In this report:

La Niña appears to be slowly forming

Differences between El Niño and La Niña

Some La Niña topics I will discuss over the next few months

Why corn & soybean prices rallied after a slightly bearish September USDA crop report

Long-term grain implications of La Niña & a negative PDO index

WeatherWealth Trade Ideas (click on the link)

My next report will be on Monday and discuss a historical look at global coffee weather and price action during La Niña events.

I began working on this report below, last week.

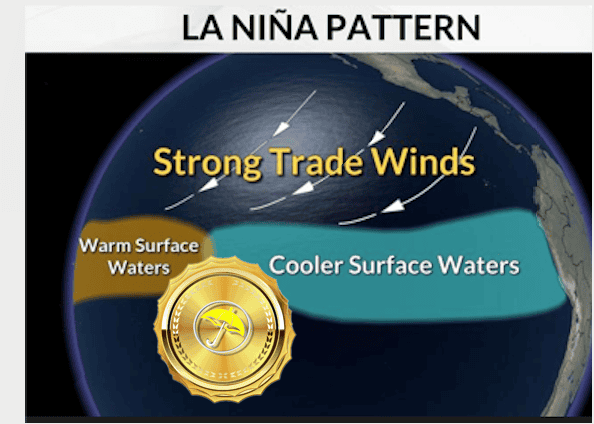

La Niña appears to be slowly forming

La Niña is forming and may be weak to moderate for the next few months. Some firms are saying the impacts will be muted as it will not last more than a couple of months. However, something we meteorologists call a negative Pacific Decadal Oscillation Index in the northern Pacific (-PDO) could potentially extend La Niña into 2026.

However, La Niña may have to remain into May-July, 2026, to warrant a major bull market in grains. This is something I am uncertain about at this time. Nevertheless, some potential crop issues could exist from December to February in Argentina and southern Brazil that “might” result in a mini-bull market in grains, later.

A weak La Niña means only modest cooling of Pacific waters, which usually results in mild shifts to global weather patterns and less consistent or less intense impacts.

In contrast, a strong La Niña leads to much colder Pacific water and noticeably stronger changes to atmospheric patterns—causing more pronounced droughts, floods, and temperature extremes in affected regions.

Differences between El Niño and La Niña

El Niño and La Niña are opposite phases of the ENSO climate cycle that significantly influence global weather patterns and commodity markets, but they do so in different ways:

El Niño

- Characterized by warming of the Pacific Equatorial Ocean surface waters.

- Tends to cause warmer and drier conditions in major agricultural areas like Australia and Southeast Asia, often leading to drought and reduced wheat crop yields there.

- Brings heavier rainfall to southeastern South America, western North America, and eastern Africa, which can boost production in those regions vs droughts in São Paulo/Minas Gerais that can hurt sugar cane and coffee production.

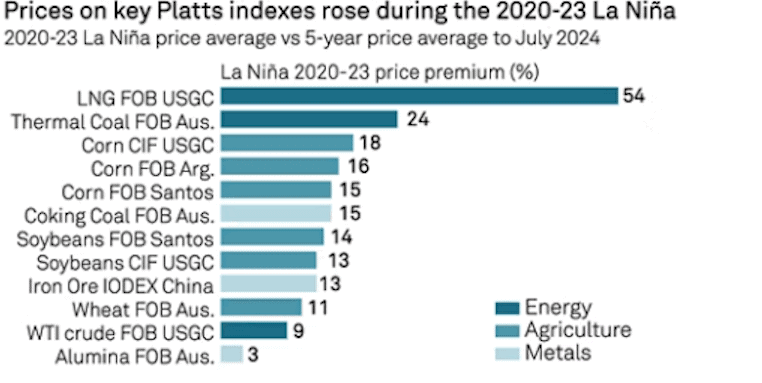

- Overall, El Niño often reduces global agricultural commodity production in some areas, causing supply shortages and price increases, especially for sugar, cocoa, and coffee.

- It accounts for about 20% of global commodity price inflation movements and can raise food commodity prices by 3-9% during strong events due to supply shocks.

- El Niño can also cause extreme weather events like floods, hurricanes, and droughts that disrupt production.

