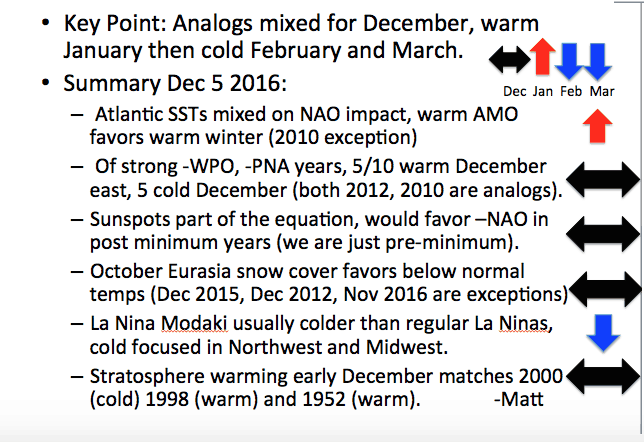

JANUARY COLD TURN COLDER AND STORMIER–BUT ORIGINAL STUDIES, SAY OTHERWISE

A weakening La Nina (which was not really strong to begin with), combined with fluctuating global ocean temps has created a wide variety of weather across the U.S. since December. The east, for the most part has been warm, while the best December ski season in years has blessed the west.

Normally, to see what we call a negative NAO/AO index (warm blocks over the Arctic and Greenland) that can cause consistently cold, snowy weather in the Midwest and Northeast, we need to see warming some 10-30 miles up in the stratosphere. We have not had that, so as a result, computer models have had their greater share of errors this winter. However, based on what I am seeing, a colder January outlook appears possible much of the U.S. However, my confidence in the winter forecast is NOT NEARLY as high as the last few years due to various factors related to teleconnections and La Nina, bouncing around. The January 2004 analog potentially may be a good one. The NAO/AO index could still go negative even without the warming aloft we talked about. This is what happened in 2004 with big western December snows and some similar teleconnections around the globe (To learn more about Teleconnections, go to our Climatech page https://www.bestweatherinc.com/products/ )

However, this cold scenario is in contrast with our original long range forecast made last October (see below) for a mixed December, warm January and cold 2nd half of the winter. Hence, trading the energy markets on weather right now is going to be more difficult and risky than normal.

Red area is warm; blue area cold and black mixed. Our original forecast for U.S. natural gas areas vs other more recent colder studies

Our original winter forecast for U.S. natural gas areas made in October

COFFEE

Along the equator, La Nina has really not gotten going too strongly. In fact, ocean temperatures off the coast of Peru and Ecuador are warmer than normal. With a warm ocean pool also off the coast of NE Brazil, this may set the stage for a few weather related problems to the Brazil coffee crop after a great crop last year.

A recent BLOG I posted discussed the differential in prices between Arabica blends (traded in New York), and Robusta blends (grown in Vietnam, Indonesia and NE Brazil and traded in London). I have been bullish Robusta coffee for more than a year due to global weather issues. Now we can see some developing dryness in some key Arabica coffee areas. Though not a major concern right now, some research I have done suggest off and on dryness into February that may compromise just a bit the 2017 crop.

TRADING COMMODITIES CONSERVATIVELY THROUGH ETF’S

ETF’s are a conservative way to get into the commodity game, as opposed to futures that have large margin requirements, inherent risk, etc. A novice commodity investor can trade through your stock brokerage account. While the weaker Brazilian Real, brought on by fears of a weaker Brazil economy and Trump’s trade deals, has pressured coffee some 25% in recent weeks, a trader can look to buy the coffee ETF (Jo) for the next 2 months risking maybe 7% on this trade.

Dryness (red) is developing in Brazil’s coffee areas after a good early start. This market may be oversold