November 17th

In This Report:

Introduction: Corn price action during La Niña events, coffee tariffs still in place & early winter outlook

December-February South American rainfall and temperature trends during La Niña events

South American Corn yields during La Niña events

A look at current South American crop conditions

Trump Administration throws another curve ball. This one is regarding tariffs for Brazilian coffee.

An historic stratospheric warming event: Implications for early winter weather?

Weather Wealth Trade Ideas (bottom of my report)

Top Trades?

Long the natural gas ETF (BOIL), as I expect one of the coldest US winters for energy areas since 2010

Short March or July, 2026 coffee call options out fo the money, longer term

Long the silver ETF (SLV) longer term

Inquire about discounted annual subscriptions to the most popular global commodity weather information with trading ideas for farmers, hedgers and traders. Click here

After your free trial, if you are a farmer or small trader, we offer discounted subscriptions up to 70%. Ask me any question here about the weather, farming, a trading idea you want or about my newsletter (Email. bestweatherroemer@gmail.com)

Introduction:

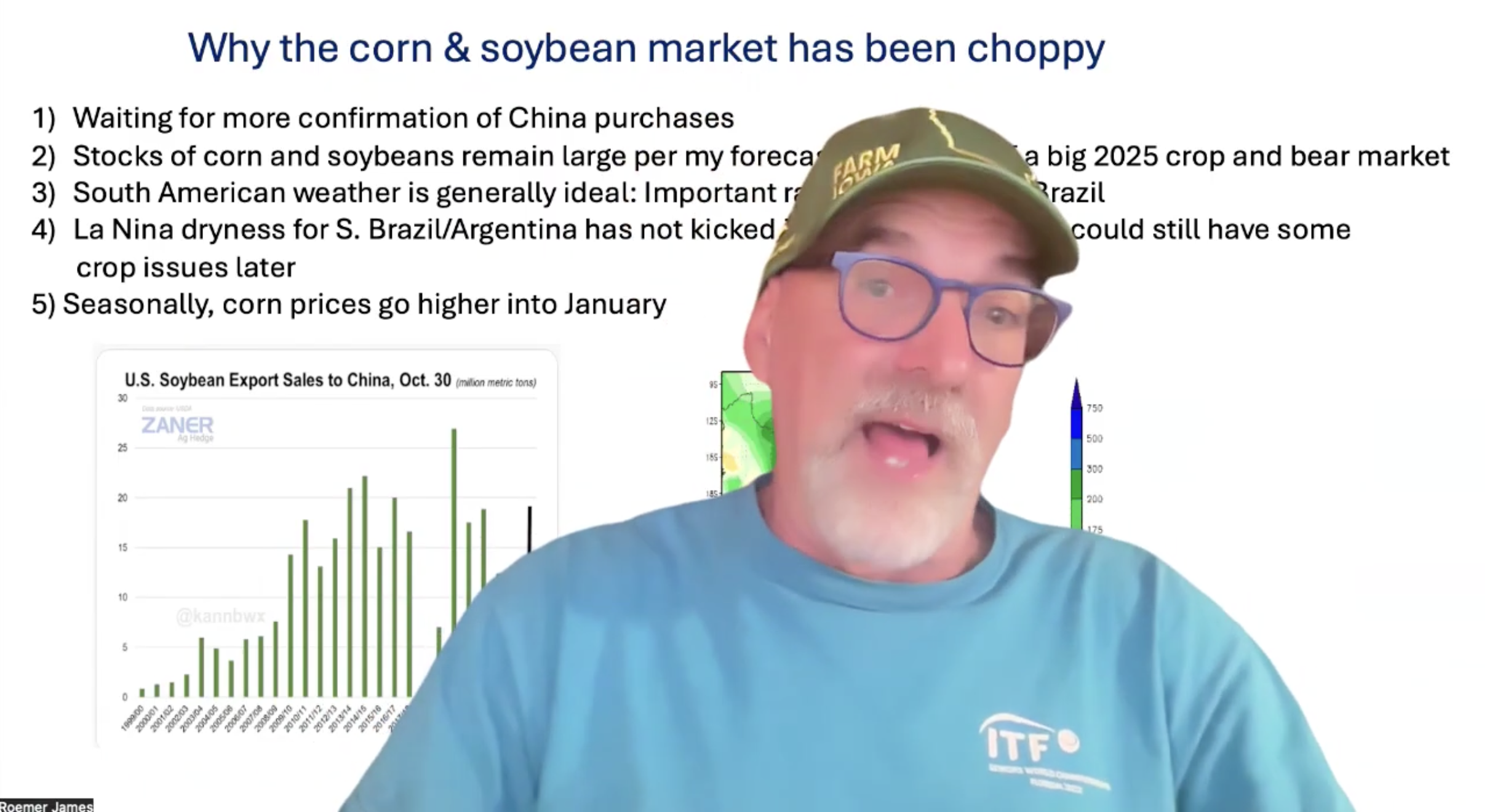

