European Corn Surges as US Market Eyes El Niño

Jim Roemer’s Corn Overview:

In late May, I turned bearish on US corn while many traders remained focused on strong export demand and the potential geopolitical risk premium from the Middle East conflict. My view was that those bullish factors had already been largely priced into the market. What was being underestimated was the weather.

From a meteorological standpoint, the atmosphere was lining up for one of the most favorable spring planting seasons across much of the Corn Belt in years. Timely rainfall, adequate soil moisture, and the absence of prolonged flooding or planting delays allowed producers to make rapid planting progress. History shows that when crops get planted on time under favorable early-season conditions, yield potential increases significantly. Markets quickly shifted their attention away from geopolitical headlines and back toward the prospect of abundant US production.

What resulted was a sharp 10–15% decline in corn futures, exactly as I anticipated.

The next major catalyst arrives with the USDA Planted Acreage Report on June 30. If planted acreage exceeds expectations, the market could remain under pressure. However, if acreage comes in below expectations or if the report reveals fewer corn acres than traders currently anticipate, prices could stabilize or even rally.

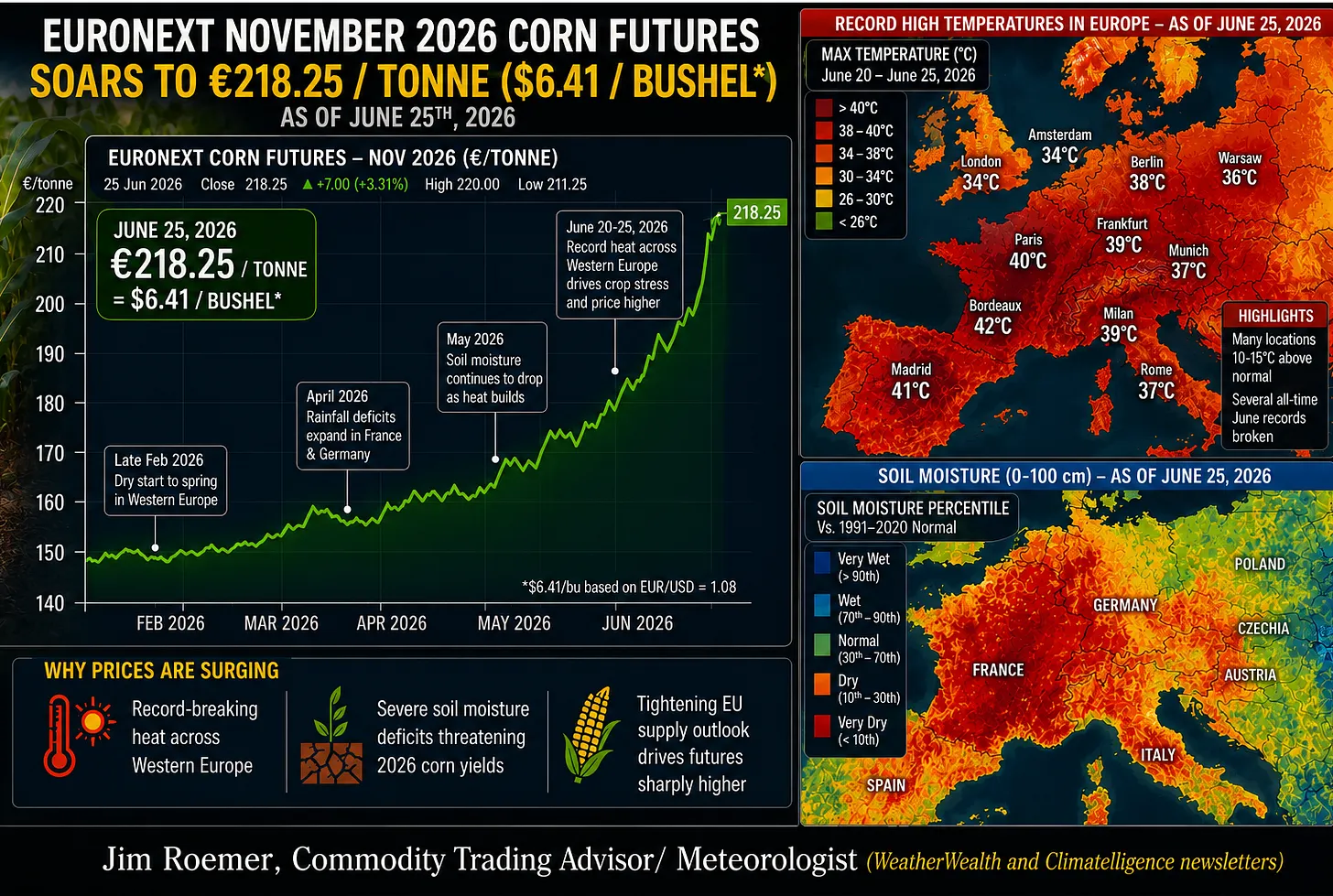

Another developing wildcard is Europe. An unusually intense early-summer heat wave is spreading across major agricultural regions, with temperatures exceeding 100°F (38°C) in parts of France, Spain, Italy, and the Balkans. Heat arriving this early in the growing season increases crop stress, particularly if accompanied by below-normal rainfall. European maize prices have already begun to climb as traders reassess production risks.

