In this Report from January 8, 2023

Introduction: Video about the Pineapple Express, La Niña, and the record-warm weather

History of the cattle industry and how the Plains drought has created a major bull market

Why the bear market in coffee has resumed

The historic collapse in winter natural gas prices

Argentina drought regaining market attention

Weather Wealth Trade Ideas (always bottom of my reports)

Introduction: Watch the Video

History of the cattle industry and Plains drought

The growth of the cattle industry in the United States in the nineteenth century was due to the young nation’s abundant land, wide-open spaces, and rapid development of railroad lines to transport the beef from western ranches to population centers in the Midwest and the East Coast.

The Europeans who first settled in America at the end of the 15th century brought longhorn cattle with them. By the early 19th-century cattle ranches were common in Mexico. At that time Mexico included what was to become Texas. The longhorn cattle were kept on an open range, looked after by cowboys called vaqueros.

In 1836, Texas became independent, and the Mexicans left, leaving their cattle behind. Texan farmers claimed the cattle and set up their own ranches. The beef was not popular so the animals were used for their skins and tallows. In the 1850s, beef began to be more popular and its price rose to make some ranchers quite wealthy.

Post-Civil War cattle drives from Texas north to railroad depots in Missouri, Kansas, and Colorado were a necessary part of the American economy in the late 19th century. The nation’s growing demand for beef, coupled with the concentration of beef cattle in Texas, led that state’s ranchers to organize cattle drives to bring herds north to railheads so they could be shipped to slaughterhouses in Chicago and other cities.

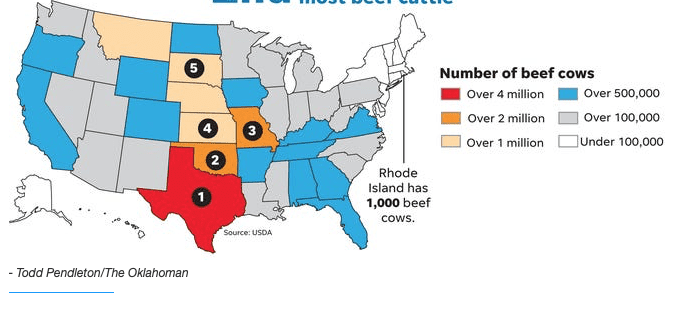

The United States was the largest producer of beef in the world in 2022 followed by Brazil and China. The United States, Brazil, and China accounted for roughly 51% of the world’s beef production. The United States accounted for roughly 21% of the world’s beef production in 2022.

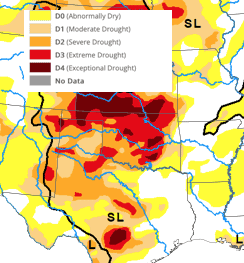

Plains drought and recent cattle on feed report bullish but the market has already seen a stellar rally

The most recent USDA Cattle on Feed report confirmed the cattle herd is continuing to shrink, and high beef prices will likely be with consumers for some time.

Cattle in feedlots came in at 98% of a year ago. High input costs and, more importantly, persistent drought conditions in the western half of the United States are a one-two punch that cow calves and backgrounders have experienced.

The most weighted variable to feed costs is the weather. In most years, weather determines if a bumper crop is to be had or if supplies will be limited and potentially rationed.

High input costs are impacting the marketing and processing of cattle. The drought had a significant impact on pasture and rangeland this summer, especially in the West and the Southern Plains. When drought causes pasture conditions to decline, heifers (female cattle that have not borne a calf) that would typically be kept as breeding replacements are instead placed into feedlots for eventual slaughter. High input costs have been another obstacle to farm profitability and have incentivized cattle producers to market more cattle.