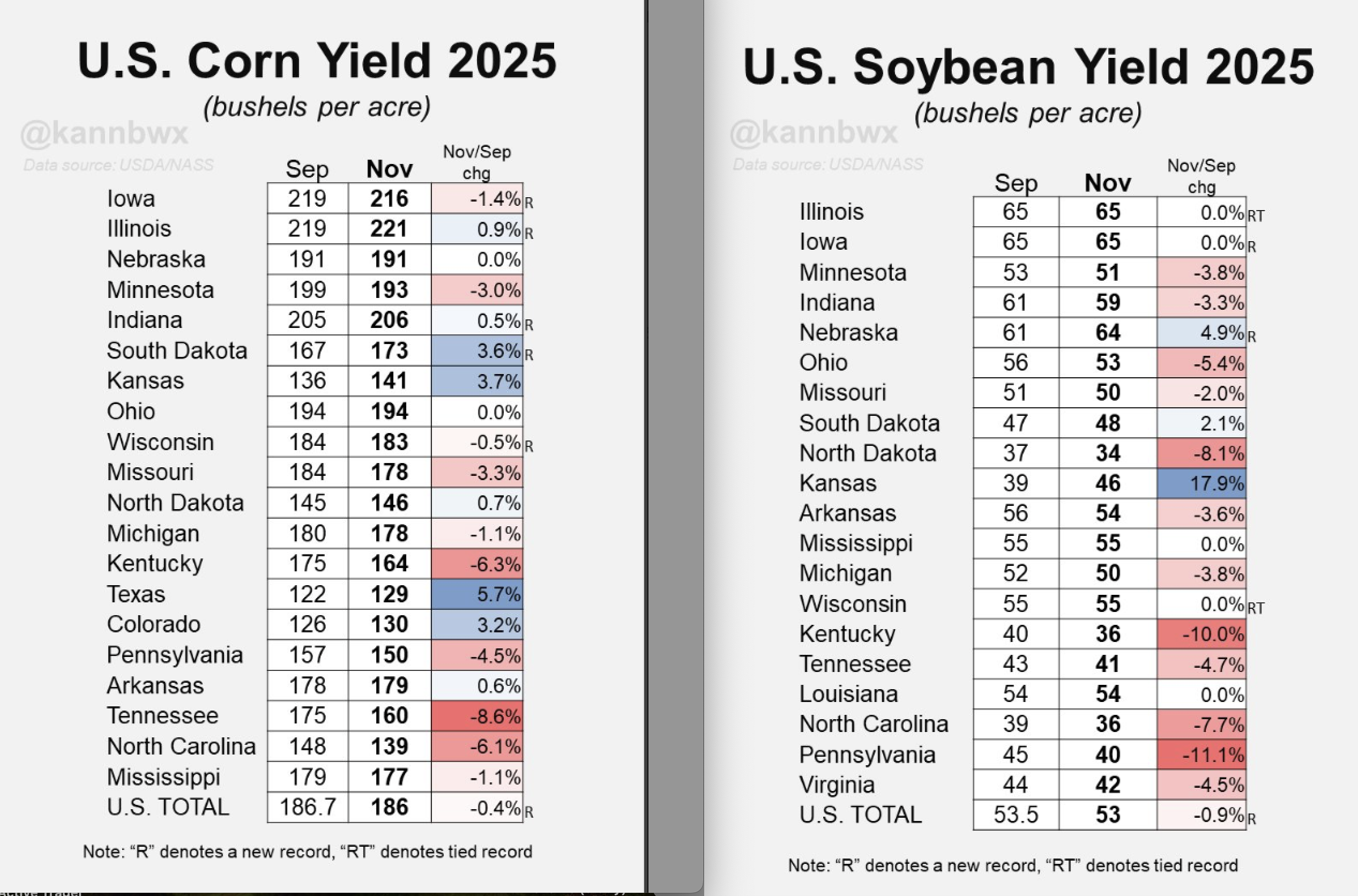

The USDA throw a bearish shocker on Friday basically keeping US corn and soybean yields the same (Even in the midst of a dry late Midwest summer and some disease issues to corn). Could this be a buying opportunity in corn and soybeans due to the “demand” side of the equation improving and La Niña that could lower South American production two to three months from now? It is possible.

While not “written in stone” by any means, Trade Tariffs and a host of other fundamentals are affecting grain prices.

This report covers La Niña and what usually happens to South American corn production and price action. I also discuss the ridiculous and volatile coffee market regarding “on again, off again” Trade Tariff jargon and briefly address why the US winter could be colder than normal and eventually affect natural gas prices. Currently, the natural gas market got way ahead of itself, given the warm outlook in returning to the US for the next week or so.

Corn and soybean prices collapsed on Friday due to the USDA, and not lower yields. However, due to a lack of data during the government shut-down, it is possible that downward adjustments for yields could occur in future reports.