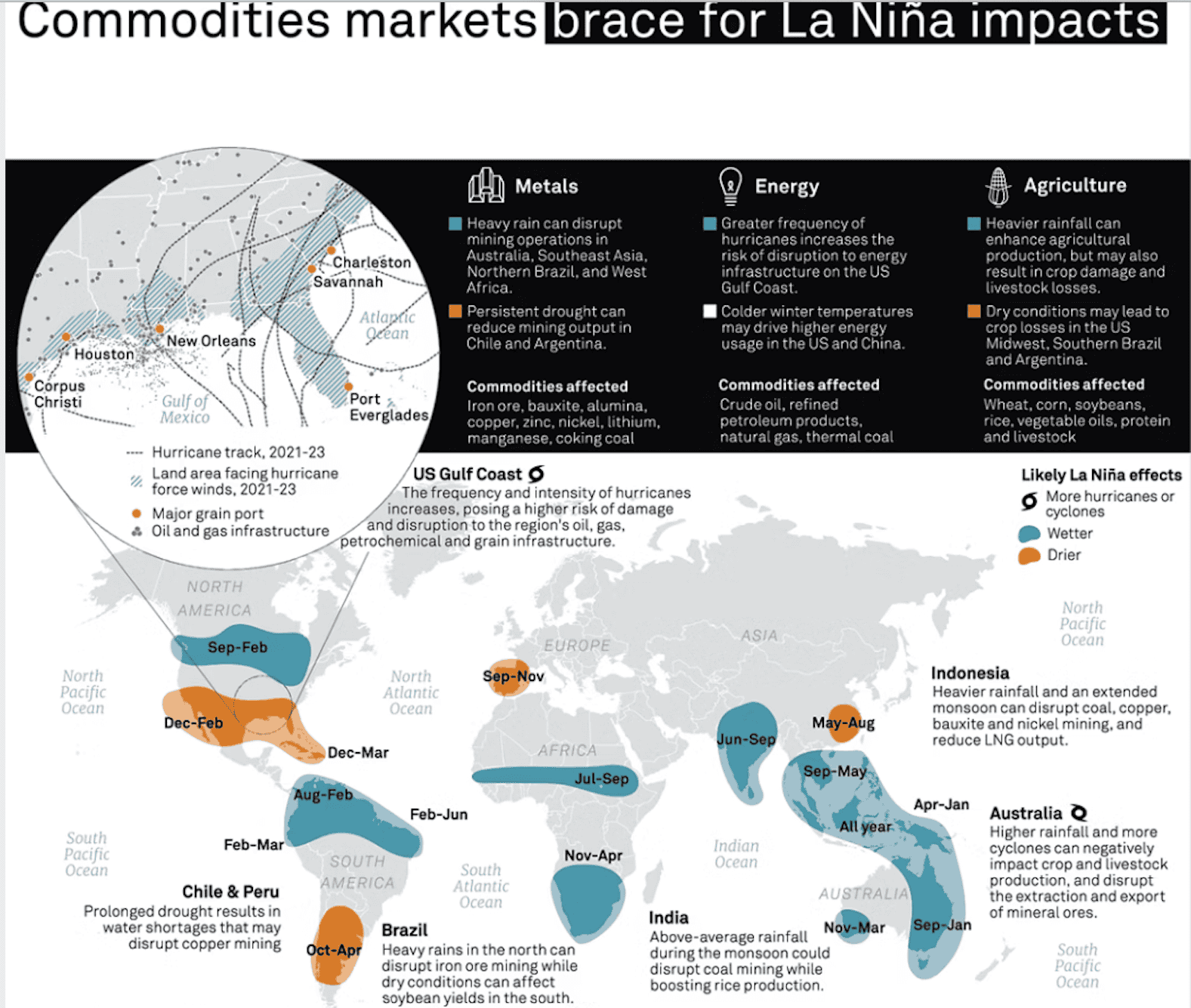

La Niña

- Characterized by the cooling of the Pacific Equatorial Ocean surface waters.

- Typically leads to wetter conditions and flooding in Australia, Indonesia, and parts of Southeast Asia, benefiting crops there.

- Causes drought and heat stress in parts of the U.S., Canada, and/or Russian wheat, corn, or soybean regions during the spring and summer.

- La Niña events often result in lower crop production for key Argentina and southern Brazil commodities like corn, soybeans, wheat, and sugar cane, due to drought impacts in critical growing regions.

- Can have mixed results for global coffee production, with generally improved yields for Vietnam and Indonesia Robusta. Brazil coffee yields can vary and are more favorable during weak vs strong La Niña events.

Some La Niña topics I will discuss over the next few months

1) Whether Argentina and southern Brazil may have dry weather this winter (their summer) and resulting in a bull market in grains?

2) Could La Niña extend into the spring, summer, and the 2026 growing season, and help corn, wheat, and/or soybean prices bottom?

