WEATHER WEALTH SAMPLE CONTENT

HELPING YOU MAKE THE BEST INVESTMENT DECISIONS BASED ON THE WEATHER

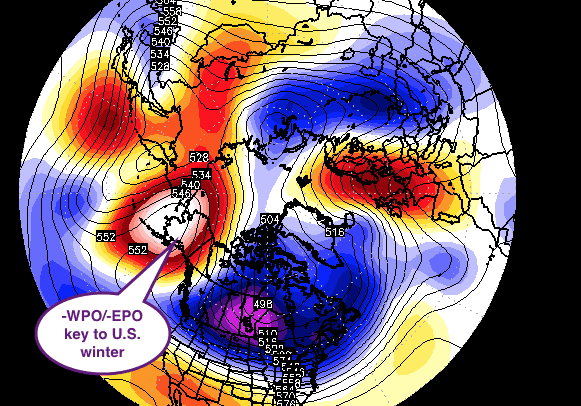

The natural gas market has rallied more than 15% the last 2 weeks due to ideas of a much colder winter and more bullish EIA’s vs last year’s warm winter. We began noticing blocks in Canada 2 weeks ago, that made us adjust our forecast for colder weather and become more in the bullish camp with prices just above $3.00. What will be keys to the winter forecast? Will it warm up after 2 weeks of cold? What these blocks due (-WPO) and (-EPO) are keys. Subscribers to our service will get up to date short and long range weather forecasts, plus invaluable information gauging the psychology of these and many other markets based on the weather.

Chart below supplied by StormVista of teleconnections predicted by mid December

Some of the best skiing in the U.S. will be across the Pacific Northwest and into places in Utah (Snowbird, Utah), etc. the next few weeks. Several more feet of snow will fall from the Cascades and N. Sierras to the Wastach range in Utah making for improved skiing for December. Cold weather will be the rule across New England well into mid-late December favoring improved skiing across Vermont, New Hampshire and Maine. Should be good skiing in the Northeast for Christmas and possibly 1-2 storms in the next 2 weeks.