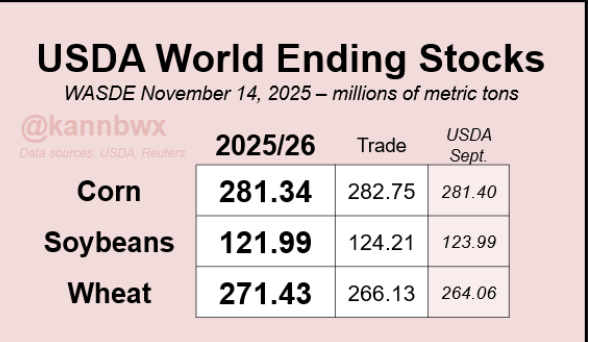

World ending stocks for corn, soybeans and wheat were raised

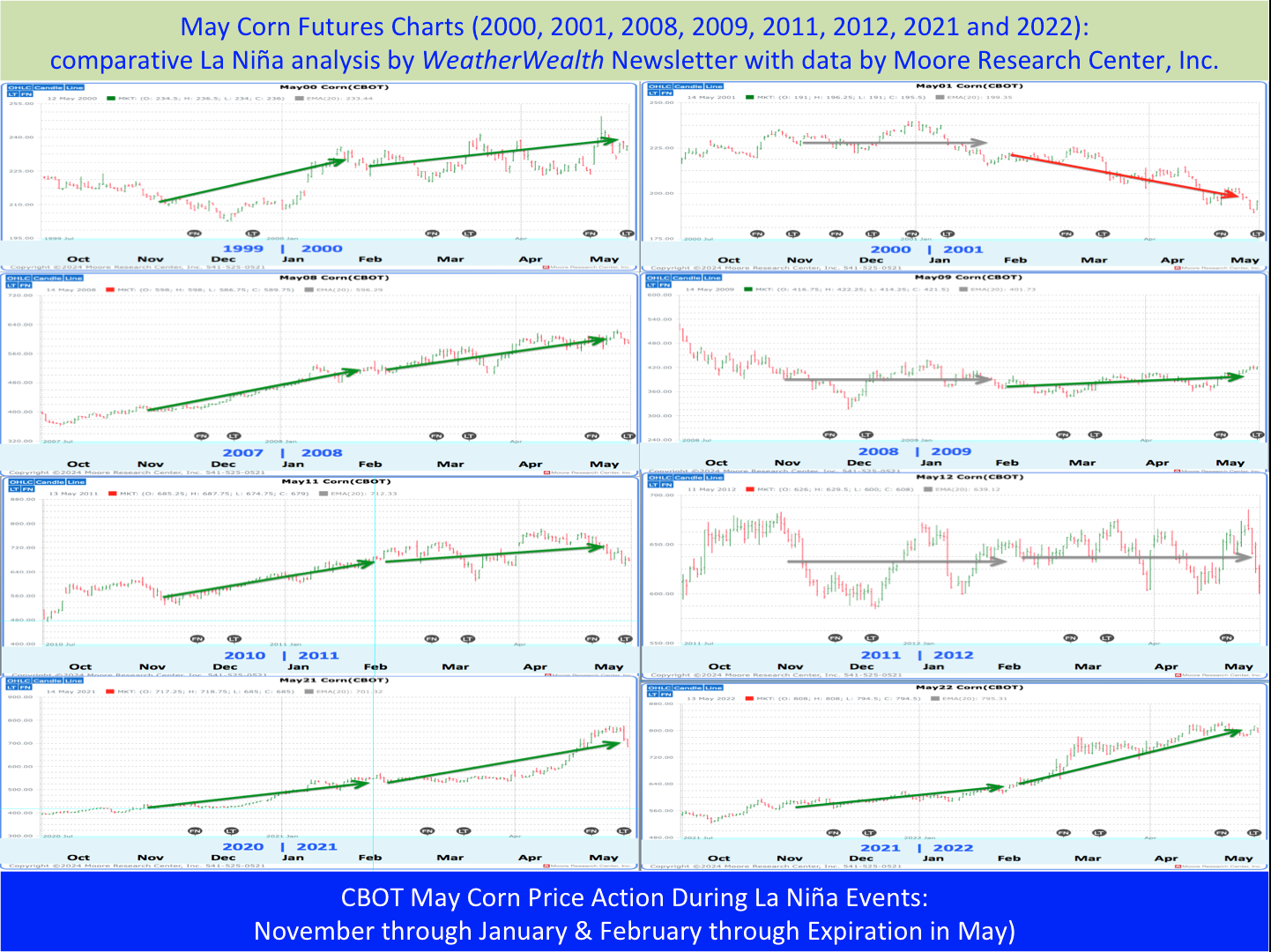

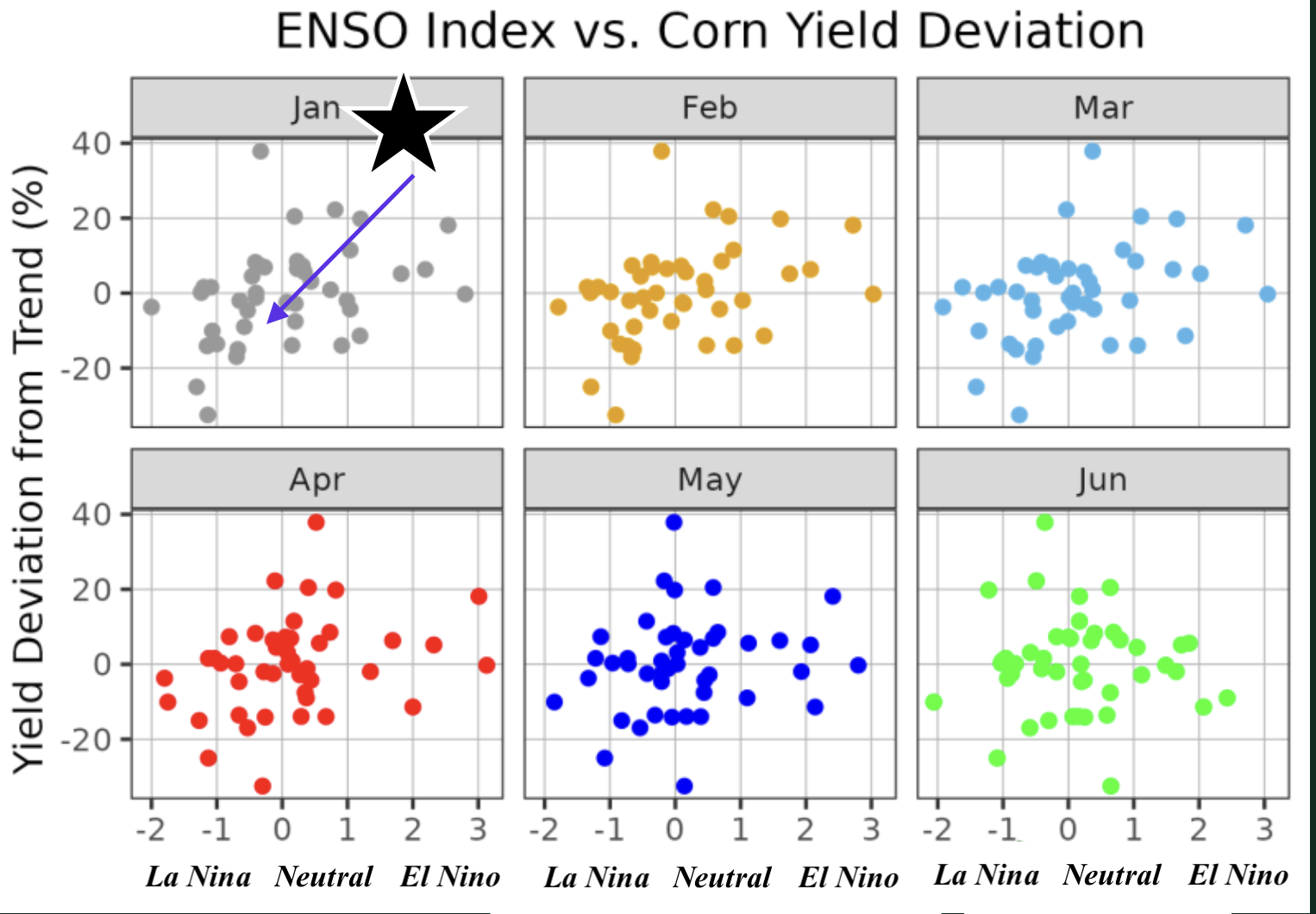

Corn prices have tended to be steady to higher (December-March) during six of the last seven La Niña events with the exception being May 2001 corn (top right chart) during the North American winter (South American summer) of 2000-2001.