Seasonality and technical picture for cattle prices

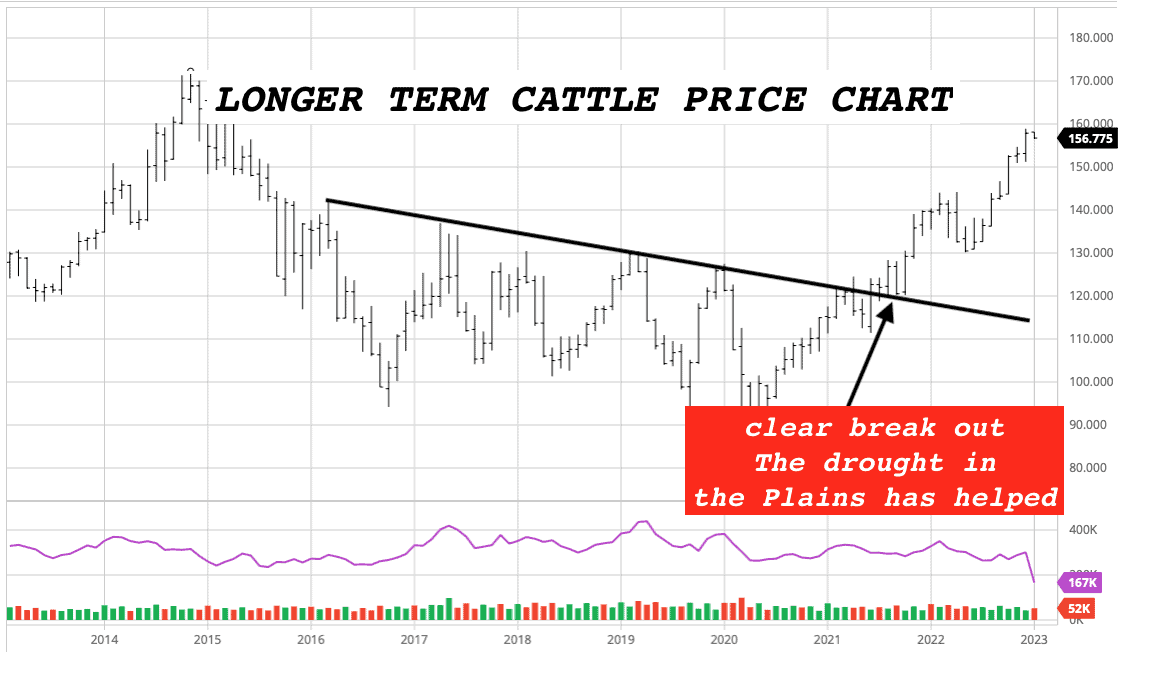

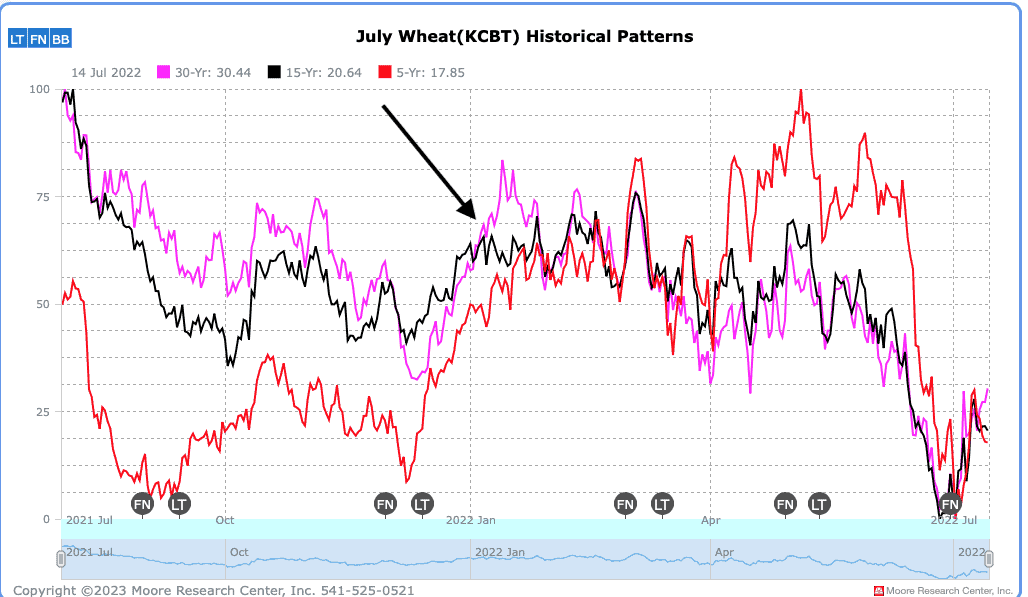

I have so many other markets to follow, I really have not advised even once in this market. One can see on the longer-term price chart (third image below, second chart) how prices clearly broke above resistance last summer in late 2021 as cattle supplies began being affected by a multi-year drought.