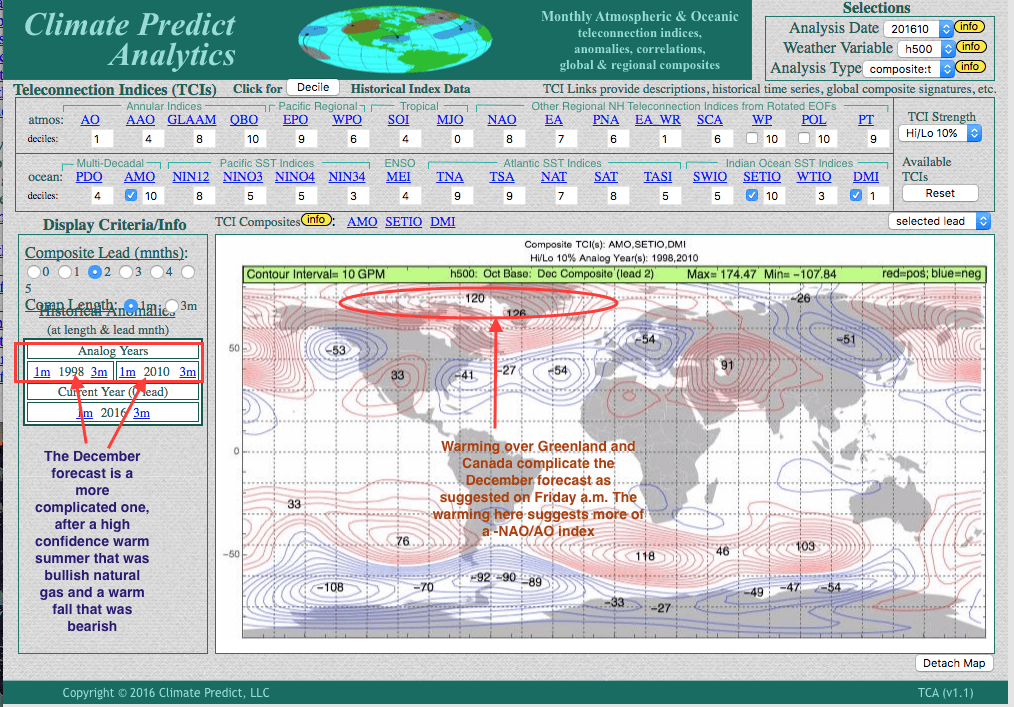

KEY POINT—GLAAM (which has to do with El Nino/La Nina) is acting much more like a La Nina. This is different that I thought 2 months ago. This will have some important implications for cocoa (good crops) , coffee, grains (maybe Argentina dryness later on) and perhaps energy weather in the weeks and months ahead. (more on this over the next week or so).

In the meantime, this also complicates the early winter U.S. forecast (1998 warm winter vs. 2010 a cold one).

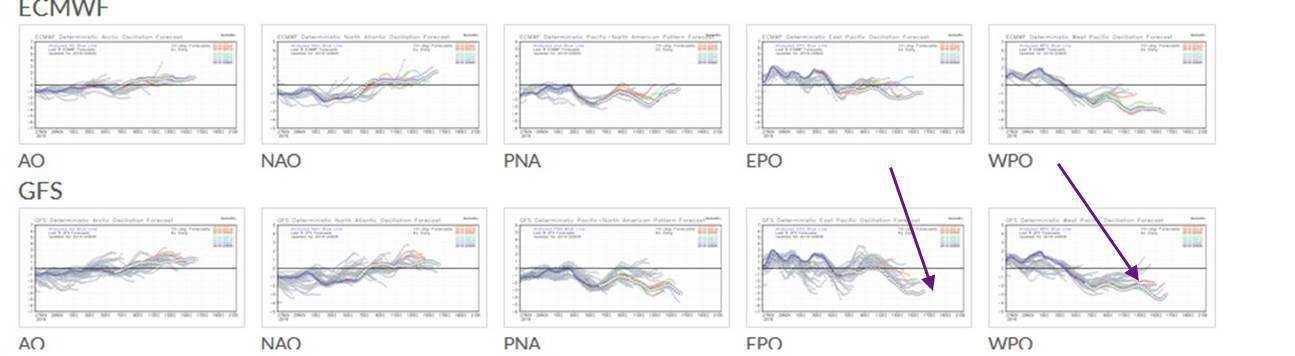

Most studies I have done suggest temporary cold in December and not long lasting. However, given this scneario below, some colder risks will occur in the Midwest and Plains with big time snowstorms the first week to 10 days of December. THE BOTTOM LINE IS, after my high confidence back in October about a collapse in natural gas prices, the market will remain volatile the next couple weeks and possibly supported on breajs, and not as clear cut as I pointed out, weeks ago.

LOOK AT 2 DIFFERENT ANALOGS BELOW

1998 was a very warm December and 2010 was a cold one. Our original analog of 1998 has worked great for world coffee, cocoa, sugar and forecasting the warm summer for natural gas and warm fall. However, until we can dig into this a bit further—some complications and lower confidence has arisen with 2010 (cold winter) also coming up.

THE GRAPHIC BELOW FROM OUR TELECONNECTION PROGRAM SHOWS THE FOLLOWING—

The influence of a -NAO/-AO index on December temps across U.S. natural gas areas, in this case the Midwest and Plains. Notice when the NAO/AO is negative it can make a huge difference in temps.

This complicates our original forecast for a warm December a bit, even though many studies suggest cold weather will be short lived. If and when the -NAO blocks weakens, we will be the first to alert you to potentially overall warmer risks. For now, the trend is a bit colder as discussed early Friday, for December.

By Jim Roemer

Recent dry weather and strong Brazil real responsible for slide in coffee prices with improving Brazil weather.

Off crop year still for Brazil producers.

