by Jim Roemer | Aug 21, 2017 | Climatelligence

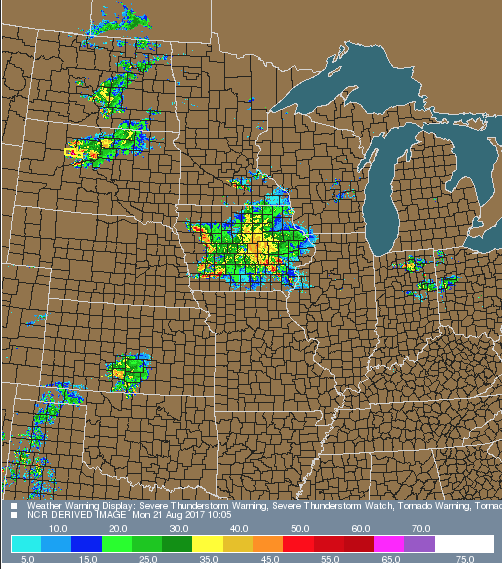

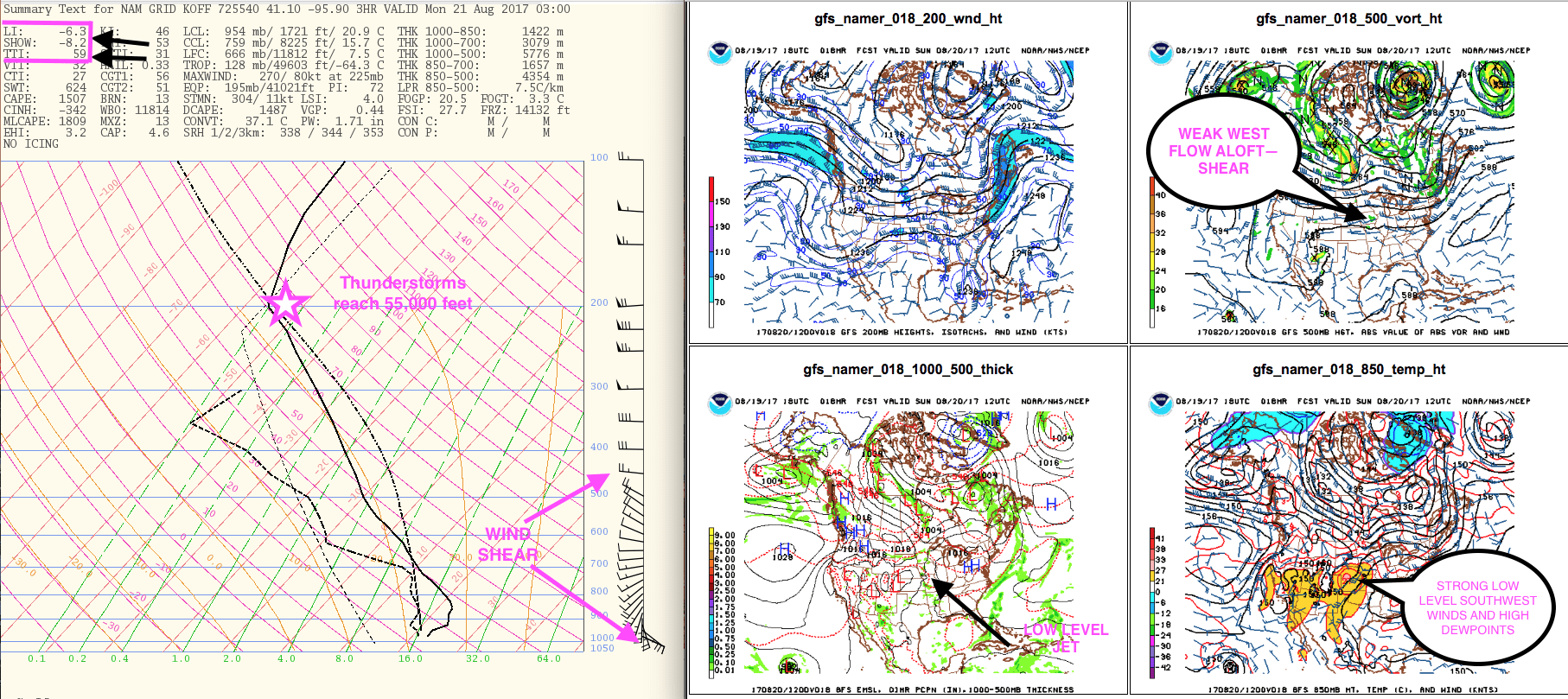

Great rains fell over drought stricken Iowa this morning. We mentioned this possibility in our newsletter Friday morning. Models did not pick up on the extent of these storms until Saturday. However, the general set up showed a strong potential for ample rainfall. Models forecasted weak westerly flow aloft, a low level jet, and strong low level southwesterly winds a high dew points. This led to deep thunderstorms with a Lifted Index of -6.3 and a Total Totals Index value of 59.