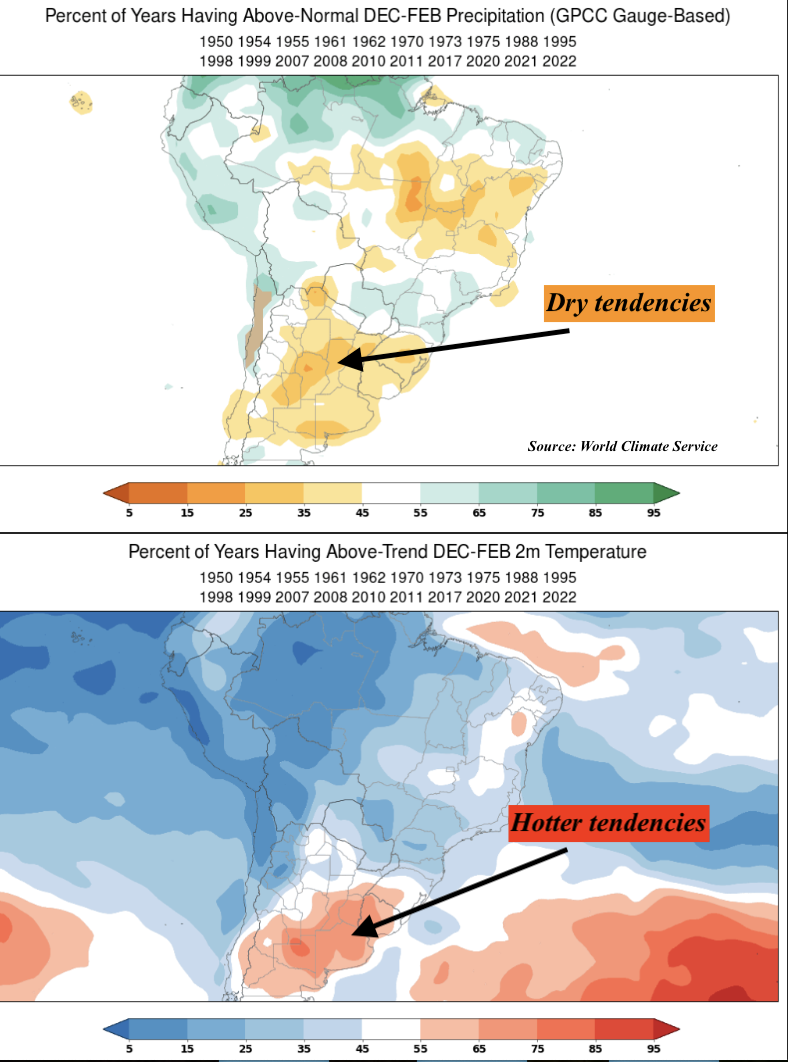

December-February South American rainfall and temperature trends during La Niña events

In the weeks and month ahead, I will be monitoring both South American weather and, of course, the northern Hemisphere spring and summer weather for grains and other commodities.

One key will be whether La Niña sticks around and strengthens in 2026. Many models have it weakening which would not be as bullish later (stay tuned).

Most (not all) La Niña events show some dryness and heat for corn and soybeans in southern Brazil and Argentina between December and February. However, there are other teleconnections from my ClimatePredict program I need to investigate.

Sources: Crop Prophet and World Climate Service

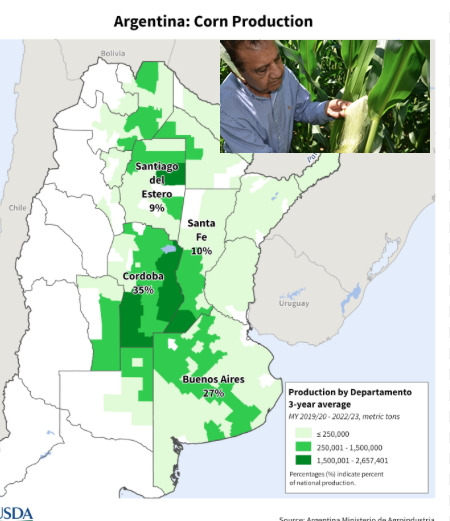

South American Corn yields during La Niña events

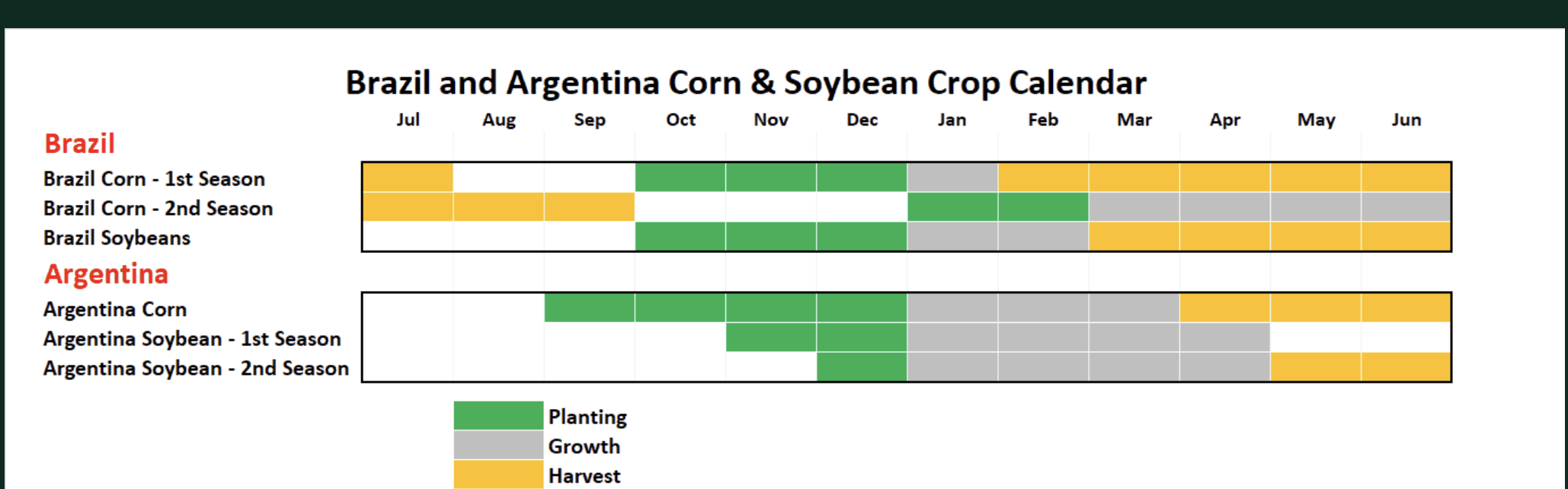

January and February are the most crucial period for corn pollination and filling stages in Argentina and southern Brazil. (This is similar to July for the US corn belt when weather is nearly a 100% influence in the market).