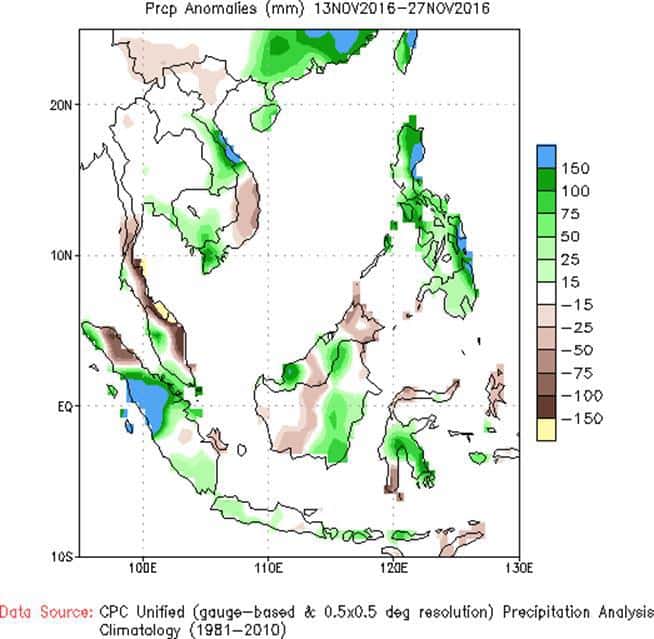

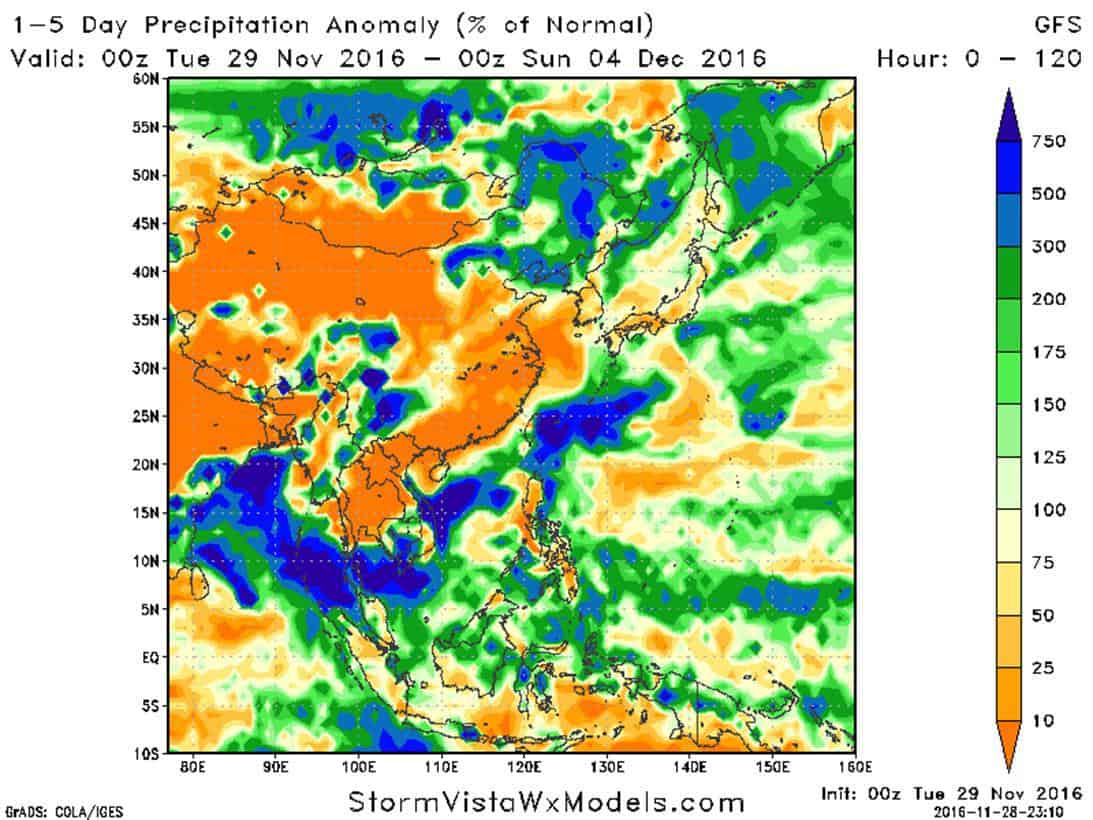

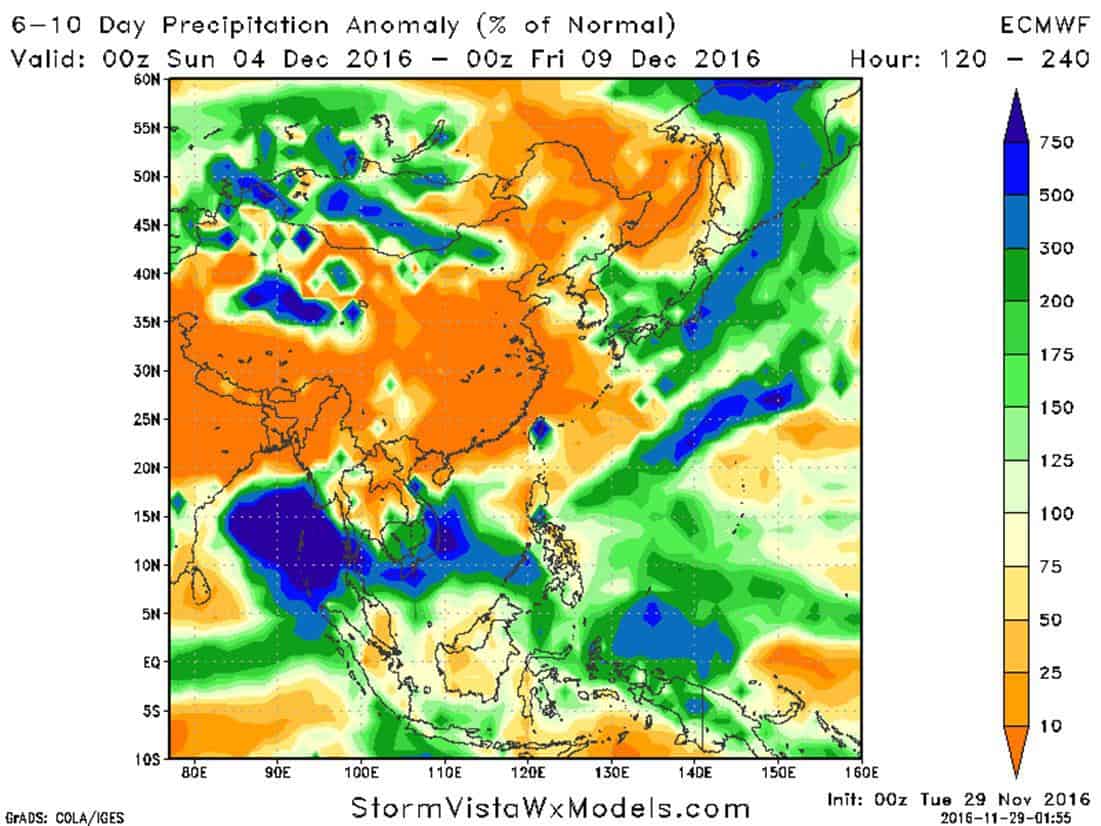

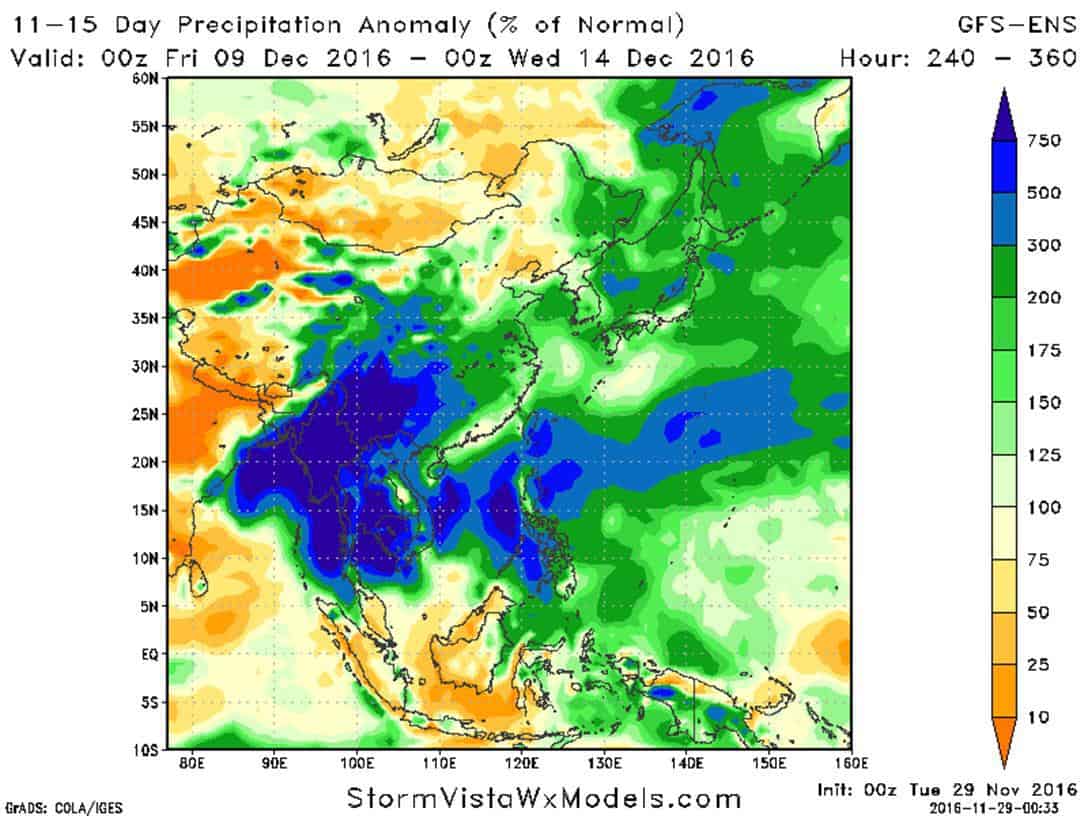

See wetter maps for Vietnam at bottom of the page with 150-400% normal rainfall next 2 weeks slowing the harvest.

Recent dry weather (above) has allowed the harvest in Vietnam to progress but more problems