The key question now is whether Europe’s weather problems can offset the increasingly favorable US crop outlook. Corn markets often shift rapidly from local weather stories to global supply concerns. While the long-term US production outlook remains favorable, adverse weather in Europe—or later this summer in the US during pollination—could signal that corn has established an important seasonal bottom.

As always, weather remains the single most important variable determining grain prices. Understanding atmospheric patterns before they become widely recognized is often where the greatest market opportunities emerge.

To find out more about our global commodity weather forecast and market outlook, please upgrade below. (If you are already a Climatelligence subscriber, you can access our full report here.

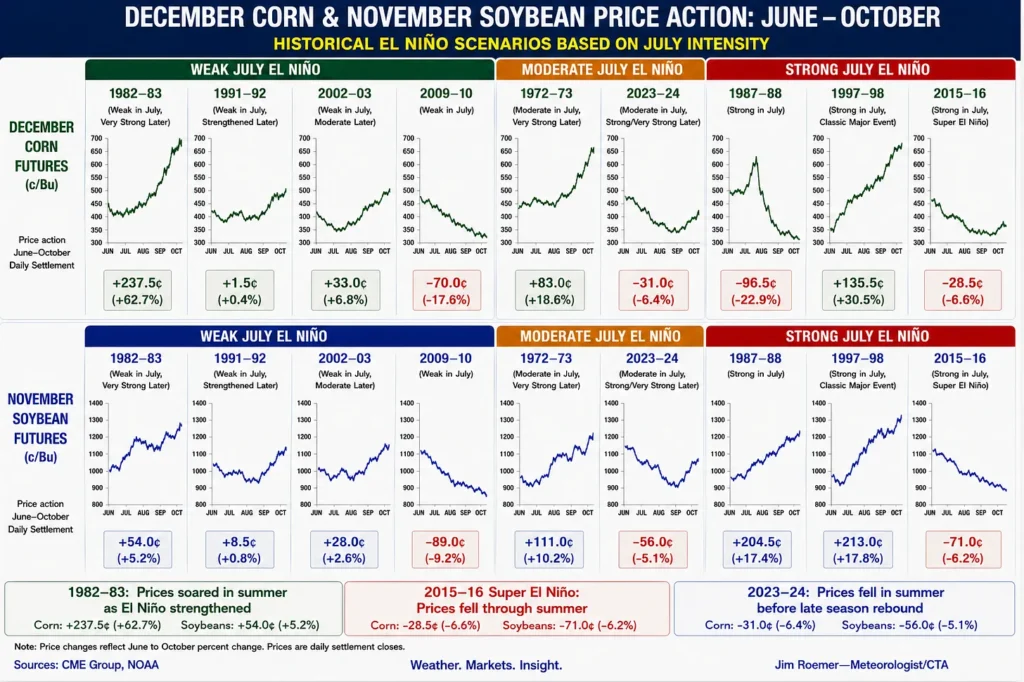

What About El Niño?

Not all El Niño events have the same impact on US corn. Strong El Niño events often leave behind abundant spring soil moisture and, as they weaken into summer, tend to produce cooler and less stressful conditions across portions of the Midwest. This generally favors above-trend corn yields and can keep prices under pressure.

Weak El Niño events, however, are much less predictable. As they fade, the atmosphere can become more volatile, increasing the risk of summertime heat ridges and localized drought during the critical pollination period in July. In those years, weather markets can quickly add a significant risk premium to corn prices.

For farmers, the decision to hedge depends on both weather risk and current price levels. After the recent decline in corn prices and with excellent crop conditions across much of the Corn Belt, many producers may want to consider incremental hedges—particularly if the USDA’s June 30 acreage report confirms a large planted crop. However, maintaining some upside flexibility is also prudent. Weather during pollination remains the single most important determinant of final yields, and a shift toward hot, dry conditions could trigger a sharp summer rally.

The bottom line: favorable weather has driven prices lower, but the weather market is far from over. July remains the most important month for determining whether this year’s crop fulfills its yield potential—or surprises the market. Some heat is likely next month, but I am not convinced we are looking at a major drought that would result in a massive bull market, such as what is currently happening in the European market.

We appreciate your interest and look forward to helping you gain a better understanding of the powerful connection between weather and global commodity markets.

Jim Roemer, Scott Mathews, and the Best Weather Team

Mr. Roemer owns Best Weather Inc., offering weather-related blogs for commodity traders and farmers. He is also a co-founder of Climate Predict, a detailed long-range global weather forecast tool. As one of the first meteorologists to become an NFA-registered Commodity Trading Advisor, he has worked with major hedge funds, Midwest farmers, and individual traders for over 35 years. With a special emphasis on interpreting market psychology, coupled with his short and long-term trend forecasting in grains, softs, and the energy markets, he commands a unique standing among advisors in the commodity risk management industry.

As a veteran in the commodity futures industry, Scott’s career has taken him from learning the business on Continental Grain’s New York trading floor and later co-directing Citicorp’s entry into the energy commodity business in the bank’s brokerage subsidiary Citicorp Futures Corporation.

As an early participant in the weather derivatives market, Scott consulted and advised the Chicago Mercantile Exchange in designing and launching the first weather-indexed futures contracts for temperature, precipitation, and hurricanes. For nine years, he produced Weather to Buy or Sell – a feature that appeared in the weekly edition of The Wall Street Journal. This “infomercial” covered the CME weather futures activity.