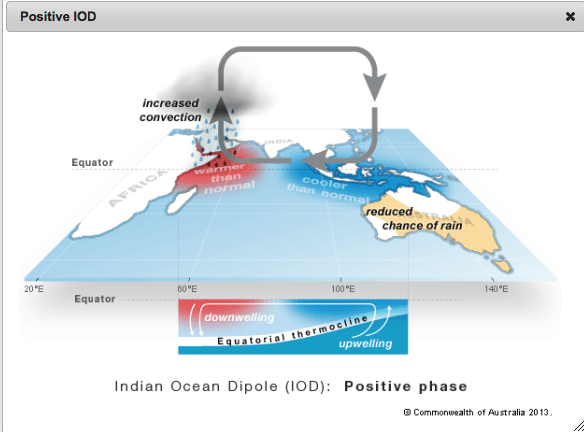

It is atypical for Australia to be in a four month drought during a weak La Niña. 75% of the time, this would result in good soil moisture for cotton, sugar cane and wheat. However, there a few exceptions, and this year is one of them. The Indian Ocean Dipole (Figure 1.) is a climatological phenomenon that can significantly effect Australia’s weather. The IOD has been unusually positive for several months. Normally, this does not happen during a La Niña. The upshot has been an extensive drought now covering many important growing areas. Consequently, according to all models below, the IOD will turn negative by summer (Australia’s winter).

Figure 1.

The Indian Ocean Dipole: When ocean waters warm to the east of Africa and cool over Indonesia, the IOD is positive reducing rains in Australia. While this often does not happen during a La Niña event, it has the last few months resulting in a much drier solution for Australia where wheat planting is not jeparadized.

Figure 2.

All forecast models suggest that the IOD will turn negative by summer. If so, it will bring relief to Australia in a few months, but Russia could have weather issues later this summer. That could result in the first decrease in Russian grain crops since the 2010-2011 season. However, standard computer models are beginning to show rains in Russia first. Otherwise, wheat prices could explode.

Figure 3.

If the IOD does go negative, the result would be improved moisture for many Australian grain areas. However, it is problematic that wheat will be planted in dry soils in coming weeks, prior to dormancy setting in and before winter rains and snows occur. Depending on Australia’s weather in September through November, when the wheat crop begins to grow again, yields would be greatly reduced “If” El Niño was to form and the IOD does not turn negative.

My greatest concern is regarding parts of Russia and Ukraine. On April 24th, I was early in suggesting to clients that dryness in these regions may begin to gain attention by the wheat trade. A weakening La Niña, as well as teleconnections such as the IOD and others, suggest the Russian grain crop will be compromised.