3) The possibility of a colder-than-normal start to the US winter in key natural gas and/or heating oil demand areas. However, warmer-than-normal US weather in October usually reduces energy demand and is often bearish for natural gas, first.

4) Why could weak, not strong, La Niña events set the stage for improved Brazilian coffee weather? The caveat remains Climate Change and deforestation of the Amazon; otherwise, typically, we would have a bear market in coffee later.

5) Generally improved weather for West African cocoa and below normal chances for a strong Harmattan Wind. This tends to be bearish for cocoa prices in 65% of these cases by winter and spring. The caveat? Here too, Climate Change and the old age of trees in West Africa are also significant.

6) Weak La Niña events tend to increase global sugar production, while stronger ones can affect production more adversely with droughts in Brazil sugar cane areas and flooding in other parts of the world.

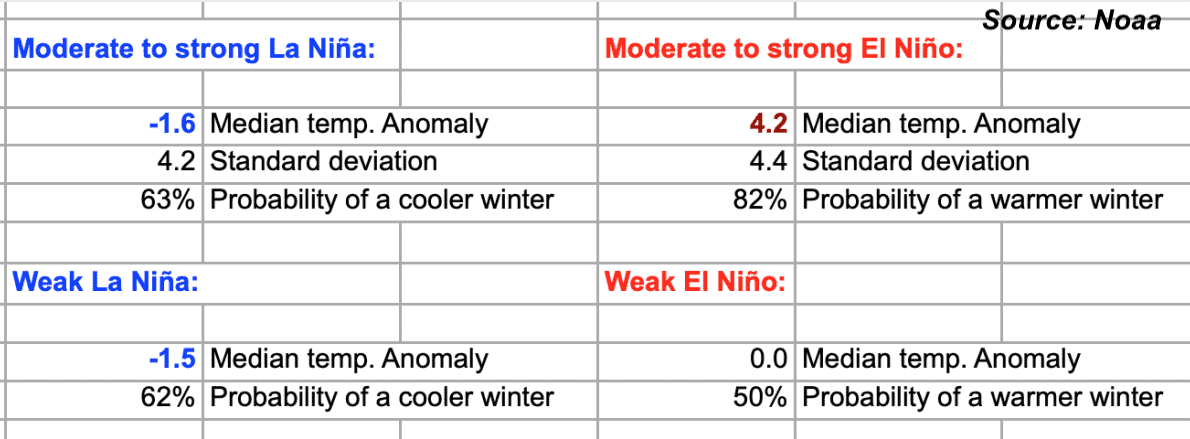

Source: S&P Commodity Insights, NOAA & UK Met office

The impacts of La Niña on global commodities (tables above) can be more muted during weaker events. In addition, the onset of Climate Change, African dust (weakening the hurricane season), and a host of other teleconnections, such as the strongly negative PDO index, can also have a major influence on global weather and commodities. So… take the tables with a “grain of salt”