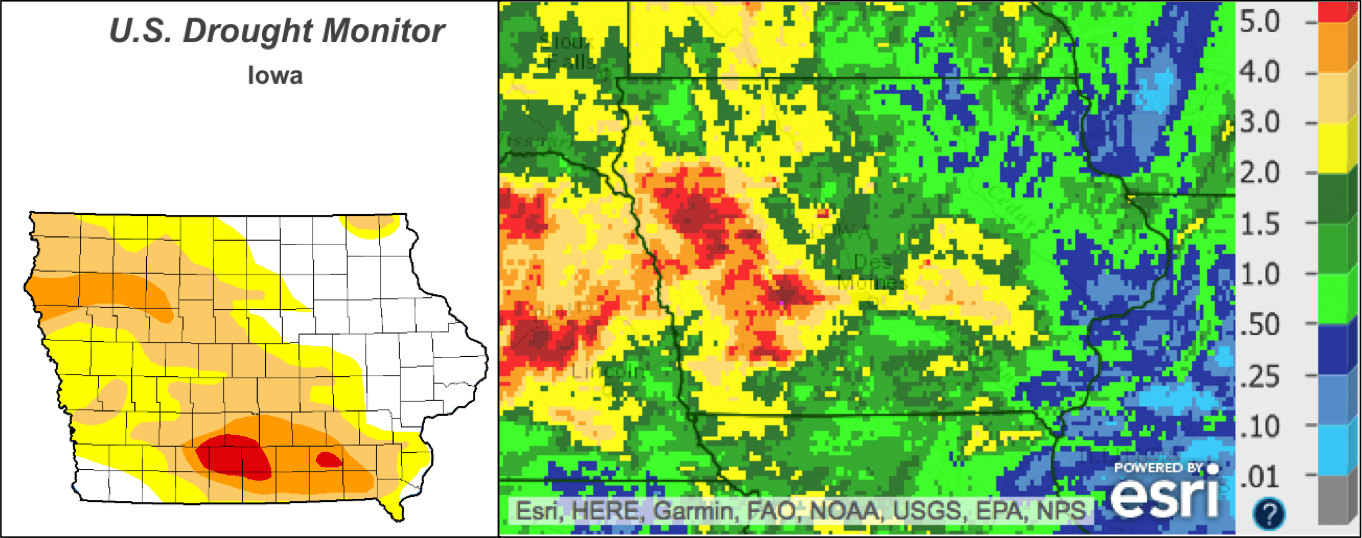

The rainfall over the past two days should improve drought conditions in parts of southern Iowa. Notice the 2″-6″ in the image below. Traders will have to grapple with this news and the fact that PRO FARMER tour will be going on August 21st-24th. The recent beneficial weather may be overshadowed by the realization of damage from previous dry weather.

HERE ARE TWO EXCERPTS FROM OUR CLIMATELLIGENCE WEATHER COMMODITY NEWSLETTER LAST WEEK:

USDA Shocker for Grains

“Several weeks ago, we stated that the Iowa drought would begin to ease later in the summer, and that the easing “would just be a matter of time.” Also, we pointed out that it is rare to get a bull market in corn and soybeans when the weather is cool in the Midwest. With August weather much more favorable and the world awash in beans; furthermore, a couple of weeks ago, we advised subscribing clients to reverse positions and ride the current wave down in soybeans. All eyes will be on the September USDA crop report and whether, or not, the department’s huge crop estimates had been over-estimated. September can often be an up month in grains, so we would not recommend necessarily shorting grains on this current break, although, U.S. weather is bearish for now. We look for important rains in drought stricken Iowa, next week.

SOME RECENT TRADE SUGGESTIONS

So what were some of our other trade suggestions in late mid-late July in Climatelligence? Remember, this is only a FREE newsletter right now, and again not all of our thoughts, trade ideas and viewpoints have been presented.

We recommended selling cocoa put options, thinking that demand and disease issues in west Africa could help prices, and also selling natural gas after potentially bullish EIA numbers in the July 27th report. The gas advice was due to cool weather. However, both of these recommendations were “short-term” in nature and not available in our monthly newsletter. Cocoa prices hit resistance a week or so ago, and we felt that at $2000, prices were high enough. Global production has rebounded and the chances for El Nino have diminished.

Finally, the psychology of the hurricane season and lower production from recent EIA reports could set a floor in natural gas prices. Though we are still awash in shale production; and cool late summer U.S. weather is keeping a cap on prices. Both the crude oil and natural gas market will be watching the Gulf coast or hurricanes this fall. Given the potential for more international tensions and hurricanes, crude oil may have more upside potential.

However, updated daily advice is only reserved for full time daily clients email us for information at subscriptionsbestweather@gmail.com