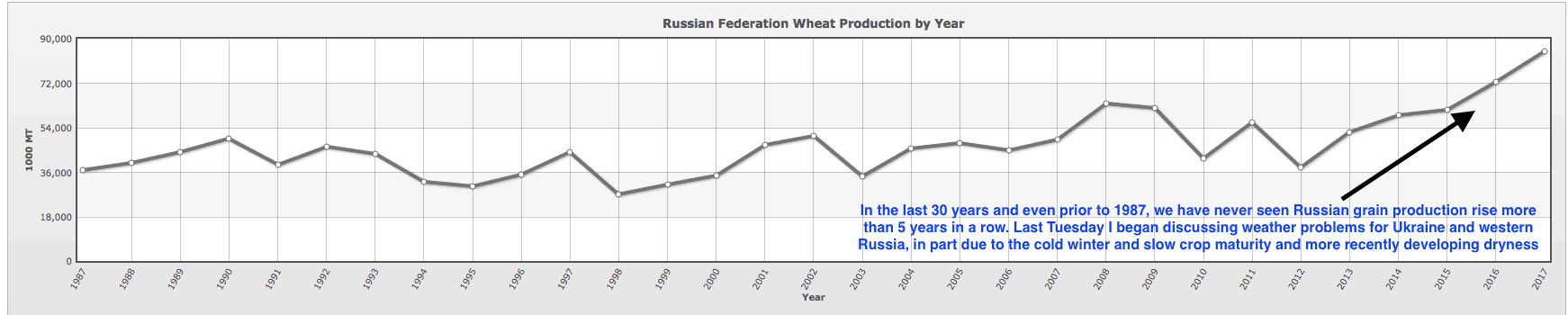

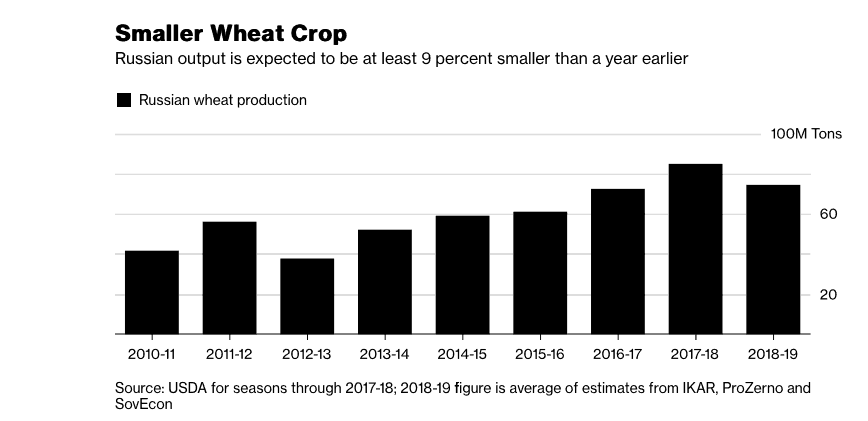

In fact, as the chart shows below in Figure 4, there have been five back-to-back wheat production increases in Russia.

Figure 5 bears out that there have not been six consecutive Russian wheat crop increases in 30 years. This matches well with our research.

Figure 4.

Figure 4.

Figure 5.