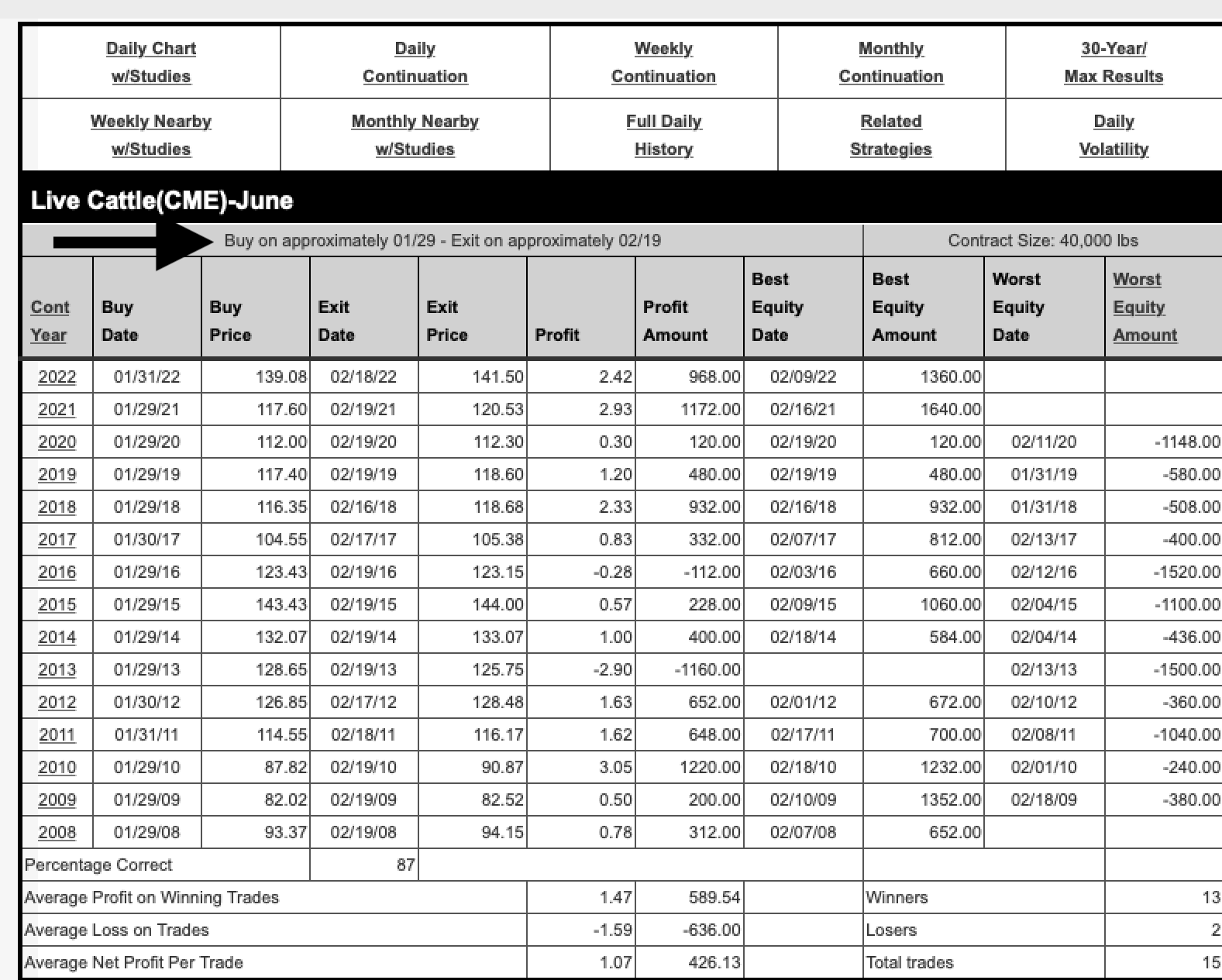

Cattle prices by late January have rallied in 13 of the last 15 years into mid-February.