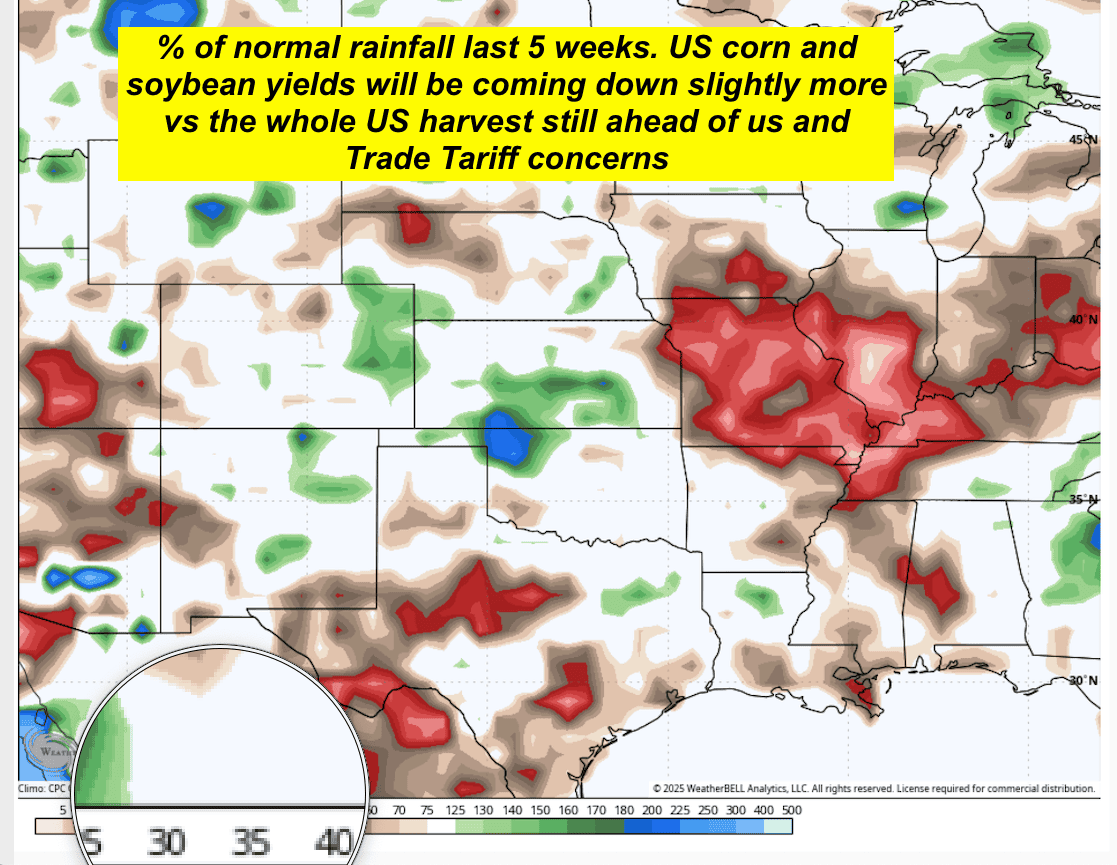

Why corn & soybean prices rallied after a slightly bearish September USDA crop report

Even though I said (two to three weeks ago) the very dry end to the US summer should mean “lower US corn and soybean yields”… why did I not make any strong buy recommendations in corn and soybeans?

The answer is: “Because the entire US corn and soybean harvest is still ahead of us.”

Due to the recent dry weather, my Weather Spider went from slightly to modestly bearish most of the summer to unsure last week for corn and soybeans (see the WeatherWealth Trade Ideas section here).

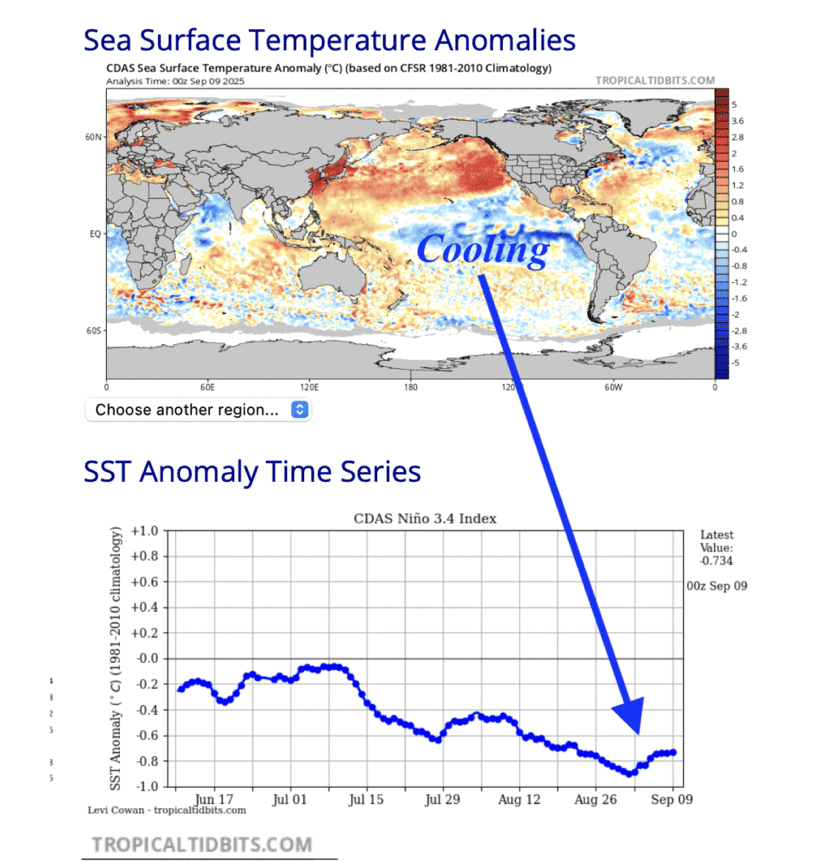

This is also a sign that La Niña is slowly forming.