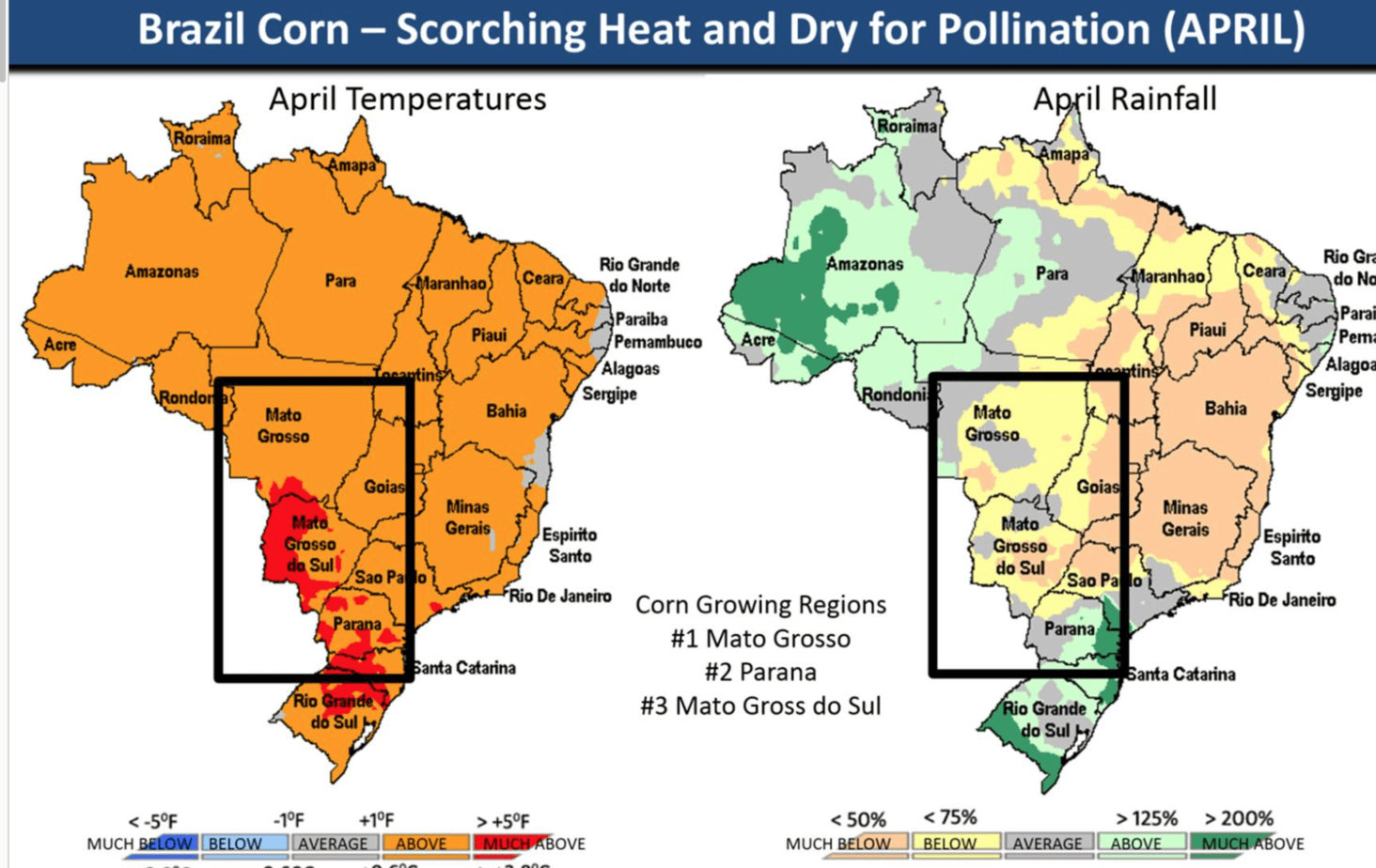

Finally, drought in Brazil is compromising the 2nd corn crop (SAFRINA)

SOURCE OF MAP ABOVE: WEATHERTRENDS 360

Figure 6.

by Scott Mathews | Mar 21, 2018 | Climatech, Commodities, Energy, Forecast, Global Warming

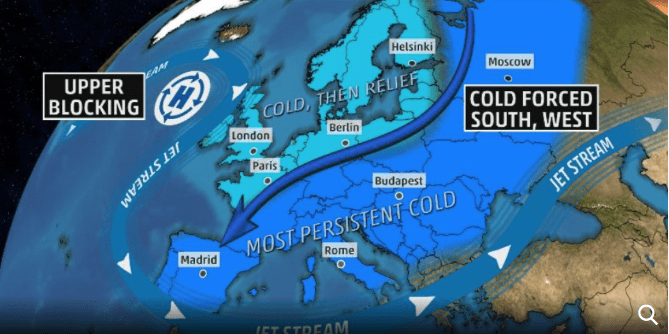

EUROPE’S BEAST FROM THE EAST

The warming Arctic this winter has resulted in incredibly cold weather in parts of Europe and Northeast Asia. Another symptom has been unusual March snowstorms in the Northeast U.S., the likes of which are unprecedented. Although four Nor’easters have clobbered the Eastern U.S., I do not agree with the forecasters who attribute this to La Niña.