and complications could arise from heavy rains the next 2 weeks.

NOVEMBER 23, 2016

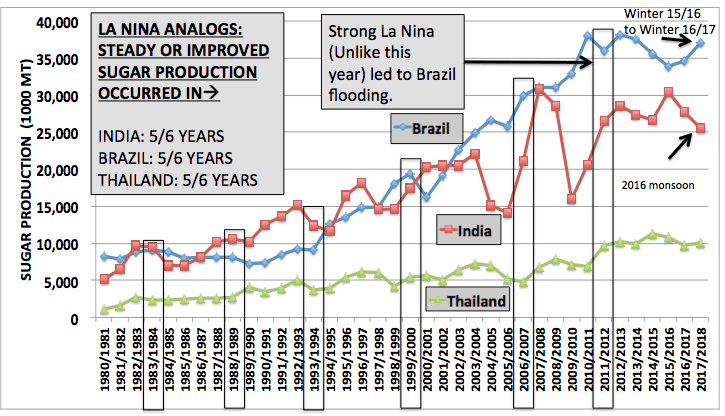

What happens to sugar production after strong El Nino years? This graph shows the production of the top three sugar exporters during these years. Notice the consistent increase in production (5/6 years) in India and Thailand (93/94 only exception, weak El Nino→bad for SE Asia Monsoon). In Brazil, production increased 5/6 years (2011 had flooding, strong La Nina). As we have been forecasting a weak La Nina, this should lead to good sugar production in all three countries. THIS IS A LONGER TERM BEARISH SIGNAL IN SUGAR DISCUSSED IN OCTOBER, 2016

Current Brazil rainfall forecast matches our analogs and overall sentiment.