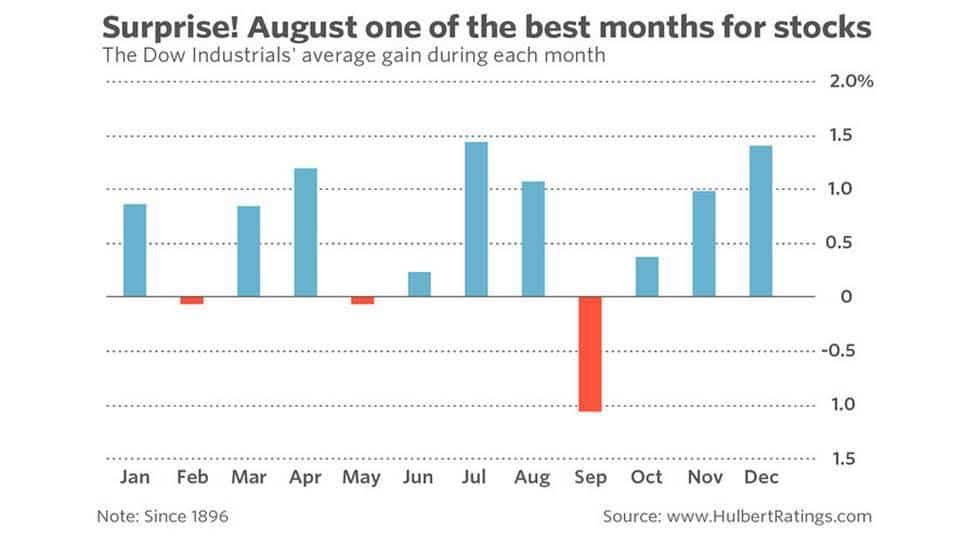

The Trump Effect May be Over and September is often a Down Month for Stocks

While we try to shy away from strictly talking about stocks (unless they are related somehow to weather and the environment) a word of caution about the stock market. Most of Trump’s promises to his “base” have not come to fruition and while U.S. unemployment is at the lowest level in years. (No credit to Trump, may I remind you, but this was set in motion by the Obama administration years ago.) there may be too many people bullish stocks.

Terrorism is rising, there is political uncertainty in Washington and the chart above shows the history of lower stock prices in September. We still like the stocks NEE and TAN as the world turns more towards solar energy. Remember, NEE has been regarded one of the most ethical companies. In the world for 10 years. Nevertheless, a word of caution that If the stock market sector has a correction, so will these stocks.”

by Jim Roemer | Jul 27, 2017 | Commodities

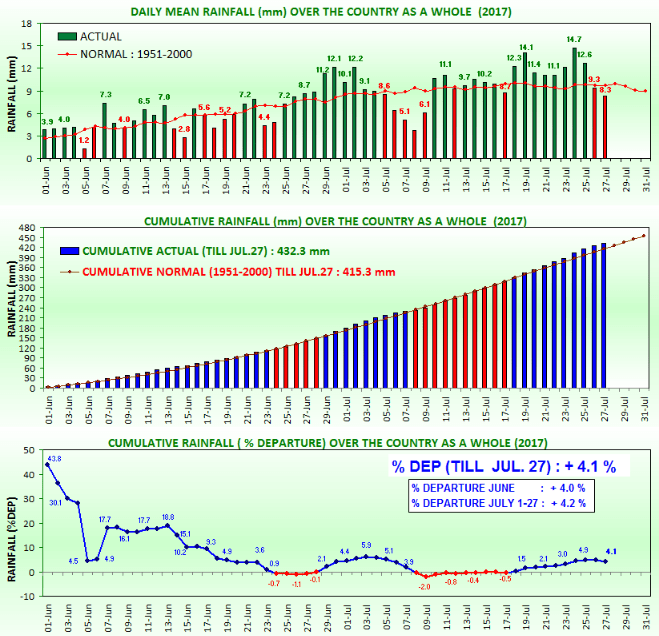

A complete turnaround in SE Asia weather has occured this summer compared to last year. Persistent El Niño conditions in 2015 and 2016 helped force below normal rainfall for India. A dry hot 2015/2016 winter in India furthered poor irrigation levels. This year, rainfall for All-India and the cumulative anomaly is above normal. See below:

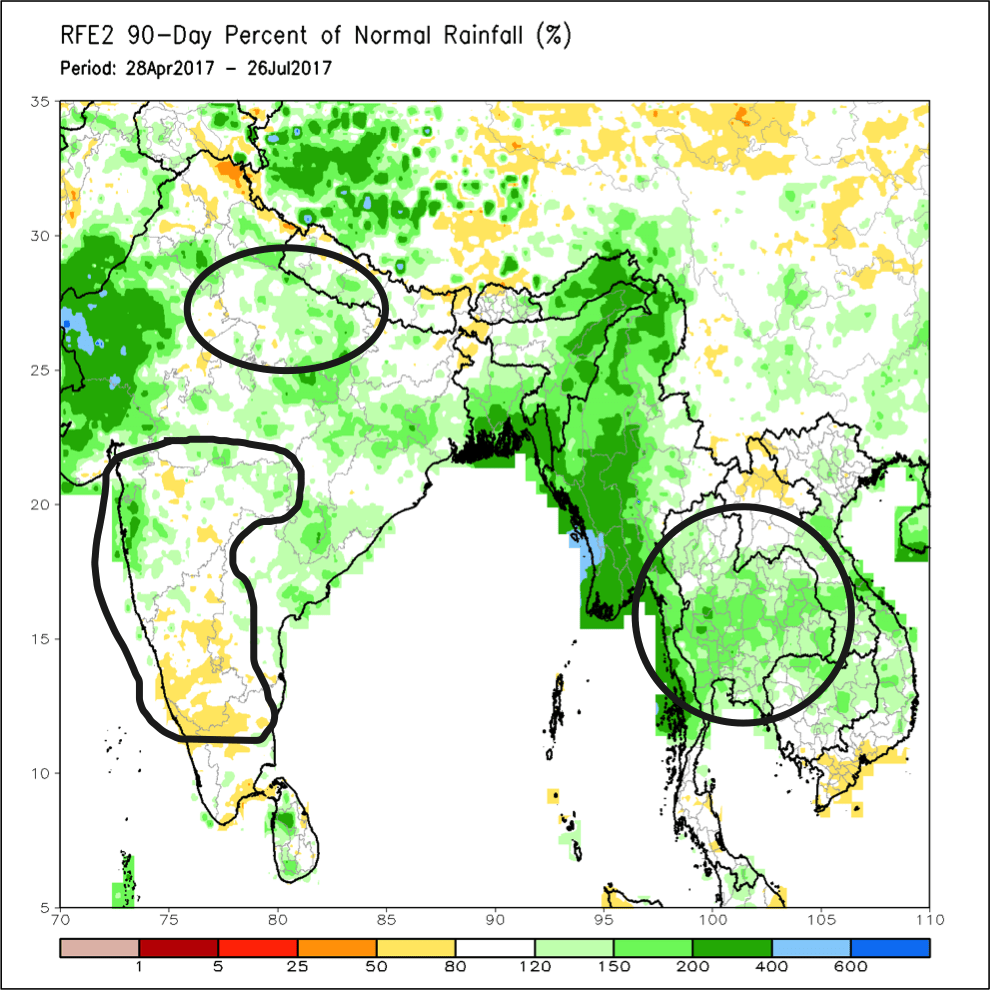

India’s monsoon has shined, particularly in the Northern sugar areas. There are two main areas for sugar production: the Southwest (states of Maharashtra, Karnataka) and the Northeast (Uttar Pradesh). The spatial rainfall anomalies for the past 90 days show near normal to above normal rainfall has occurred so far. Readers should also note that Thailand, a major producer, has had above normal rainfall.

The current outlook for India sugar production is good, but, sugar traders will still be watching the end of the monsoon in India, which runs into October.

Brazil Crush & Fuel Tax

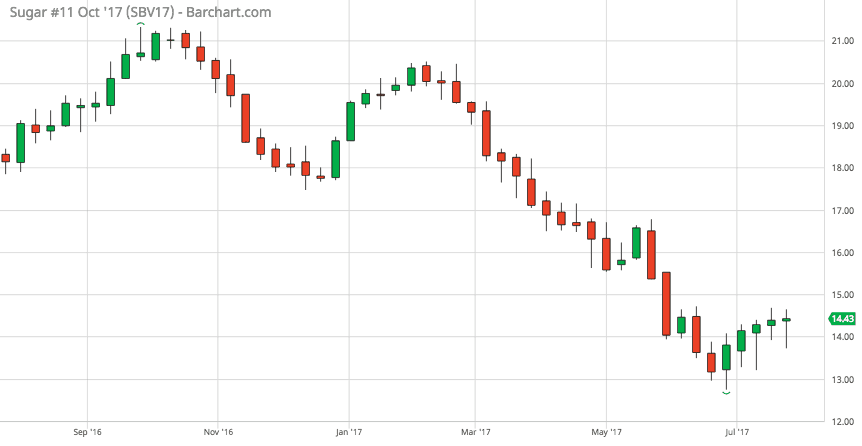

Sugar prices have fallen nearly 33% since early winter. Great expectations of the Brazil crop, which started developing in December, have helped prices decline. See the chart below:

Besides periods of showers in late May, there has been little disruption of the sugar harvest in Brazil. On Tuesday, the Brazilian Sugarcane Association (Unica) released their crush numbers from the first two weeks in July. Production was up 9.1% from last year, with a total of 3.1 million metric tons. The other news from Brazil this week was a reinstatement of the fuel tax. It is expected that the tax should help widen the price spread between ethanol and gasoline. This could make ethanol production more appealing, leading to less sugar cane used for the food industry.