See the “growth stage” for corn and soybeans on the chart below

Historically, one can see that during the critical January pollination stage for South America corn, yields tend to fall by at least 5-10%, more than half of the time.

However, this is not written in stone and “usually it is the strong La Niña events that affect corn and soybean production the most in South America. Currently, we have a weak La Niña. Nevertheless, some reduction in corn and soybean yields could still occur two to three months from now.

SOURCE; CROP PROPHET : WORLD CLIMATE SERVICE

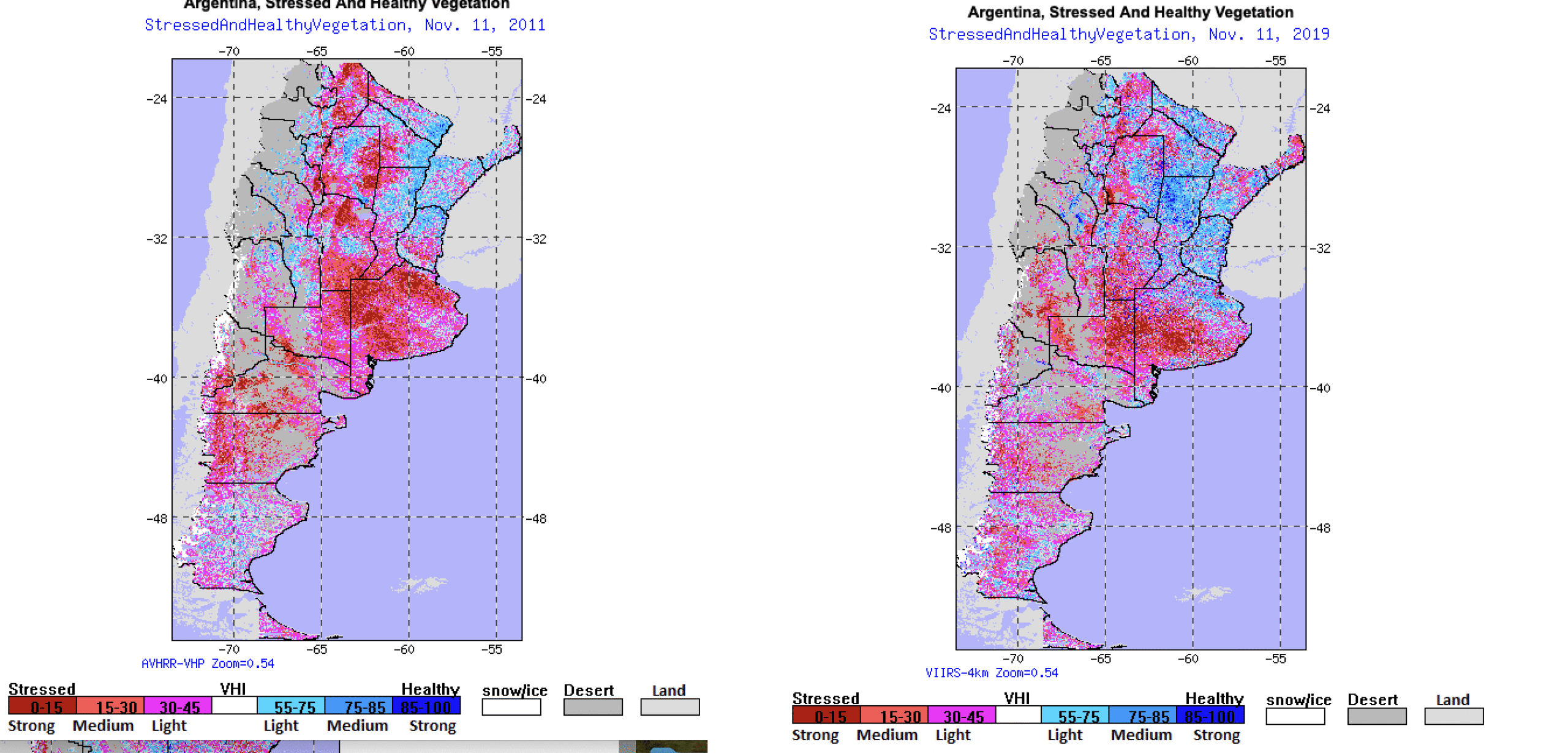

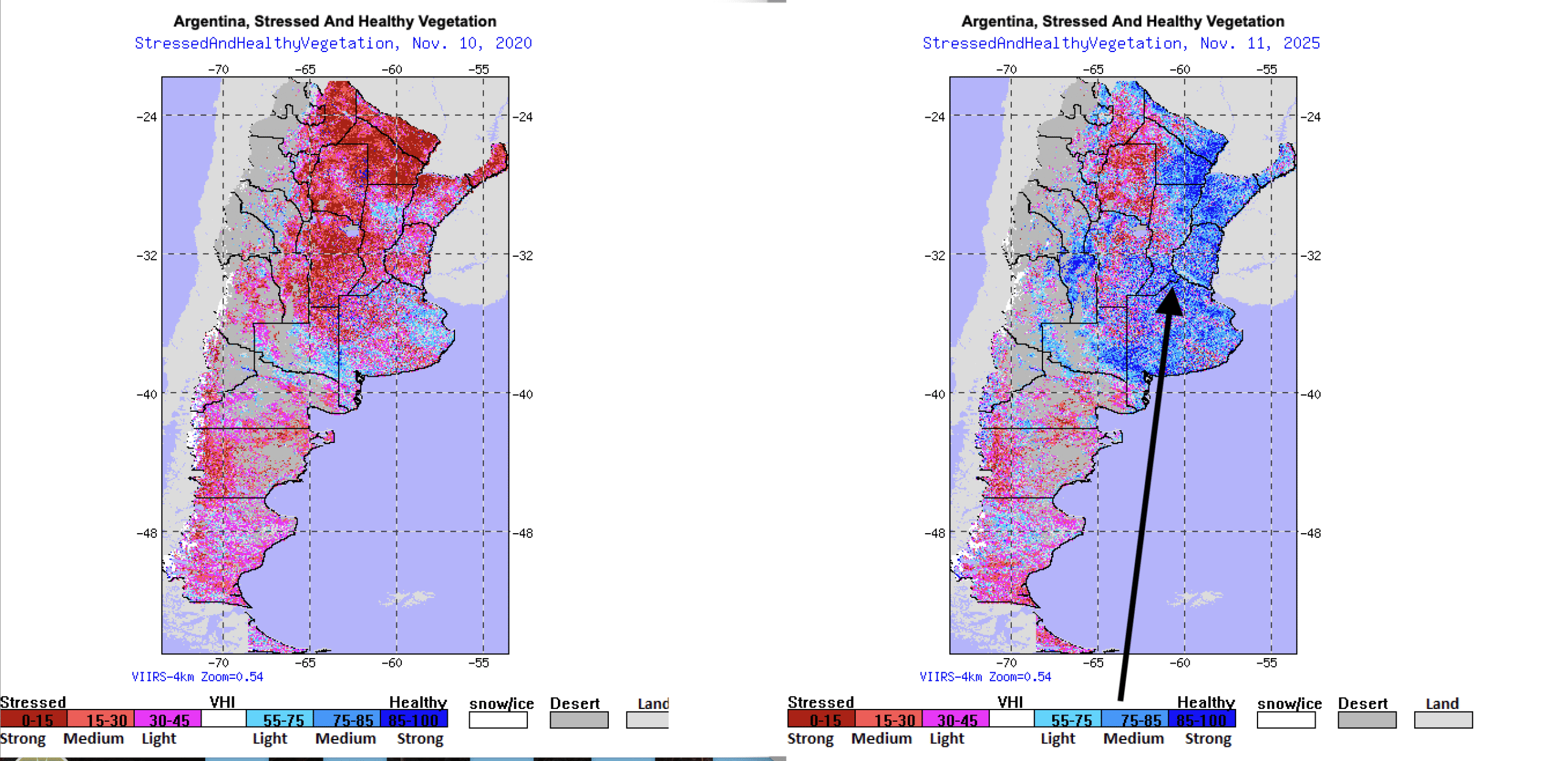

A look at current South American crop conditions

Some of the strongest winter (South American summer) bull markets in corn and/or soybeans during La Niña events began when crop stress was high as early as mid-November (maps below).

Needless to say, remember that planting is going on currently and it will not be until later December-February that we will be more in a South American weather market for corn and soybeans.