Corn and soybean prices rallied modestly last Friday, following a neutral to bearish USDA report because of this fact:

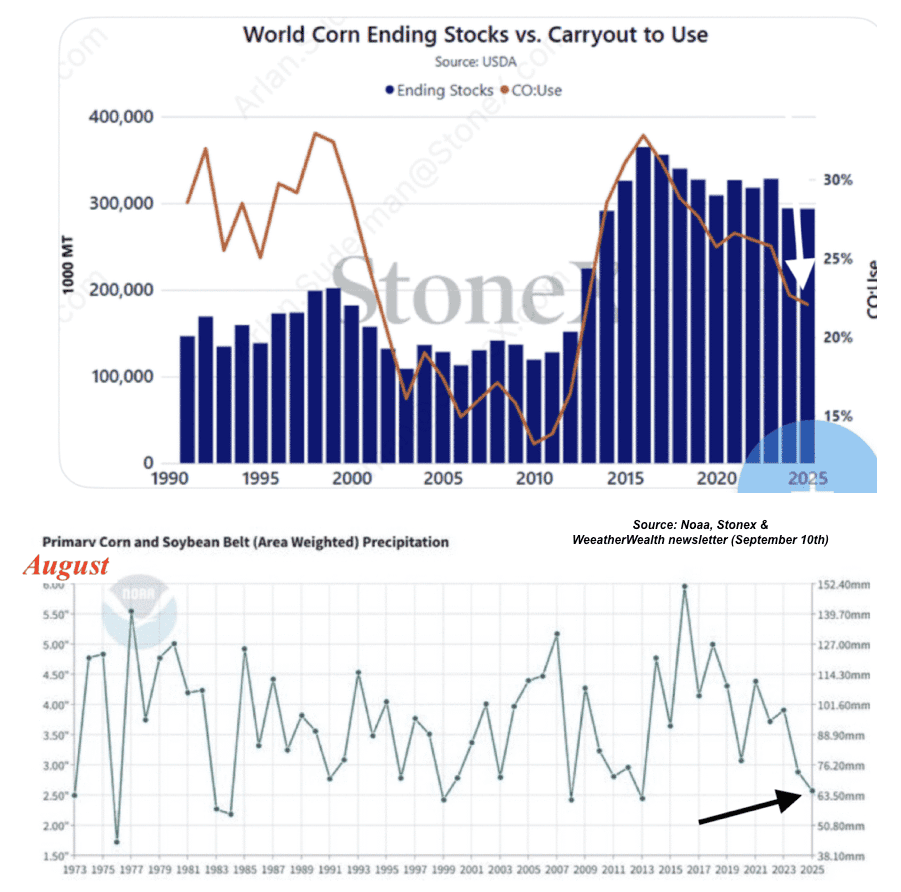

Lower US yields will likely occur in future USDA reports. Nevertheless, there are still huge corn and soybean prices out there.