by Jim Roemer | Jul 5, 2017 | Commodities

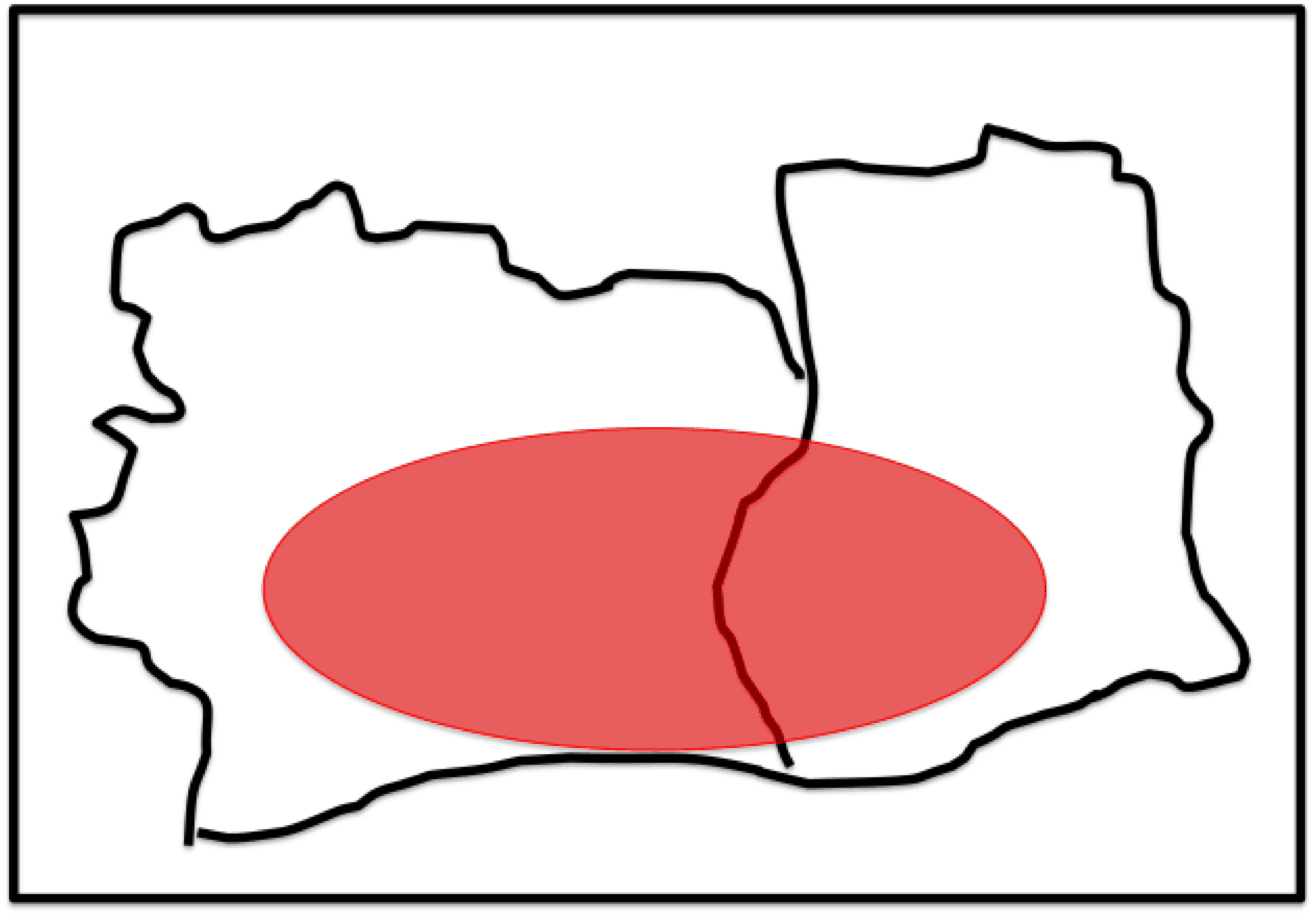

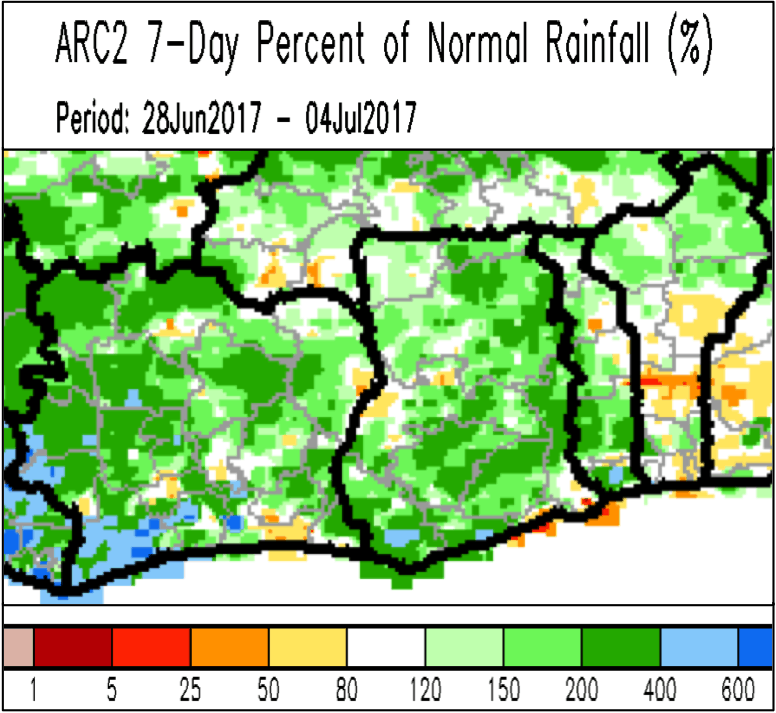

There have been conflicting news stories about the recent weather in West Africa cocoa areas. Nearly 50% of global cocoa production occurs in Ghana and the Ivory Coast. The crops are mainly grown in the area marked with a red circle below.

Too Much Rainfall?

Rainfall has been well above normal the past few weeks. Some news reports mention concerns about it affecting the the harvest and sale of the mid-crop (May-Aug). The roads have been impassible at times. Another worry is black-pod disease caused by a fungus. Too much rain provides better conditions for the disease to occur and spread. June had above normal rainfall, with the past week being particularly wet (+200%-600% of typical rainfall in spots).

SOURCE: NOAA/CPC

On the other side of things is the sentiment that this rainfall is ‘great’ for the developing main crop (grows May-Sept). We’ve had strong rainfall compared to the last few years. The ample soil moisture can be viewed as beneficial, rather than detrimental to the supply/demand outlook. Typically, rainfall dies down in June, as the Inter Tropical Convergence Zone moves north. Precipitation will pick up again in August and September. Traders will be watching to see if too much or too little rainfall occurs. The main crop harvest will set the scene for cocoa prices in the months to come. Only our paid subscribers will receive our proprietary weather forecast and production outlook.