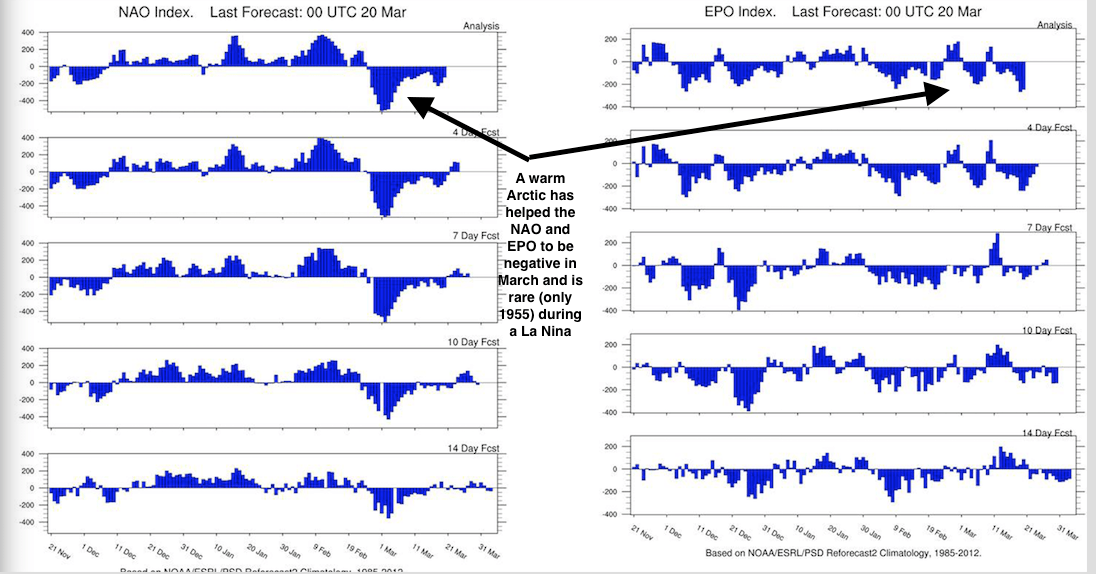

Once again, the “warming planet” signals are the handwriting on the wall. They read “the Arctic is warming” and “the Atlantic ocean temperatures are rising.” As far as the energy markets are concerned, the UK natural gas futures contract reacted extremely to the cold weather. The U.S. has not had nearly the consistent cold winter as observed in Europe. The negative NAO. Index (warm block near Greenland) and warming near Alaska (negative EPO) have resulted in this “Beast from the East”. For more information about this incredible European cold and some changing feelings about global warming, Please click the following link: Here

a rare coincidence of the NAO and EPO indices

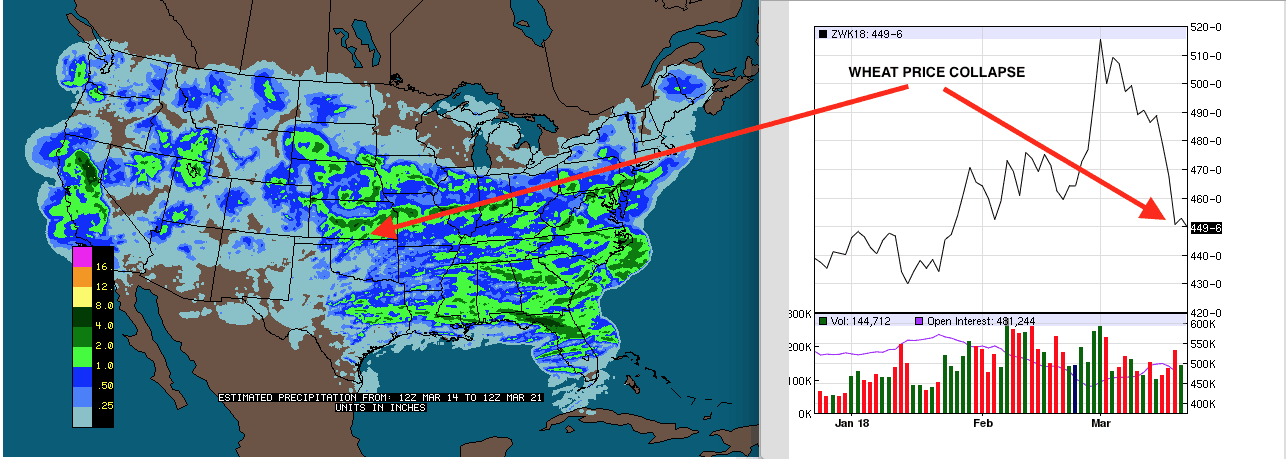

WHEAT PRICE COLLAPSE DUE TO SUDDEN SHIFT IN U.S. PLAINS DROUGHT

Wheat prices have had a steady climb during January and February, as the chart reveals below (right). However, it usually takes some other weather disaster somewhere in the world to have a longer term bull market in wheat prices. Two fundamental factors are brewing in the world of wheat:

a) The U.S. has not been competitive in the world market, and

b) Russia is sitting on huge global stocks.

These realities began to increase wheat market volatility long before we changed our forecast views presented to private clients on March 15th. We issued a heightened alarm for a potential easing of the Plains drought.

Due to weather factors not related to La Niña, there has been a precipitous drop in wheat prices.