Some notable cases were 2011, 2019 and 2020. However, notice today (vegetation index lower right–November, 2025) how current soil moisture conditions are quite favorable (blue). Otherwise, I would have a strong buy recommendation following traders being washed out Friday by a bearish USDA crop report.

SOURCE: NOAA VEGGIE STAR

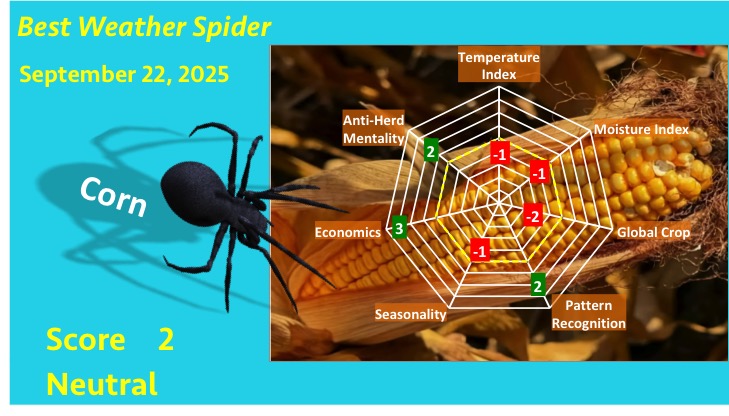

Bottom Line For Corn Prices and production:

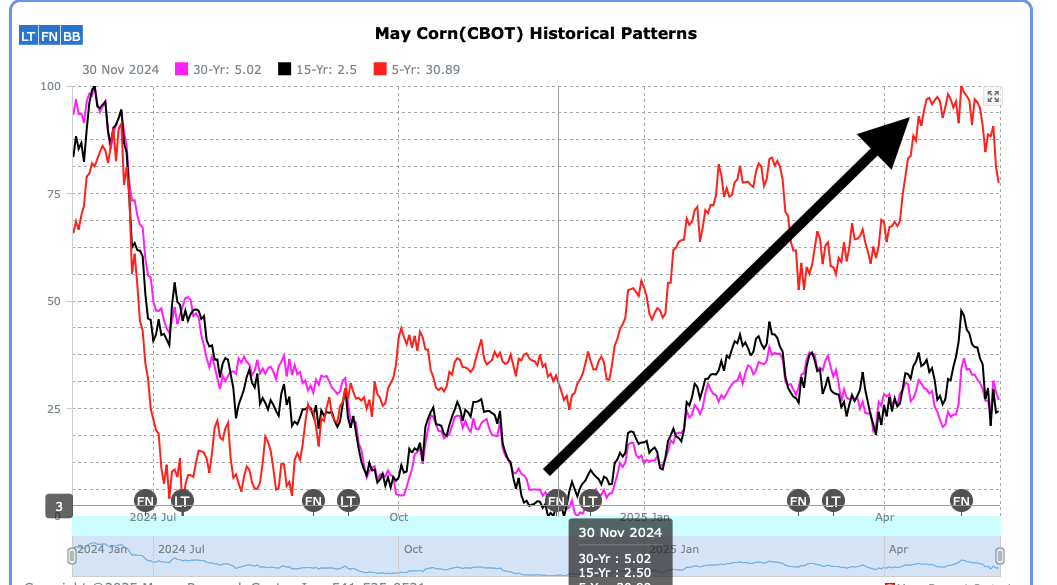

For nearly two months. the BestWeather Spider for corn has been mostly in the neutral to slightly bullish range. It is surprising that given disease issues to corn in parts of the Midwest and a dry late summer, the USDA did not lower US corn yields to at least 183 bushels/acre of lower. Almost every analyst missed the boat. However, I do not like guessing at crop reports and have abstained from making any high confidence trade recommendations since my summer 2025 bearish attitude. It is possible that this strong bullish seasonal below combined with the “potential” for the excellent early season weather conditions in South America to begin to deteriorate due to La Niña could put a floor in this market at some point and result in a conservative long position.