by Jim Roemer | Jun 27, 2017 | Commodities, Forecast, Strategy, Weather

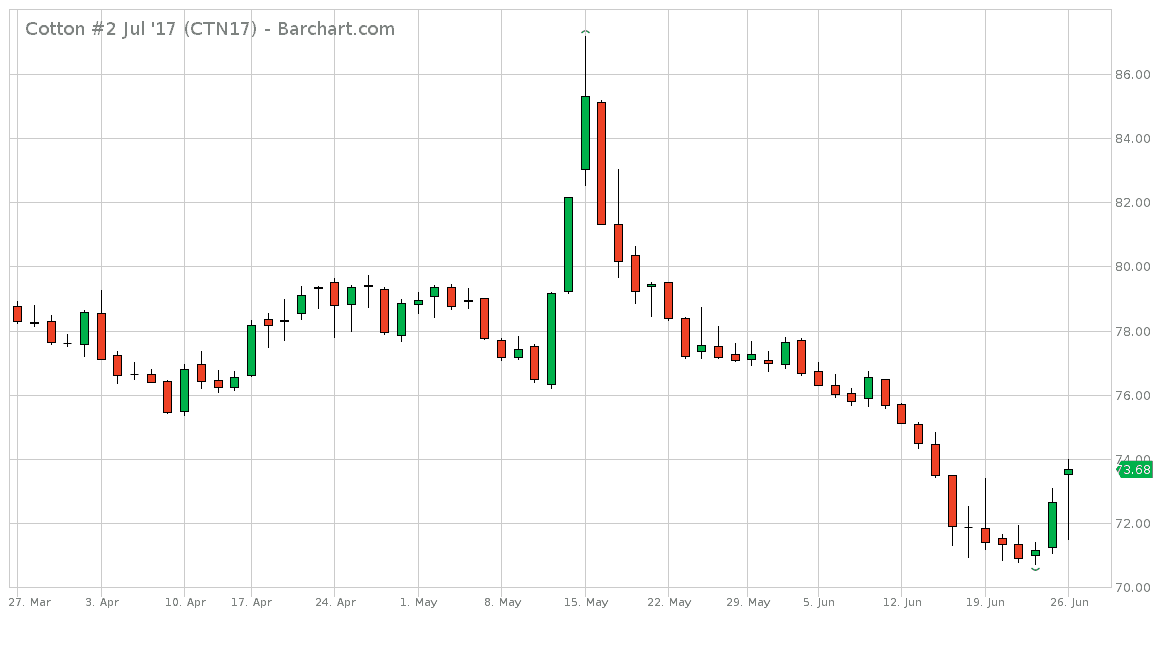

Cotton prices dropped nearly 20% from May highs into late June. July futures prices spiked in May on tight supplies predicted in the USDA report. Great global crop conditions and strong speculative selling then spurred the current collapse.  Credit: Barchart