Long-term grain implications of La Nina & a negative PDO index

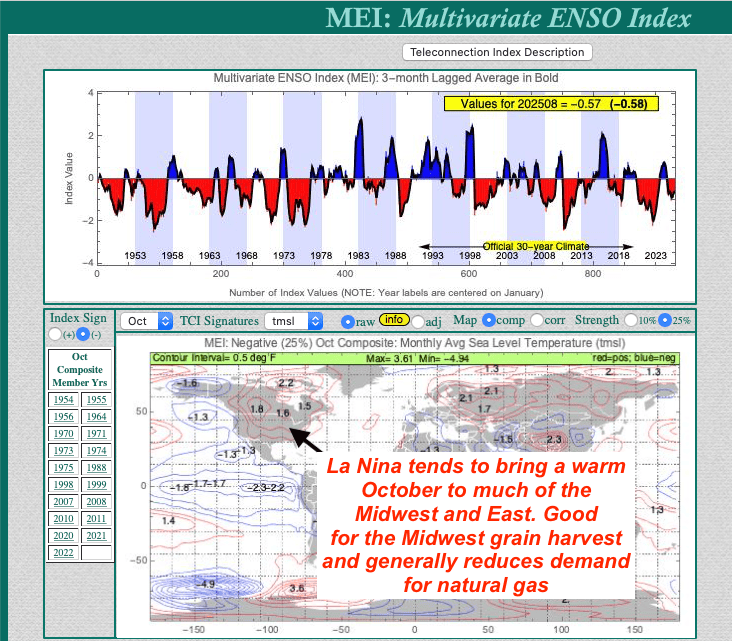

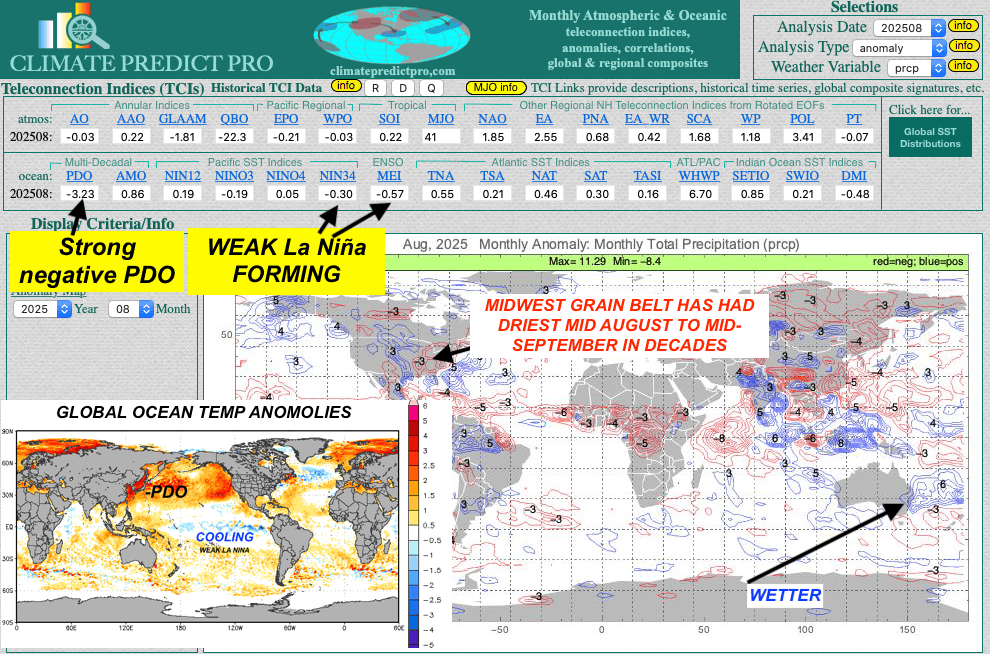

1) Generally warm, dry weather for the Midwest grain harvest

A weak La Niña forming in September, combined with a strong negative Pacific Decadal Oscillation (PDO) index, tends to produce warmer, drier conditions in the U.S. Midwest during the critical October grain harvest period.

Again, this is why I did not make any strong recommendation to buy corn and soybeans. However, longer term, after being generally bearish most grains the last two to three years, this “might set the stage” for a bull market later. I am just not sure of the timing.

It is already happening in the corn market, but I do not want to recommend buying a 30-cent rally ahead of harvest.