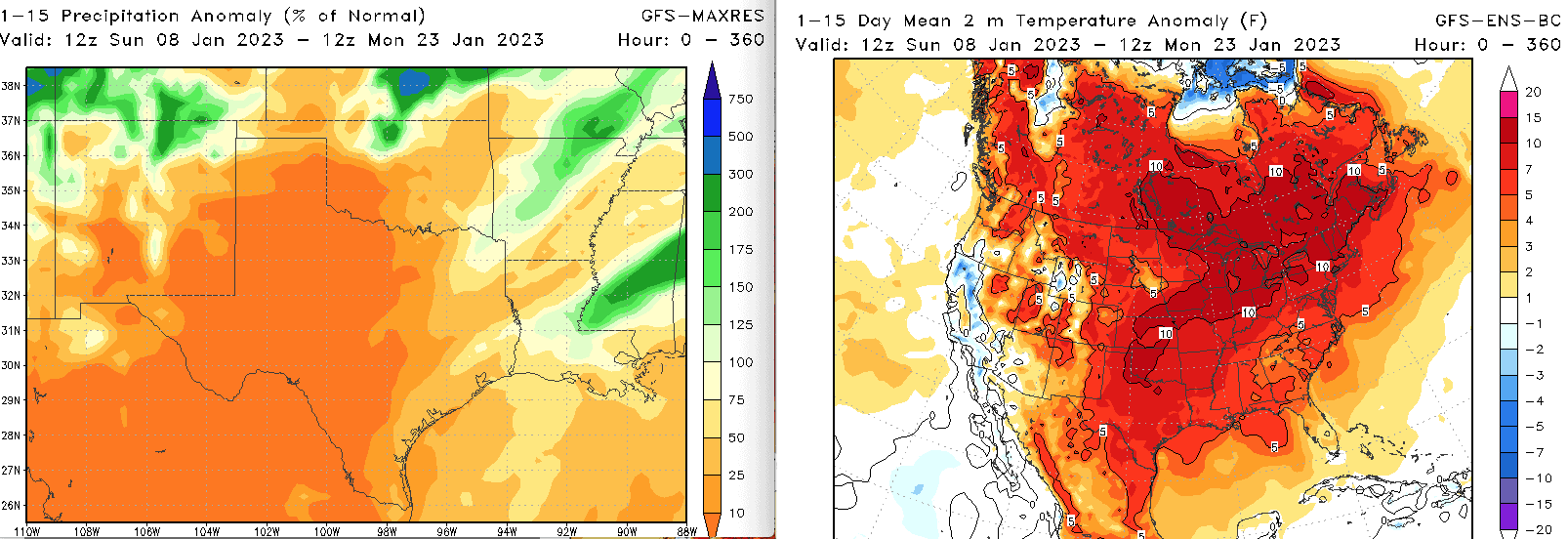

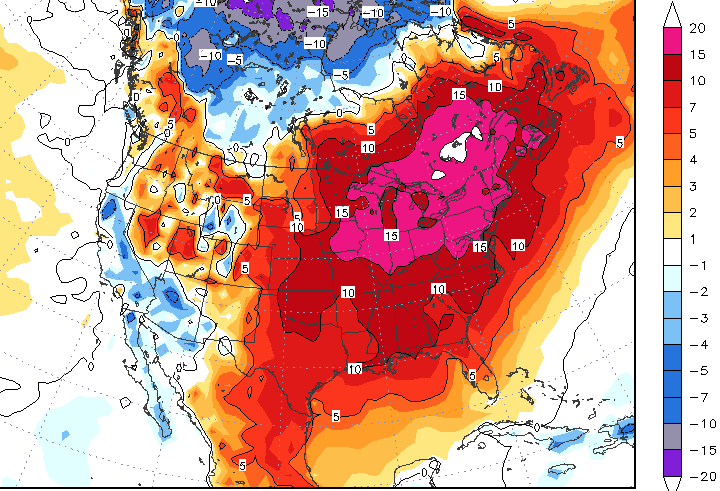

Conclusion: While I have no specific advice in the cattle market I feel that July KC wheat prices may have bottomed for now given the drought in the Plains, the recent freeze 2 weeks ago, and this big-time warmth you see (map to the right)

