4:30 a.m. EDT – October 16th

In this report:

Weather Spider update from Wednesday

Discussion of all Ag and natural gas commodity markets

The boom in silver prices

I updated this Spider on Wednesday morning EDT, October 15th

A couple of weeks ago, my highest confidence trades were shorting rallies in coffee and being short natural gas into the late autumn. The natural gas trade has worked out great if you took it, coffee, may eventually work (very complicated). Short call options longer term in coffee is the safest way to play this market.

The report below discusses the fundamentals affecting all of these markets and my Spider scores.

My next update will come on Tuesday, October 21st

Sugar (-3): Market breaks key support levels on weak crude oil prices and big global crops

One of my best trades over the last few months, I have maintained a longer-term bearish outlook due to my prediction of improved global crops last April, such as a great Indian Monsoon. Lower crude prices have also helped this market remain under pressure.

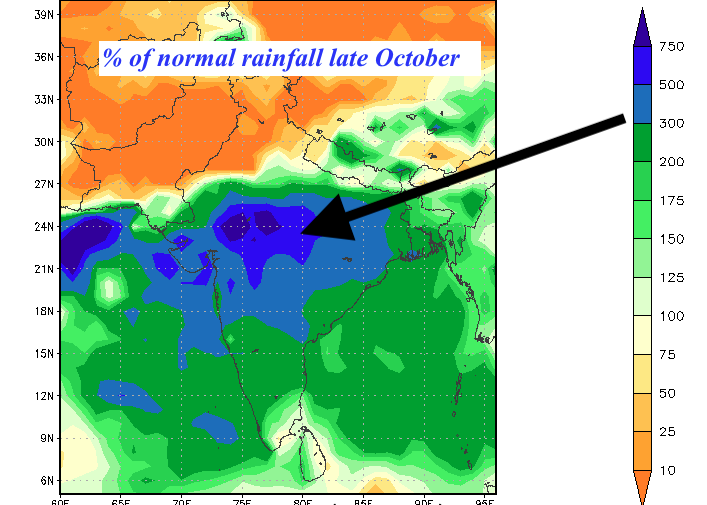

The Weather Spider was scaled back from bearish to neutral to slightly bearish due to heavy rains hitting India that may cause some quality issues.

It should be noted that, unlike grain markets in summer or the natural gas market in the fall and winter (which react immediately to short-term weather forecasts), it may be weeks or months before any potential “downgrade” in the Indian crop occurs. Hence, this may not be a market factor for a while with most fundamentals still remaining overwhelmingly bearish…

My one concern from a weather perspective “might be” that it’s getting too wet in India. The harvest usually begins in November and could cause some quality issues later. Typically, however, La Niña events result in lower prices longer term.

The weaker dollar and a big short position have helped prices bounce off their lows, but the longer-term charts and low crude prices keep me cautiously bearish on rallies.

On Tuesday, I advised that short-term traders, who may have sold March sugar a few weeks ago, take a small-modest profit of between $600-$1,000 a contract. Otherwise, if dry weather returns to India later and crude prices stay low, it is possible sugar prices could reach 12-13¢ next year. Hence, traders may still be long the March 16¢ put option from a month or so ago with small profits.