This Spider is quite old and needs to be adjusted as we get into the South American growing season and weather market come December-February.

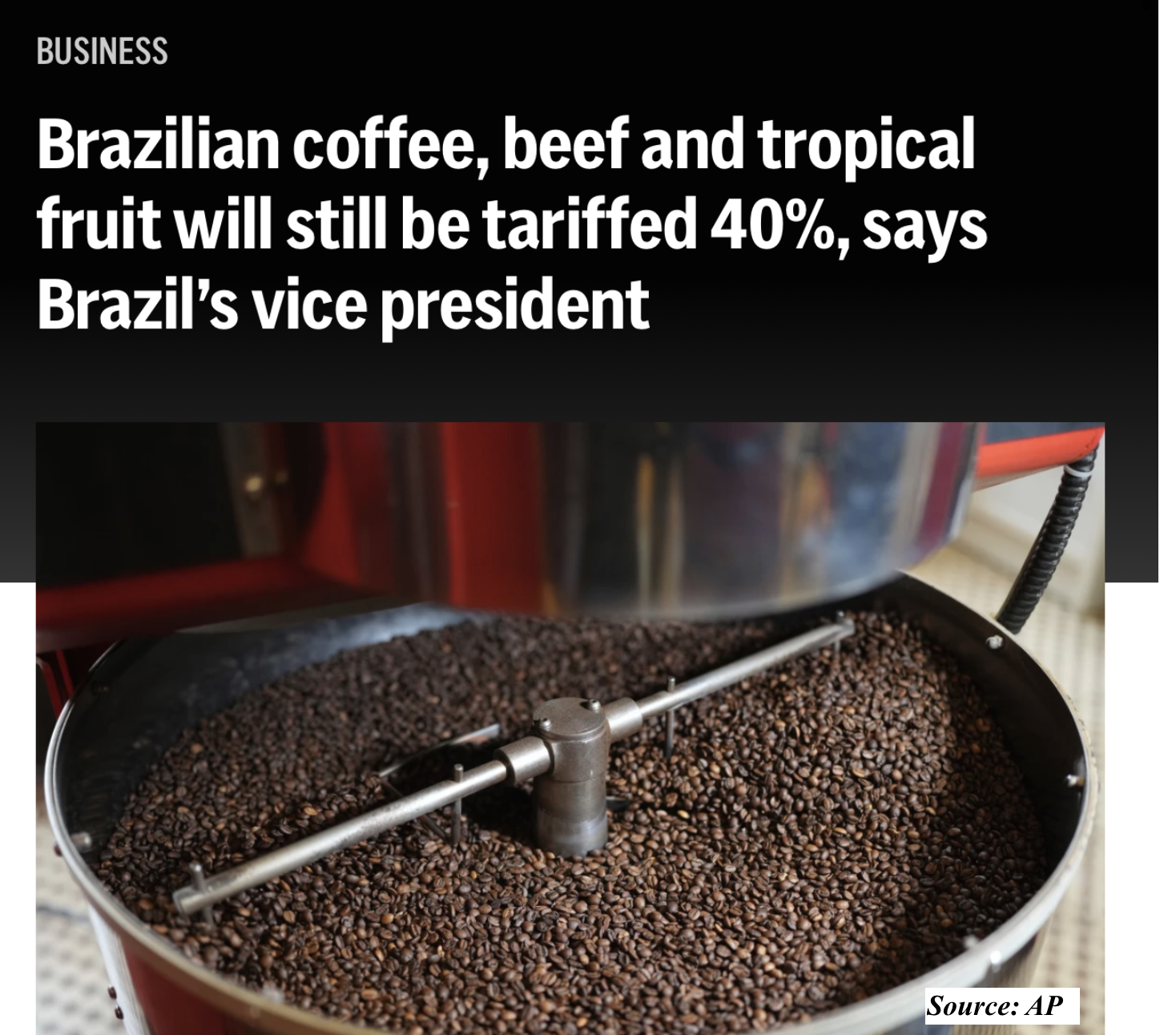

Trump Administration throws another curve ball. This one is regarding tariffs for Brazilian coffee

SOURCEL AP

Following my special update on Friday that coffee prices broke support due to potential Trade Tariffs on Brazil coffee being reduced 100%, this was indeed not the case.

The 40% tariff on Brazilian coffee remains intact, despite some recent tariff reductions by the US. Brazil’s Vice President stated that while the US has removed some import taxes on Brazilian goods, the additional 40% levy on products like coffee, beef, and tropical fruits is still in place.

Anyway, this makes it “impossible” to trade coffee futures on a day to day basis based on global weather. This is why (for three or four months) I suggested selling out of the money March 2026 call options was the “only way to play this game!”

- What the reduction means: President Trump lifted some initial, 10% reciprocal tariffs on certain goods, reducing the combined tariff on some Brazilian products by 10%.

- What the 40% tariff means: The larger, 40% surcharge that was imposed in July remains in effect on coffee, beef, and tropical fruits.

- Impact on Brazil: This leaves Brazil with a significantly higher tariff (effectively 40%) compared to other countries whose coffee exports are now exempted. Brazil’s vice president called the 40% tariff “very high” and said the government will continue to work on getting it reduced further.

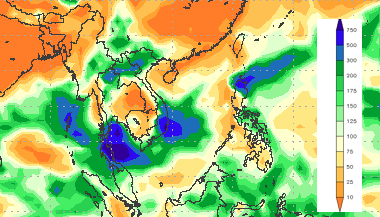

Finally, another reason that Robusta coffee is leading the pack with higher prices on Monday is due to more incessant rains in Vietnam delaying the harvest. This is why, several weeks ago, I said that Robusta coffee “might be a buy” but my Spider has been pretty much neutral to only slightly bullish (too many factors to digest).