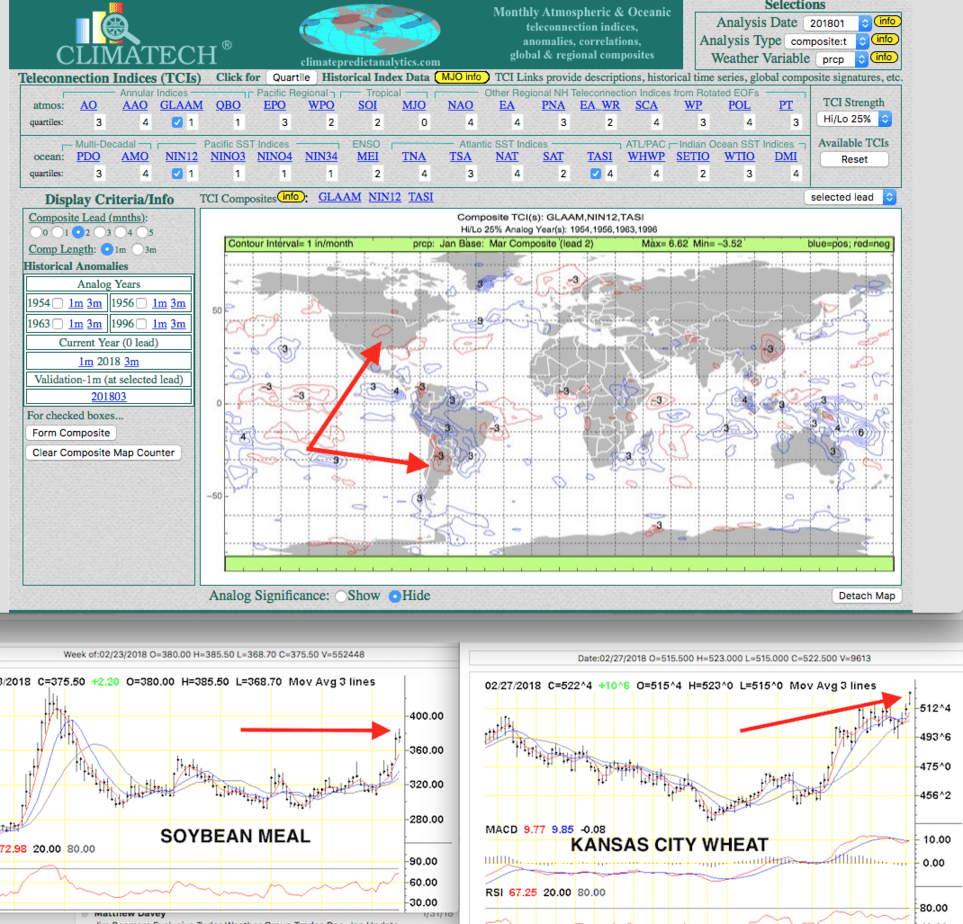

CLIMATECH (below) shows how the present La Niña is similar to 1955. Back then, “normal” dryness continued in the Plains wheat areas (red). Based on these teleconnections below, this should have happened. However, computer models, along with our forecast, began changing on March 15th. This prompted us to alert private clients about a potential change in wheat price direction. If you would like more information, please email us at

Present teleconnection situation vs 1955

COCOA PRICES SOARING

As wheat prices have taken it on the chin, one of the lone bull markets in agricultural commodities recently has been in cocoa. Dry, hot weather did cause some minor reduction in the west Africa cocoa crop this winter. This is quite is unusual for La Niña. However, the main reason for the bull move is far too many short futures positions. This high level of commercial hedges are bumping up against rising global demand. In addition, there is press coverage pointing out that cocoa farmers in Ghana will see lower production in coming years due to the “illegal gold mining boom.”

Here is an excerpt from the current issue of National Geographic:

“Gold mining has always been a part of Ghana, from the ornate jewelry of the Ashanti kings to British colonization. In the last several years, largely unregulated galamsey (informal, illegal) mining has ramped up, due in part to Chinese investors who bring in sophisticated equipment and a lagging economy that makes the prospect of striking gold too sweet to pass. These often illegal operations can result in contaminated water, deforestation, and a rise in violent crime.”

“In 2011, Ghana produced a record-setting amount of cocoa, weighing in at over one million tonnes. Since then, as illegal mining steadily ramped up, cocoa production has trended downwards, with a drop to 740,000 tonnes in 2015.”