Drought worsening for Plains wheat as La Niña holds on, for now. Notice the extreme warmth the next 2 weeks

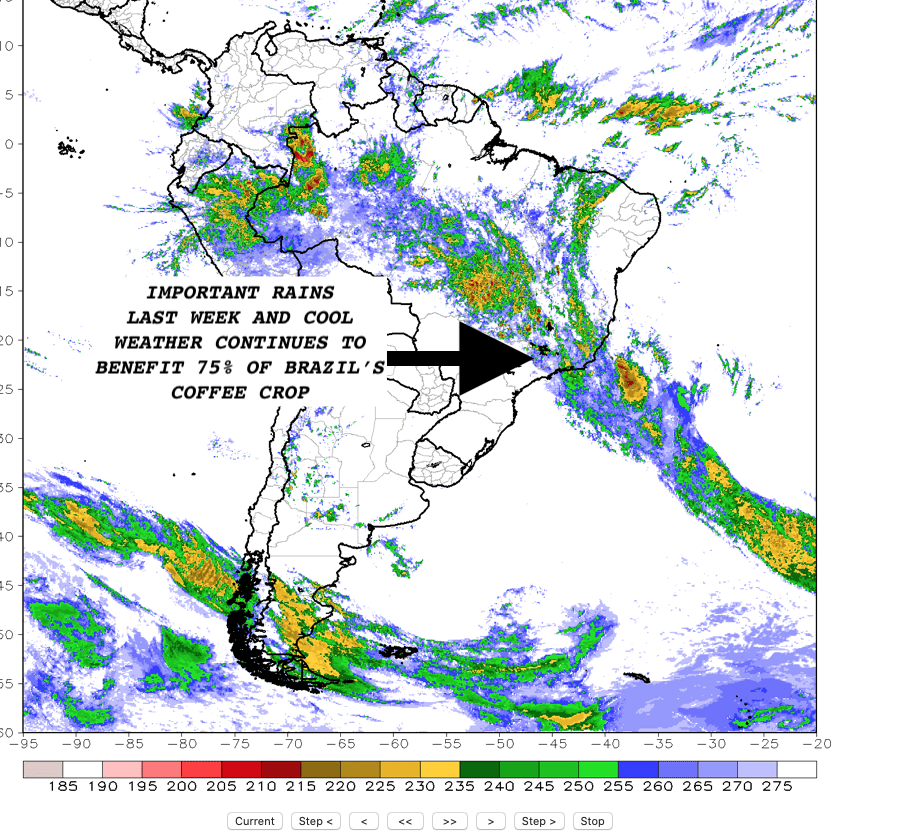

Why the bear market in coffee prices has resumed

The weaker Brazil Real, improved crop weather, and warm global weather pressured coffee prices again last week. Remember, warm winter weather reduces global coffee demand.