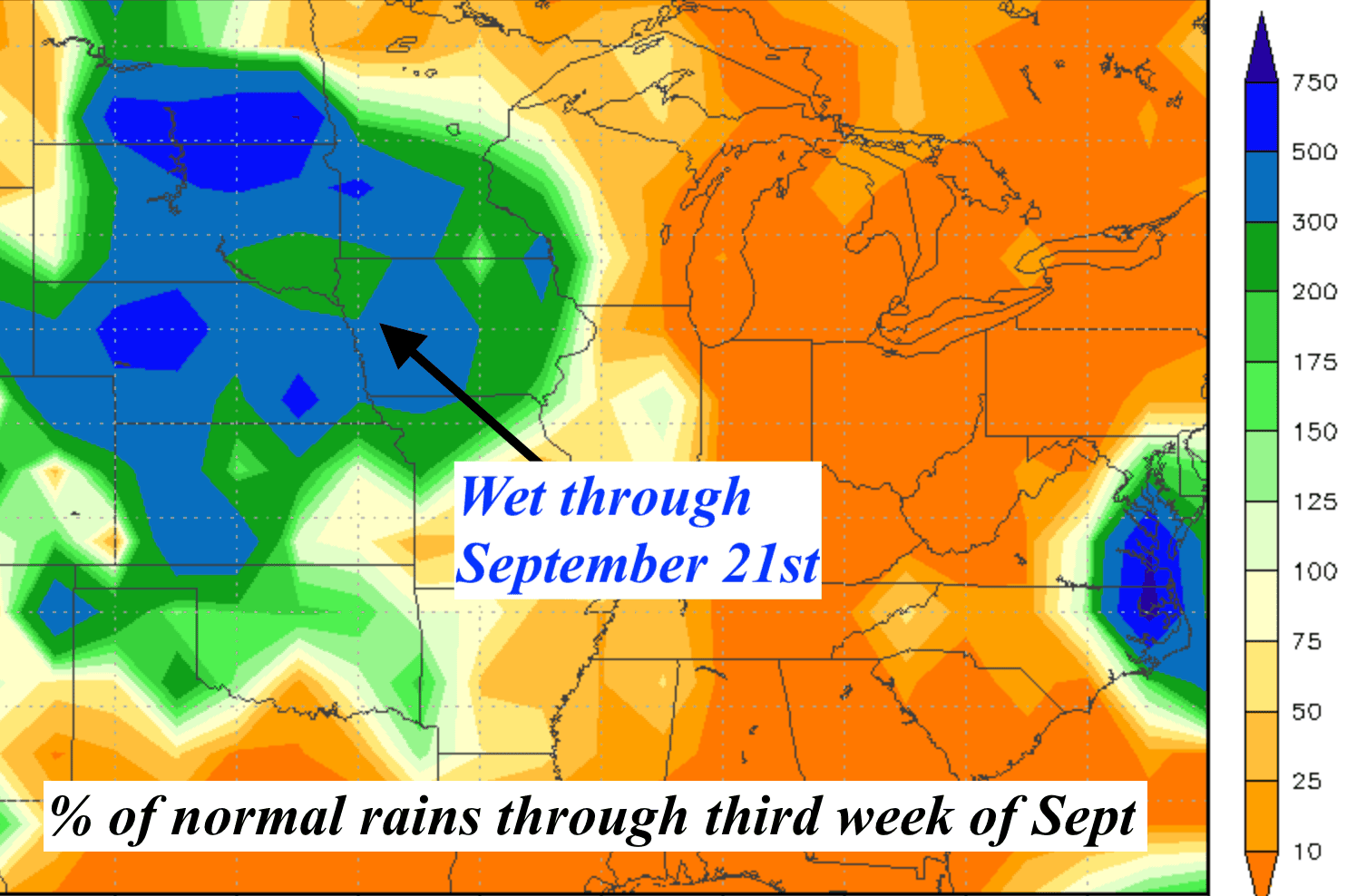

Notice the intense warming in the northern Pacific that has been the case for years (negative PDO). Also, cooling along the equatorial Pacific (weak La Niña forming).

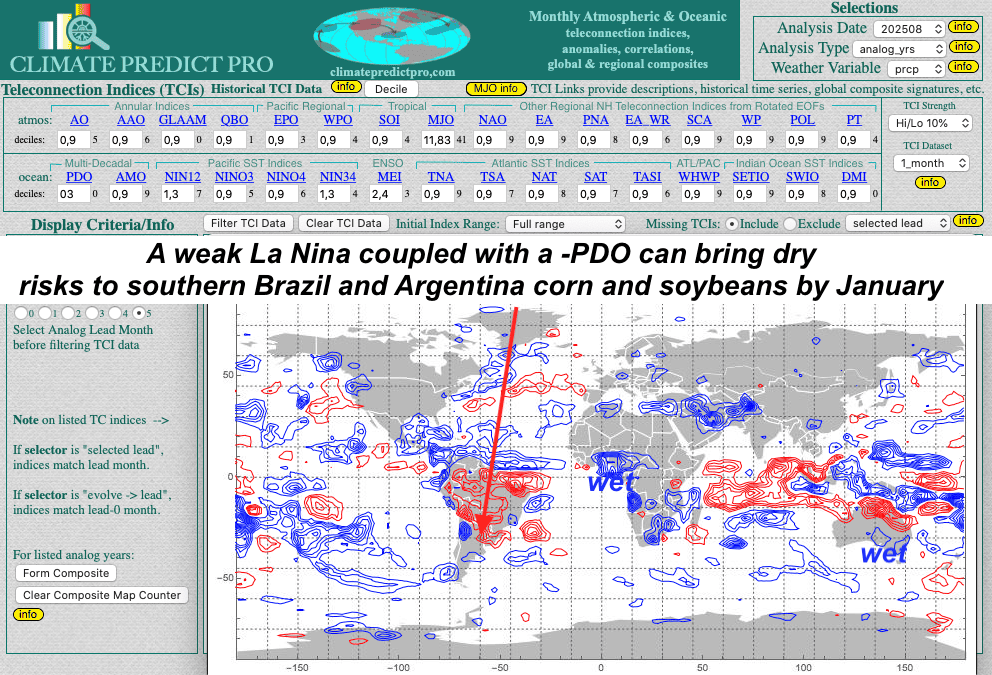

Some rains are expected in the western and northern corn belt in the next few days, but there should not be any long-lasting pattern or detriment to the harvest.