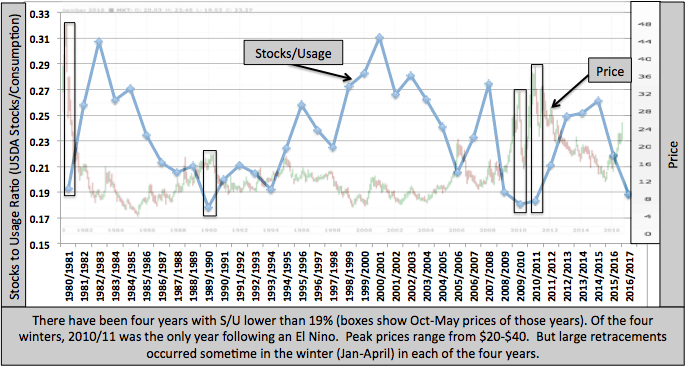

The production and current weather forecast also go along with what we’ve sent weeks ago, with the stocks/usage ratio suggesting a pullback in prices

NEWS SUMMARY:

GLOBAL SUGAR DEFICIT COULD END IN 2017/18 SEASON

“18:34 UK, 21st Nov 2016, by Tanya Ashreena and Mike Verdin

The International Sugar Organization, in its first estimate for the global sugar balance sheet next season, which starts in October 2017, said that “assuming normal weather conditions… fairly balanced global production and consumption come into view”.

This would mean “a possible end of the deficit phase in the world sugar cycle”, after two seasons when global output has fallen short of demand.

“Any easing of price in reaction to expectations of a possible return of the world supply and demand to a more balanced scenario in 2017-18 may be muted,” the ISO said.

The ISO flagged a “critically low level of stocks” which the world would be left with as of the start of 2017-18, after the two deficit seasons which have shrunk stocks by more than 13m tonnes.”

BRAZIL PRODUCTION EXCEEDING EXPECTATIONS

While ethanol prices have been relatively stagnant, the high prices of sugar have attracted refiners to produce sugar rather than ethanol. This is leading to greater production of sugar in Brazil compared to earlier expectations.

“The production mix for the season through Oct. 16 was 46.5% sugar to 53.5% ethanol. A year earlier, the mix was 41.85% sugar and 58.15% ethanol.”

Write to Jeffrey T. Lewis at jeffrey.lewis@wsj.com 10-31-16 0823ET

Copyright (c) 2016 Dow Jones & Company, Inc.

INDIA CONSUMPTION UP AND 7% DECLINE FROM LAST YEAR, BUT LOCAL SUPPLY EXPECTED TO MEET DEMAND.

0810 GMT [Dow Jones] India’s sugar output will likely decline 7% in the new crop season, but availability of the sweetener will remain adequate to meet local demand. The government estimates production to be between 23 million tons and 24 million tons, while the Indian Sugar Mills Association pegs it at around 23.4 million tons for the crop year that runs from October this year.

OTHER TECHNICAL FACTORS

11:40 UK, 21st Nov 2016, by Mike Verdin

“We would make the point that since we talk to most of the discretionary funds, we are pretty sure that none of them is wedded to the bullish story,” the broker said, flagging thoughts that system funds “will be getting out now”. Sell signals to these investors include, from a chart perspective, “the fact that some of the long-term trend lines have been broken”, besides the reversal in fund strategy to selling rather than buying.

“Almost all funds are effectively trend-seekers, so will presumably continue to follow the new trend, and in doing so, confirm it.” A potential market “mistake” was the rally in futures to 23 cents a pound, meaning prices were now where they “should be” at 20 cents a pound. “But if nothing happens to ‘stop the rot’,” in terms of fund selling, “we think that it [the price] could head lower, and maybe much lower.”

HELPING YOU MAKE THE BEST INVESTMENT DECISIONS BASED ON THE WEATHER