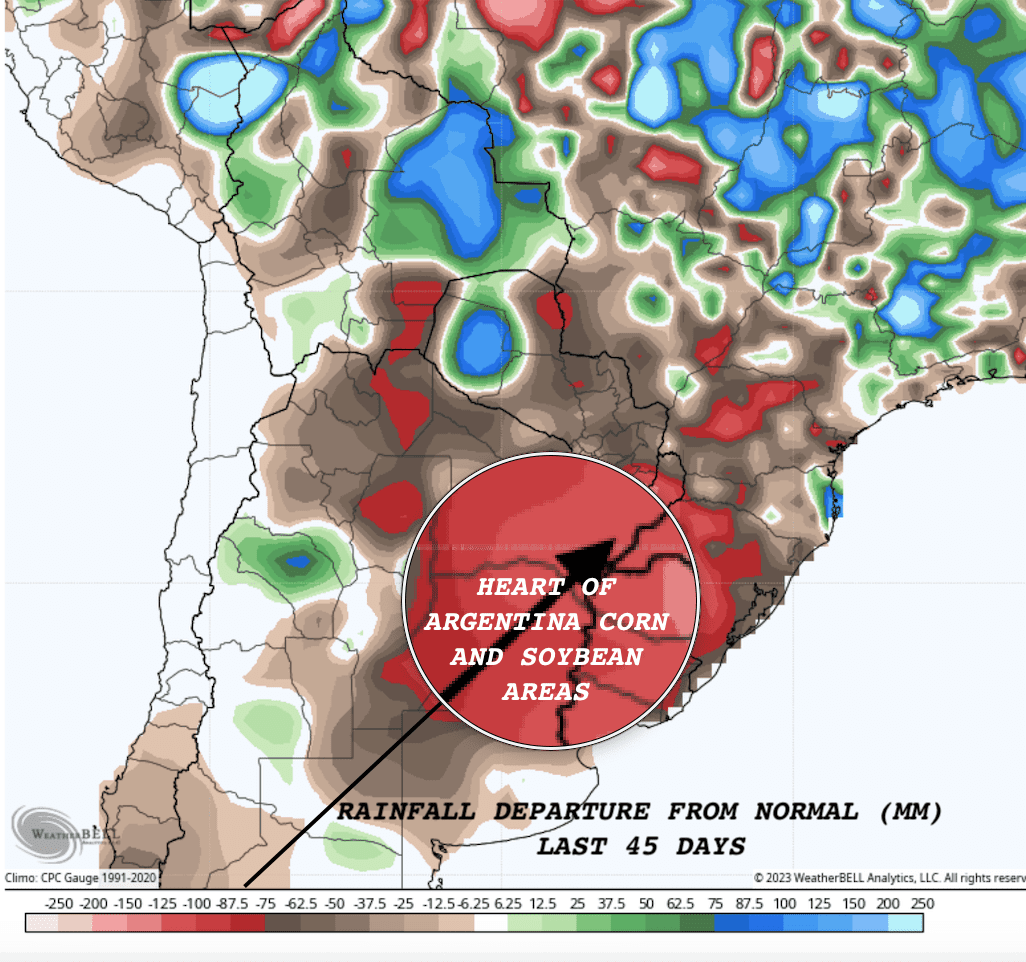

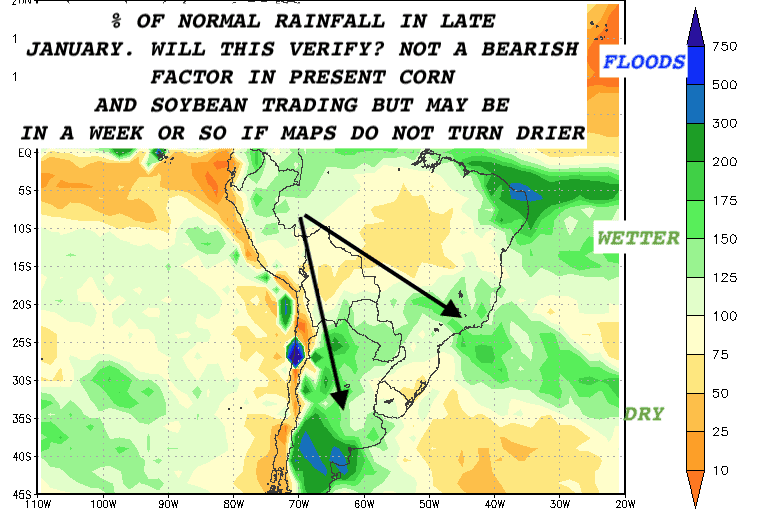

Argentina drought regaining market attention in soybeans

This is a critical time for Argentina’s corn pollination and for the early stages of soybean development in Brazil. You can see the extreme dryness and temps this week close to 40 degrees C (100 F) creating some excitement again in the grain market.

While a long way off (10 days or so from now), most models are increasing rainfall for the drought areas. Will this only be temporary? Stay tuned. Right now, corn and soybean crop prospects are falling sharply in Argentina and far southern Brazil.