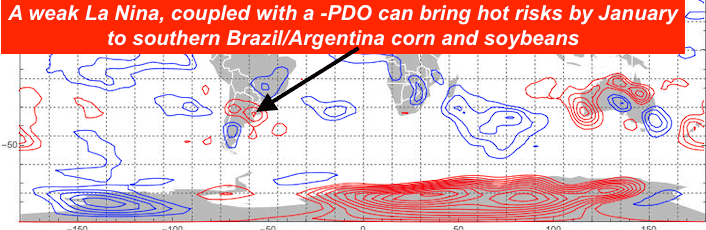

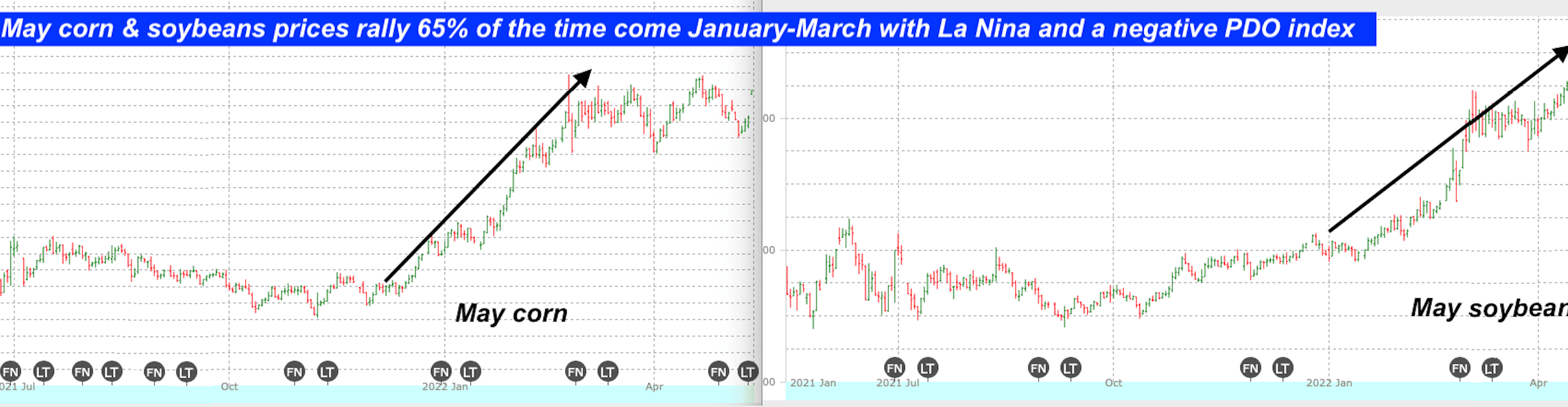

2) Potential drought risks to Argentina and/or southern Brazil corn and soybeans between December and February

Notice how corn and soybean prices tend to rally by late December or January 65% of the time, with a similar teleconnection setup. Over the next month or two, prices may chop around.

3) Potential or summer drought risks for Midwest corn and soybeans, and/or spring Plains and Russian wheat regions

The negative PDO/ La Niña combination also correlates with drought tendency in the central U.S., especially in the Corn Belt, Canada, and the Plains, and often leads to a drier and warmer spring or summer. This could stress crops next year and end the bear market in wheat and/or corn and soybeans.

However, it is presently “too early” to predict if La Niña will extend deep into 2026 and just how strong it will be (stay tuned).

Anyone talking about solar or other cycles is completely out to lunch, as far as that being a climatic influence on grain production.

BOTTOM LINE: Yes, corn and soybean prices have bottomed. Corn and soybean prices may remain a bit volatile through October, given the mixed bag of fundamentals: Generally decent harvest weather vs slightly lower crop prospects; strong demand for corn, but not so much for soybeans. However, the chances do exist for a post-harvest rally. If weather problems begin in southern Brazil and Argentina come December or January, a modest rally could occur. This depends on just how strong La Niña gets over the next few months.

With respect to wheat production and prices, I have generally been bearish on this market since April. Nevertheless, until we see how 2026 crops may fare and the charts look more positive, I currently have no interest in making any strong trade recommendation.

WEATHER WEALTH TRADE IDEAS

Please click on the image below

To see a new trade recommendation I made in coffee early Tuesday a.m., (following the massive price rally) and all about the natural gas, grain, sugar, and the cocoa market, click below