Credit: Barchart

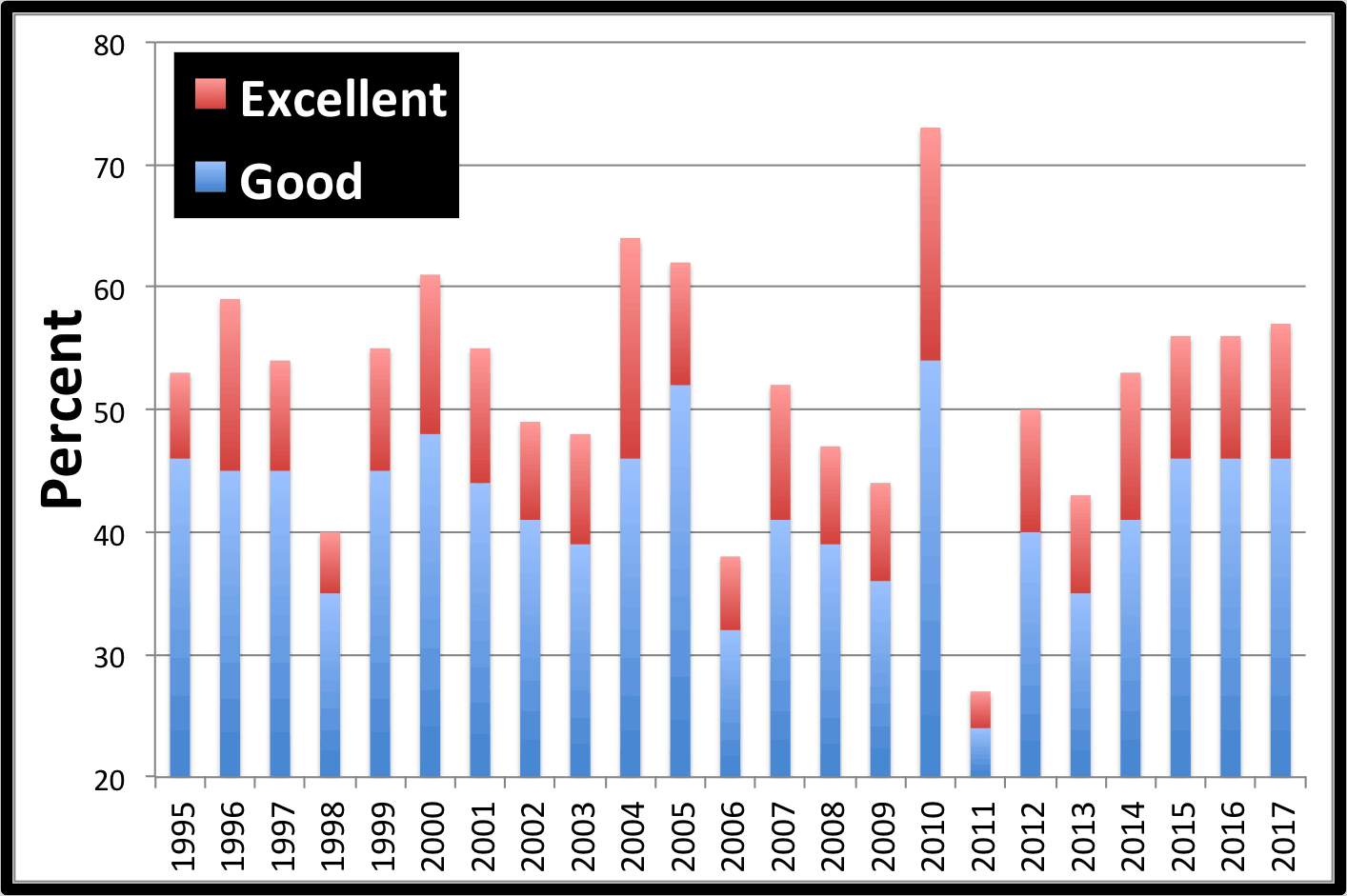

Most notably, India has had a great start to the monsoon (unlike the last few years). Farmers are getting adequate rainfall, aiding in the irrigation already in place. India is the second largest producer in the world behind China. Another country that should have great production is the United States. The latest crop condition report (June 25th) showed 41% of the crop rated good & 11% rated excellent (best since 2010 for this time of year).

Cotton Sales

The oddity of this price drop is that export sales have been very strong. China’s glut of cotton has been dwindling over the past few years. On top of that, China cotton users need higher quality cotton to blend with the old supply.

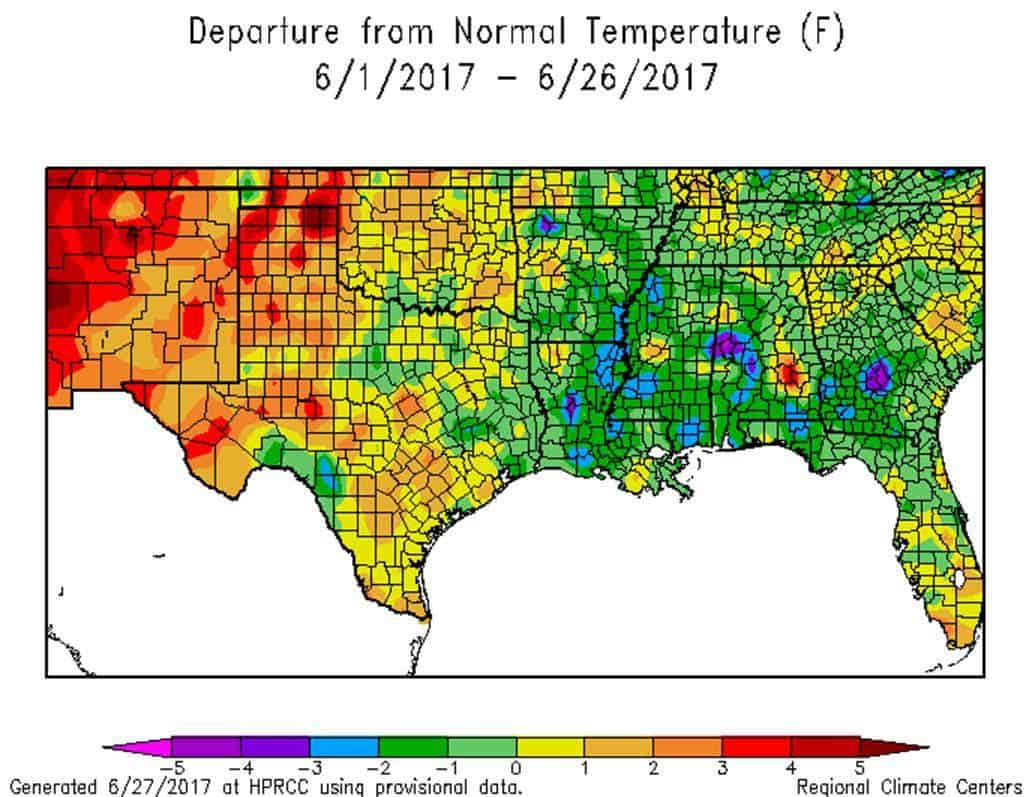

The next fundamental news to watch will be the USDA acreage report on June 30th. With good conditions, most analysts expect this to be friendly for U.S. production. Traders will also continue to watch India and U.S. weather conditions. We have an Indian monsoon report coming to our clients soon, giving the forecast for the rest of the season. The slight drought in Texas cotton areas may begin to be noticed if it continues. See the dryness developing in northern Texas:

by Jim Roemer | Jun 20, 2017 | Climate, Climatech, Commodities, Forecast, Weather

Australia Agriculture to the Rescue!

The month of May was a tough one for portfolio managers in Australia. The S&P 200/ASX fell >2.5% from April highs. The banking industry was mentioned as a potential reason for the sell off. Moody recently downgraded the major Australian banks’ credit ratings from Aa2 to Aa3 due to the mortgage risk they have (over 60% of loans are in residential property). Check out this Bloomberg article for more info:

http://www.smh.com.au/business/the-economy/moodys-move-shines-light-on-australias-home-loan-risks-20170619-gwufh4.html

Another reason for the sell off could have been the lower exports of iron ore over the past year. Cyclone Debbie disrupted production and it had a ripple affect on the economy over the past few months. The storm damaged rails when it hit the northeast shore in early April.

