Readers who recall our comments 6-8 months ago learned about El Niño’s demise along with a positive Indian Dipole. These, and other teleconnections, have led to world wide bumper crops in sugar. Recent market prices have temporarily painted a positive technical picture due to some renewed dryness in Brazil. Firming oil prices have also contributed to some bullishness, as explained in the next paragraph.

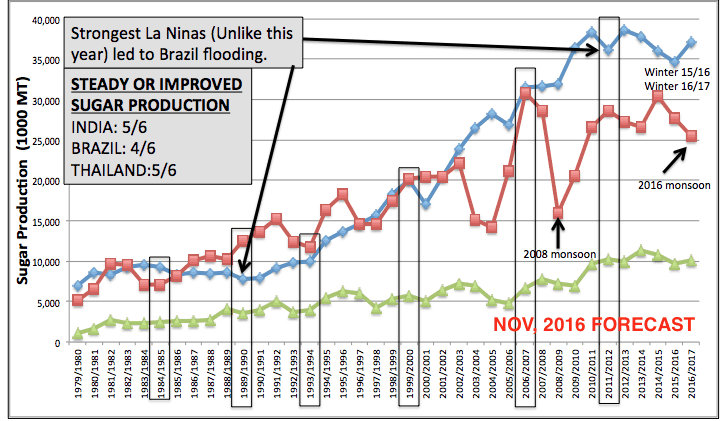

THE CHART ABOVE IS OUR NOVEMBER 2016 FORECAST FOR A REBOUND IN WORLD SUGAR PRODUCTION. THIS PREDICTION WAS CORRECT. IT EXPLAINS WHY SUGAR HAS FALLEN FROM THE EL NIÑO DRIVEN HIGH PRICE LEVELS AND GLOBAL WEATHER WOES IN THE LAST COUPLE OF YEARS.

At times, higher petroleum product prices, specifically gasoline, can impact sugar. The relationship involves growers diverting more Brazilian sugar cane for ethanol production. This reduces the quantity of sugar sold to the food industry. If the August gasoline rally prompted the cane/ethanol scenario, it seems to have run its course as a sugar fundamental. In the third week in August, the hurricane driven rally in gasoline was solely a “knee jerk” response pegged to Harvey. It was a very short-lived move. Supply fears caused the immediate over reaction. Now, back to sugar:

A sharp decline in China’s sugar production in recent years prompted government intervention. They imposed heavy tariffs on imports to protect the country’s less-efficient, and noncompetitive, sugar industry. As a result, China’s imports fell this year because sugar users turned to the country’s huge stockpiles for supplies.

Société Générale recently raised its estimate of world sugar production to 179.5 million tons for the marketing year 2017-18. This would be a 5.5% increase from the prior year. Hence, the bank now foresees a global surplus of 5.3 million tons, up from its earlier estimate of 4.5 million tons. The higher production and surplus projections are largely due to favorable weather in India. Meanwhile, Brazil, is expected to produce a record amount of sugar in 2017-18.

The key, when it comes to advising hedge funds and traders, is to predict weather ahead of the crowd. In our consultation practice, we cover how weather will constrain or improve production in both key importing and exporting countries. This is what we do best. Knowing climate/weather can often influence a country’s import/export policies. Such knowledge can often inspire them them to reconsider or re-frame certain political decisions. In the case of sugar, we monitored weather in no less than 3 countries last winter and spring using CLIMATECH to predict the 20-30% decline in sugar prices.

Rainfall Impacting Indian Sugar Crop

The map shown above indicates greater-than-normal rainfall (green) in South Asia. The higher precipitation levels in western India have prevented any major downgrade in this season’s crop. Expectations for a more normal Indian Monsoon have kept prices under bearish pressure for months.