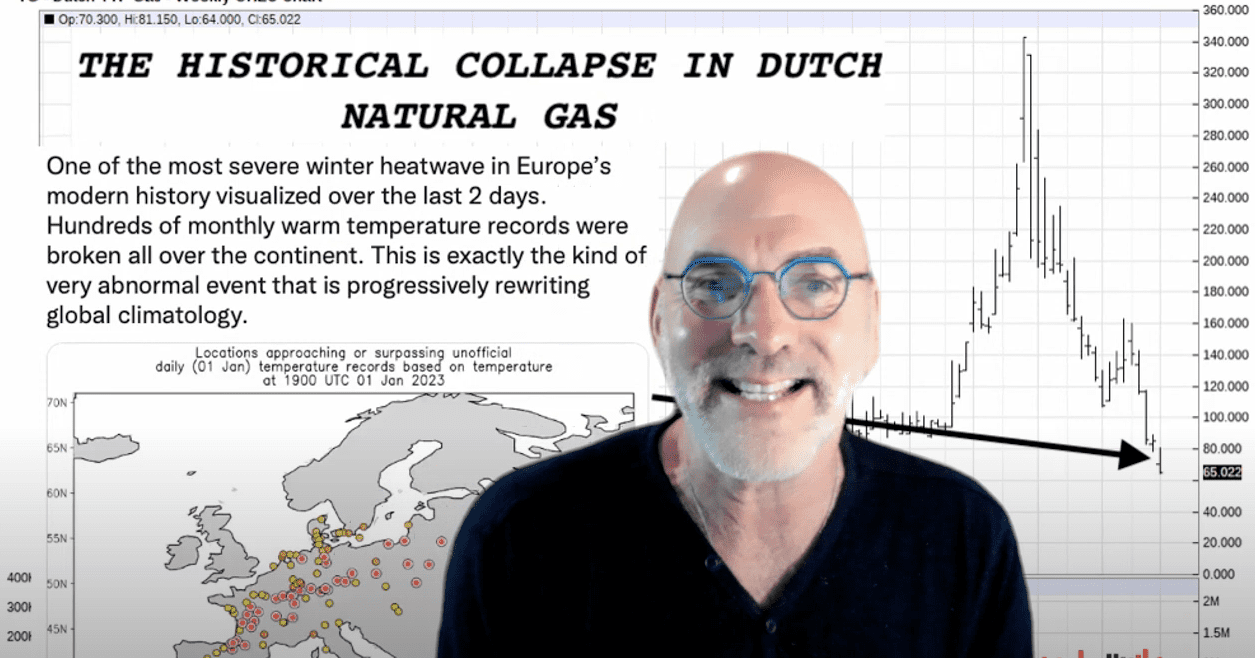

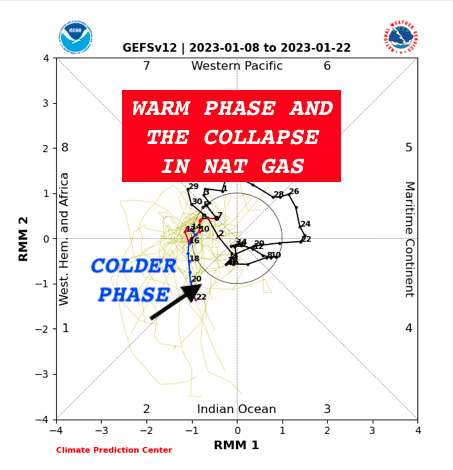

The historic collapse in winter natural gas prices

We already had the huge price break in natural gas prices I was expecting due to record-warm European weather and the warm late December and early January in the U.S.

The return of cooling over the stratospheric, combined with a warming planet and oceans for years retreated the polar vortex far to the north and helped pressure natural gas some 50% in less than three weeks.

This was our best call of the winter– (see the blue-cooling stratosphere). This helped to retreat the Polar Vortex following the historic Buffalo (NY) blizzard. Natural gas prices were trading close to $7, two-three weeks ago before this major collapse I predicted. However, honestly, while I have been bearish, I was surprised to see prices fall below $4.

|

As we get deeper into January and early February it is possible that a slightly colder weather pattern will return for the Midwest and/or Northeast U.S. This is due in part to the movement of the MJO.

However, look how warm it looks first in the next 2 weeks. Some of this has already been built into the collapse of natural gas prices.