% of normal rainfall this week (more coffee harvest delays for coffee in Vietnam)

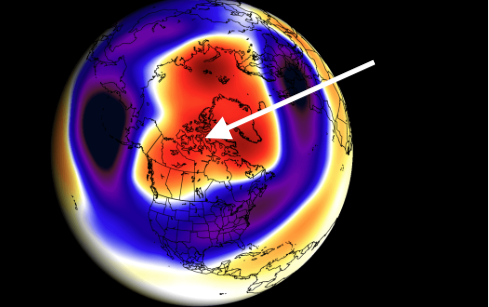

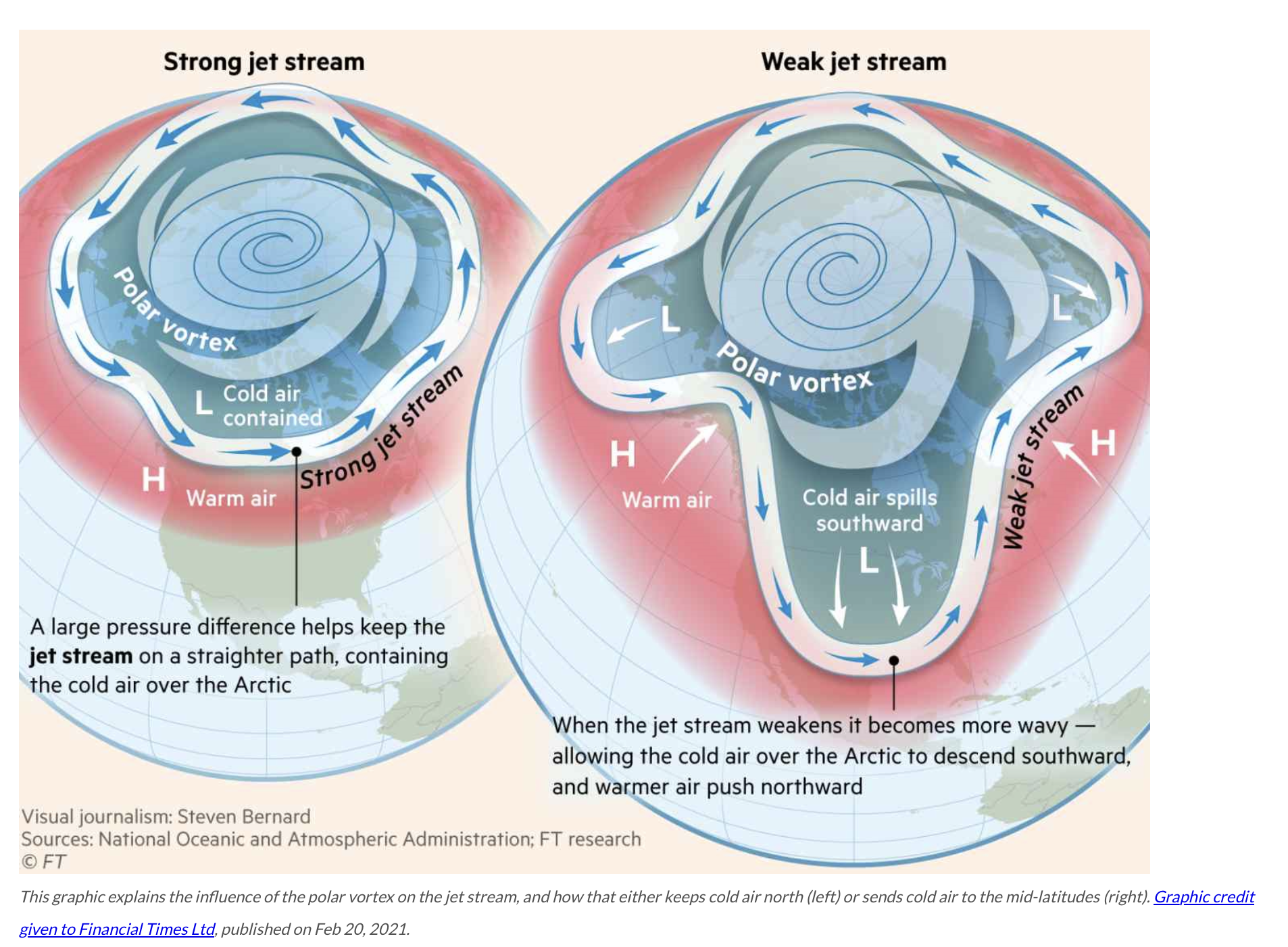

An historic stratospheric warming event: Implications for early winter weather?

A stratospheric warming event is a rapid temperature increase in the stratosphere that weakens or disrupts the polar vortex, potentially causing much colder surface weather to extend into the mid-latitudes.

However, for now, the warm weather I talked about returning to the US two weeks ago (I was a bit early) is short-term bearish for natural gas prices.

The warming you see here (30-50 miles up in the stratosphere) has only occurred twice this strongly in November. That was in 1958 and 1968. I will discuss this more with a video soon, but it opens the potential for a very cold December and possibly January in key US natural gas and heating oil demand areas (later).

These stratospheric events are often triggered by large-scale atmospheric waves that break apart the vortex, leading to a breakdown of the jet stream and allowing cold Arctic air to push southward. While not all events affect surface weather, they can lead to periods of prolonged, unusually cold, and wintry conditions.

Bottom line: Two months ago I discussed a possible warm early winter. Early November was colder in key US natural gas consumption regions then I initially predicted. Strong LNG exports and AI technology which uses a lot of natural gas were also the main impetus for a natural gas price strike. Traders were also building in “weather risk” winter premium because of this potential cold December weather pattern. I look for a early winter bull market in natural gas and for prices to trend higher. I see a much colder U.S. winter now due to stratospheric warming and a weak La Nina

(See the WeatherWealth Trade section for trading ideas)

WEATHER WEALTH TRADE IDEAS

From natural gas futures and options to longer-term grain trading strategies, please receive a two week FREE TRIAL (CLICK ON LINK). It costs just $1 and you can cancel at anytime.