For the full, interesting article about this from National Geographic, please click here

(more…)

by Jim Roemer | Mar 8, 2018 | Commodities, Forecast

Most studies we have done continue the severe drought for the Plains wheat areas. Traders and researchers that want detailed up to the minute reports on our feeling of the wheat market and updates for international crops should email us at subscriptionsbestweather@gmail.com

by Jim Roemer | Feb 28, 2018 | Commodities, Forecast

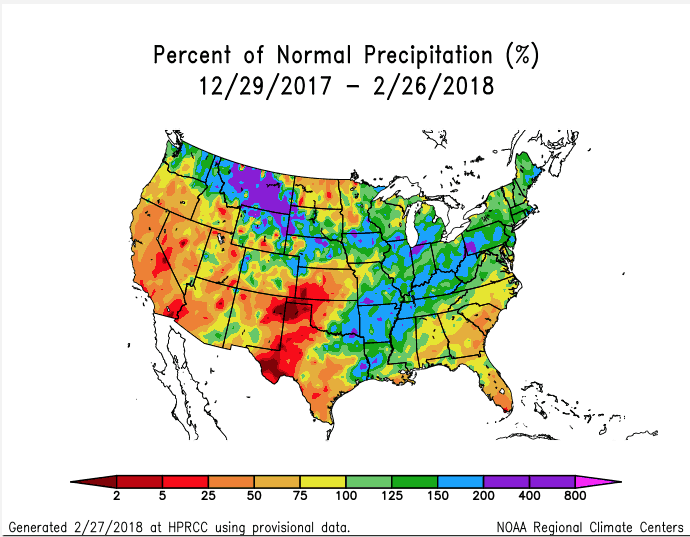

The NOAA rainfall map shows the growing drought (red) that impacted Plains wheat since the end of December. Much of the Ohio Valley suffered flooding and tornadoes.

From the economist’s point of view, food prices are on the rise due to inflation concerns based on interest rates, jobs and wages. Those are the US-centric fundamentals. We keep our eyes on the whole enchilada… Global drought is a macro systemic condition. It pierces the very core of the world’s food supply. On January 27th, our CLIMATECH analytic program predicted droughts in both the Plains wheat area and in Argentina. Recipients of our newsletter read our warning of the potential price explosion. Our forecast, based on global teleconnections (La Niña and other global ocean temperature indices) portend further problems (red) for the month of March.

The world’s largest exporter of soybean meal is Argentina. The drought will have a multi-billion dollar effect on that nation’s economy.

For the best commodity and weather analysis and for information on how you can DEMO this unique long range forecast, please email us at. subscriptionsbestweather@gmail.com

A LOOK AT GLOBAL RAINFALL TRENDS FOR MARCH, PREDICTED IN JANUARY. RED AREAS INDICATE DRYNESS.

by Jim Roemer | Jan 2, 2018 | Commodities, Energy, Forecast

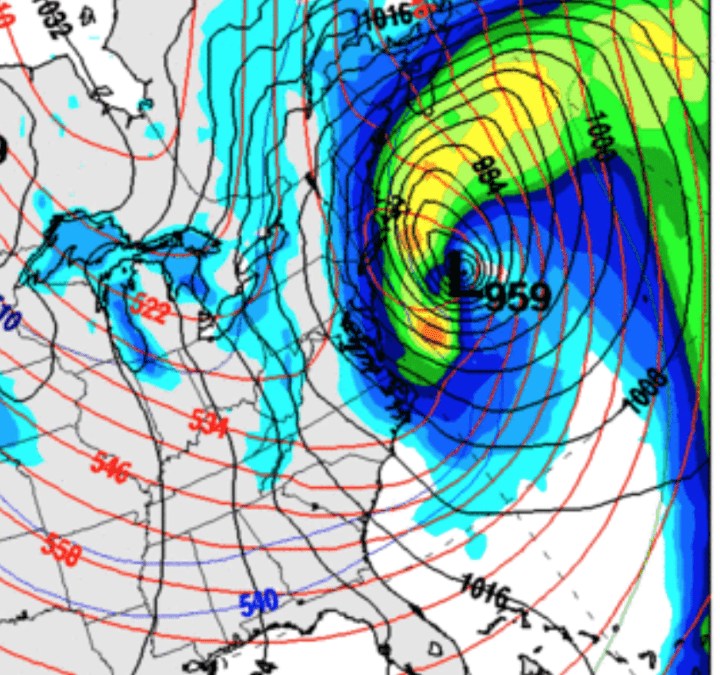

Record cold and very warm Atlantic SSTs may lead to a major snowstorm this week. “Explosive cyclogenesis” refers to a rapidly deepening extratropical cyclonic low-pressure area. The less scientific names for this rare phenomenon are:

-

Weather bomb

-

Meteorological bomb

-

Explosive development

-

Bombogenesis

The next snowstorm to brush the eastern U.S. will hit on Thursday and bring record cold. Most noteworthy, this could be an historic event in terms of establishing the lowest barometric pressure ever observed and recorded. Some areas around Boston, including Cape Cod and even eastern Maine, could see 1 to 2 feet of snow. However, the ultimate problem will be the extreme cold with sub-zero wind chills all along the east coast. Therefore, on Thursday, near hurricane force winds could hammer the entire region from Long Island to Cape Cod.

For more information about “Bombogenesis” please go here.

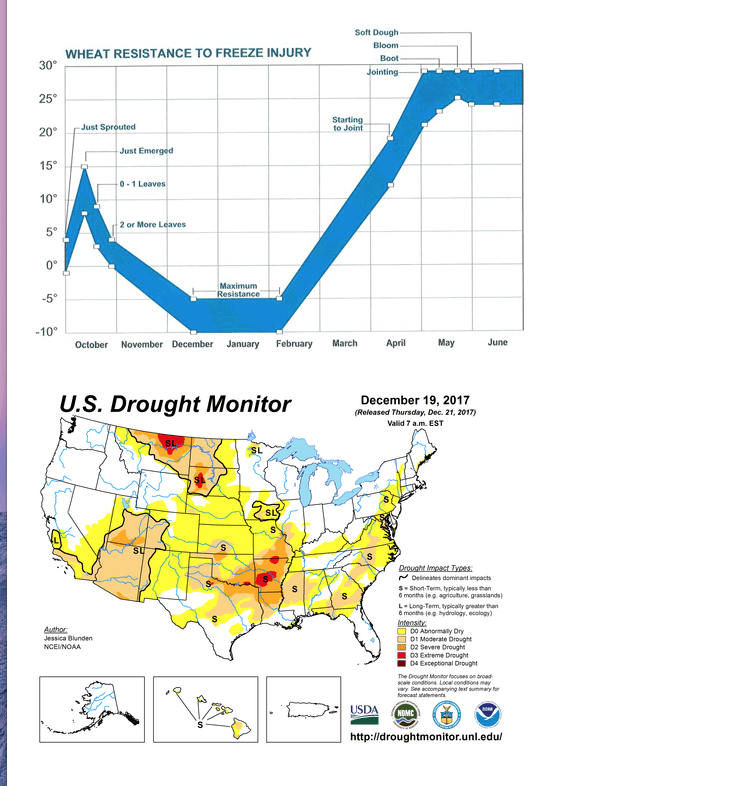

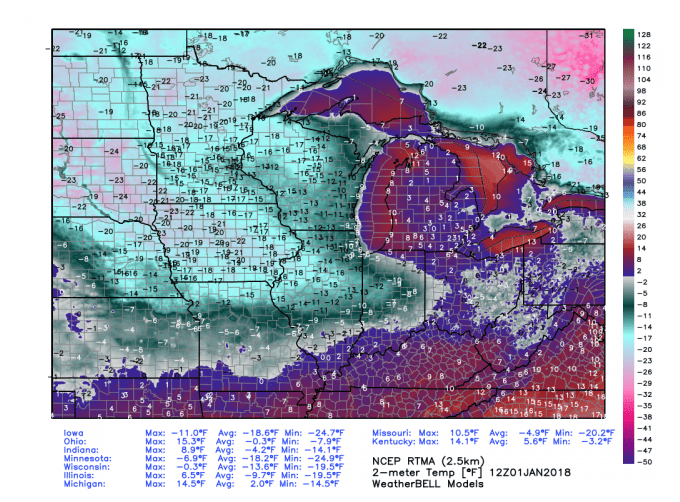

U.S. wheat crop suffering from drought and cold:

In addition to the drought expanding, record cold temperatures probably damaged some U.S. wheat. Therefore, extremely cold weather in the Plains, combined with worsening drought, will likely begin to adversely affect the wheat crop.

Yet, we expect moisture in the Plains by mid January. When spring arrives, if widespread moisture has not occurred across the U.S. grain belt, wheat prices could stage a major rally.