WEATHER WEALTH TRADE IDEAS

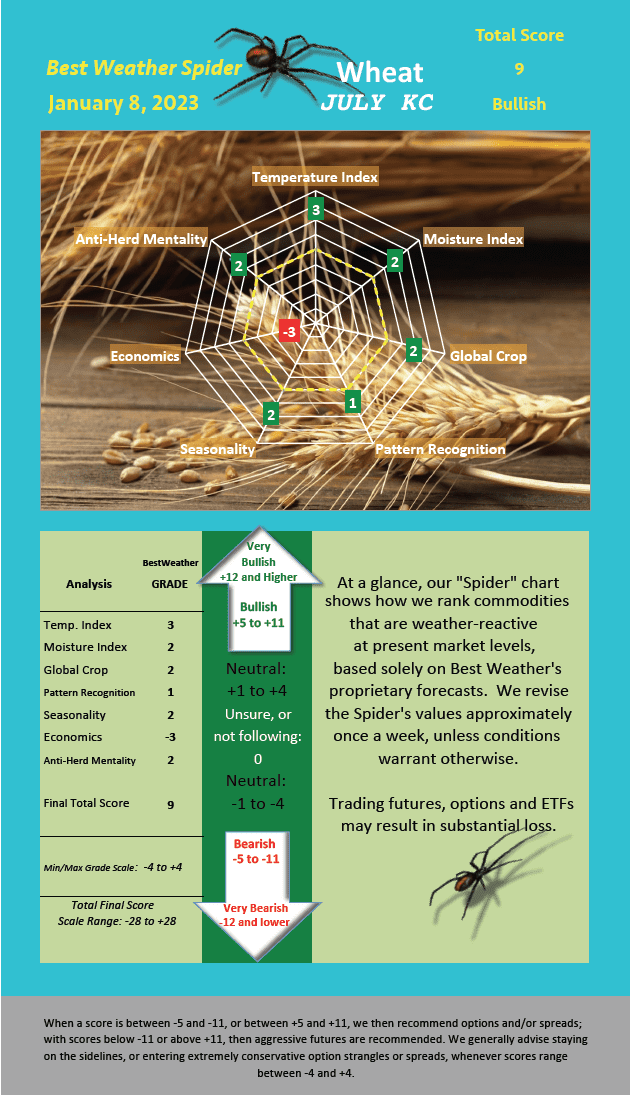

I will have my popular weather Spiders by Thursday a.m. I will likely raise natural gas from very bearish to neutral; my wheat Spider (KC wheat) was raised (see below) to slightly to modestly bullish; my coffee spider is bearish, and my corn and soybean spider is really unsure (neutral) due to possible rains later this month in Argentina and worries over the demand side of the equation and a big Brazilian soybean crop

FUTURES:

Long March corn from $6.54 on the Argentina drought from 2-3 weeks ago. The trade was up $1,000 a contract at one point and is now about even. Stop at $6.46 ($400 risk) ( confidence low-moderate)

Buy July KC wheat on the Plains drought and recent freeze and my weather spider in the video. Risk 20 cents ($1,000 a contract) (confidence moderate to high)

Long March soybeans and short November soybeans from last Tuesday (see last week’s reports) on the Argentina drought and seasonals, while November beans may lag due to an expected increase in 2023 Midwest acreage and the potential for wetter spring or summer Midwest weather. This trade is out $300 a contract before the opening Sunday night. Risk $1,000 on this trade. (confidence low to moderate). I frankly feel with a potential big soybean crop in Brazil and the chances for late January rains, there may actually be a shorting opportunity within a week or two. I am unsure about being in this spread for now.

OPTIONS:

Been short the March $1.80 coffee call for 1-2 months from 350-600 points and is now ahead $800-$1600 a contract. This is on top of at least two other option strangle or short call trades late last summer and early fall that potentially made you at least $2000-$3500 a contract, as well. (confidence high)

Been short the February $7,$8, and $10 calls for the last 2-3 weeks with nice profits again of anywhere from $1500-$3500 a contract. These short calls will expire worthless and be my 4 consecutive winning options trade in natural gas since late last summer. Stay tuned, I want to think about another trade in March options, but the market is quite oversold right now per my Spider in my video above. (confidence has been very high for 2-3 weeks, but I like taking profits on all short positions and waiting, for now)

ETFs/ETNs:

Took huge profits of 45-70% short the natural gas ETF (KOLD) last week. (confidence was very high the last few weeks)

Long the all grain ETF (TAGS) from two weeks ago and this trade is about even or down slightly. (confidence low to moderate)

Traders can buy the wheat ETF (WEAT) (confidence moderate to high)