The bright side of the past year has been the agriculture sector. The Australian Bureau of Statistics stated that the sector grew 27% in 2016. This is expected to continue, with wheat, canola, sugar and especially cotton leading the way. Now, however, below normal rainfall may threaten crop production, and thus the Australian economy.

Drought Potential

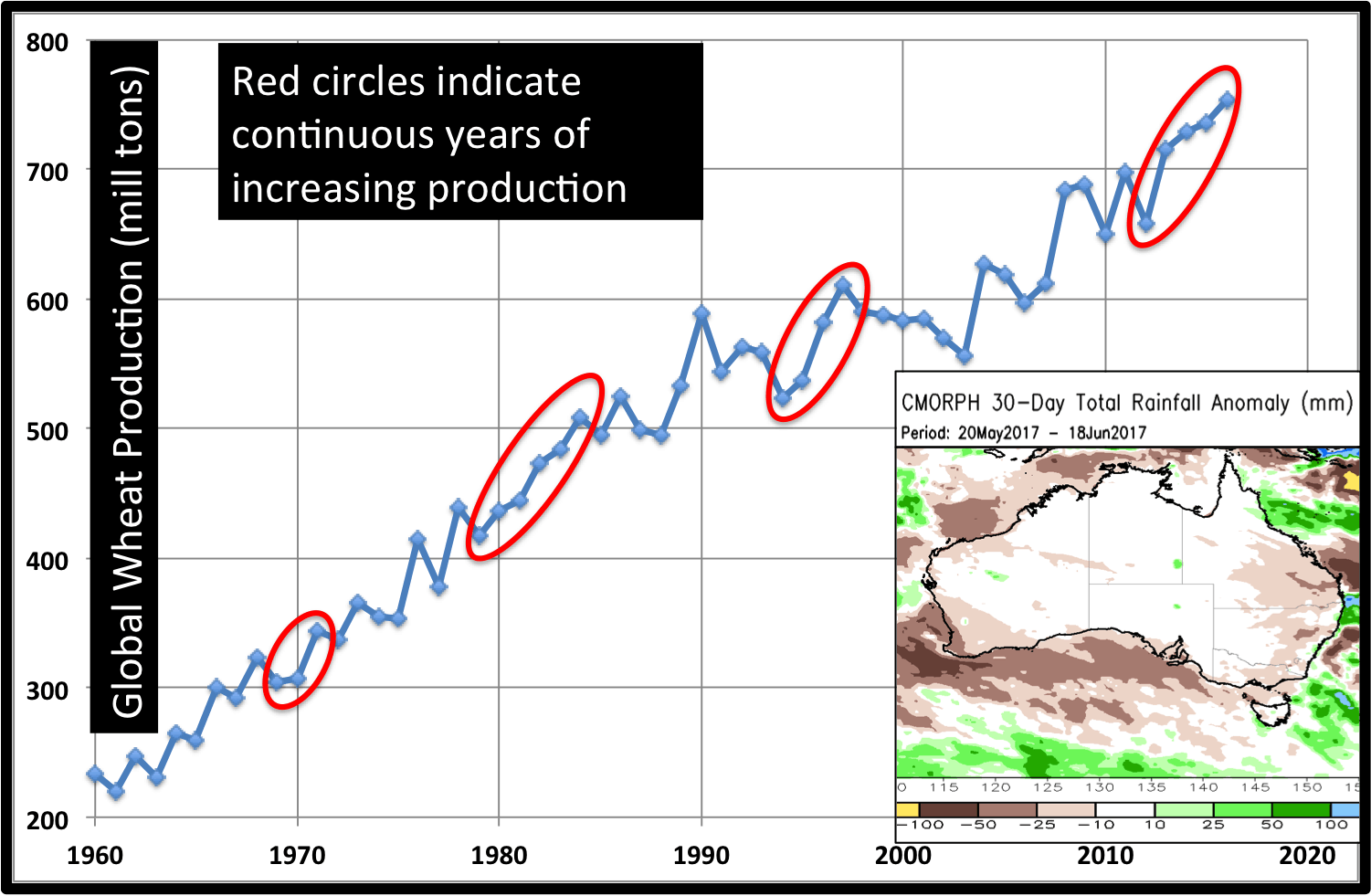

There is talk of drought moving forward for Australia, most notably in the cotton regions in the east. The past 30 days have been slightly dry, (10-50mm below normal). Wheat needs to be planted soon, and requires adequate moisture to do so. Cotton farmers need not worry for a few months. Global wheat production has risen 5 straight years. Australia will need more rainfall to help this trend continue.

Rainfall will become even more important later, from August through December. The major concern is the potential for El Niño conditions during this period. Warmer waters in the equatorial Pacific create greater descent over the Australian continent.

In addition to the El Niño impacts, the Indian Ocean can also affect Australian rainfall patterns. When the Indian Ocean Dipole is in a positive phase (current state), the western Indian sea surface temperature anomalies are warmer than those in the east. This set up usually leads to below normal rainfall over Australia. The questions moving forward are: Will a moderate El Niño form and will +IOD conditions persist?