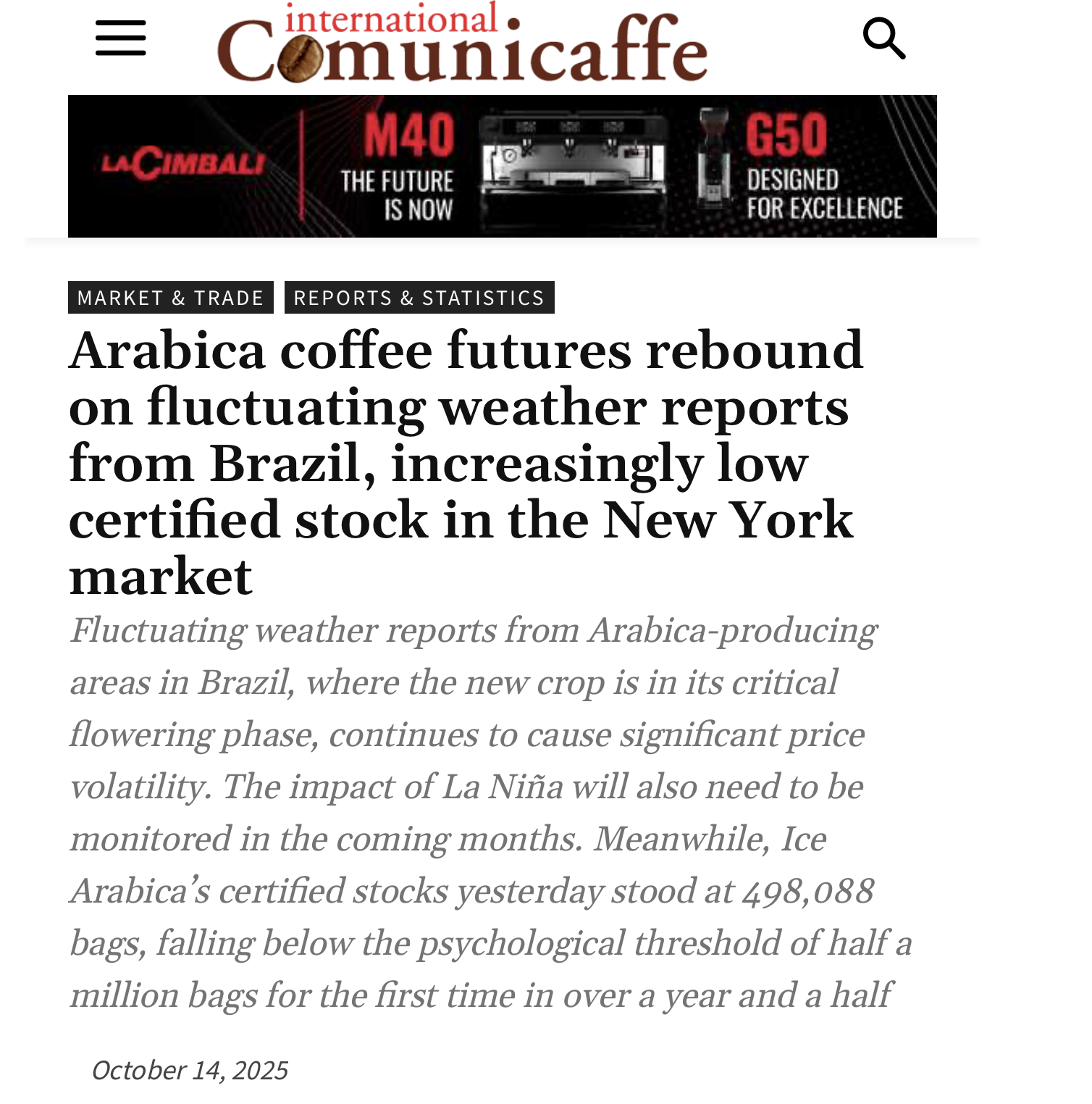

Coffee: Arabica (-2), Robusta (-0): Incredibly complex market (using options for potential longer-term bearish move is safest !)

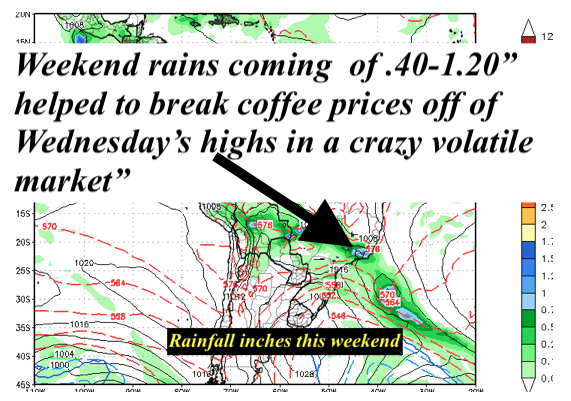

Late on Wednesday, the coffee market crashed due to rain forecasts in Brazil this weekend. This is nothing new, I have been saying this would happen for 2 weeks.

The Weather Spider was raised slightly somewhat from a -7 (bearish to very bearish) to a -2 (neutral to slightly bearish). This is due to no new resolution in the Trade War with Brazil, the fact that up until this coming weekend, there hasn’t been enough rain in Brazil for the flowering, and due to very tight certified stocks. The chart pattern also became a bit more friendly when we bounced off support earlier this week.

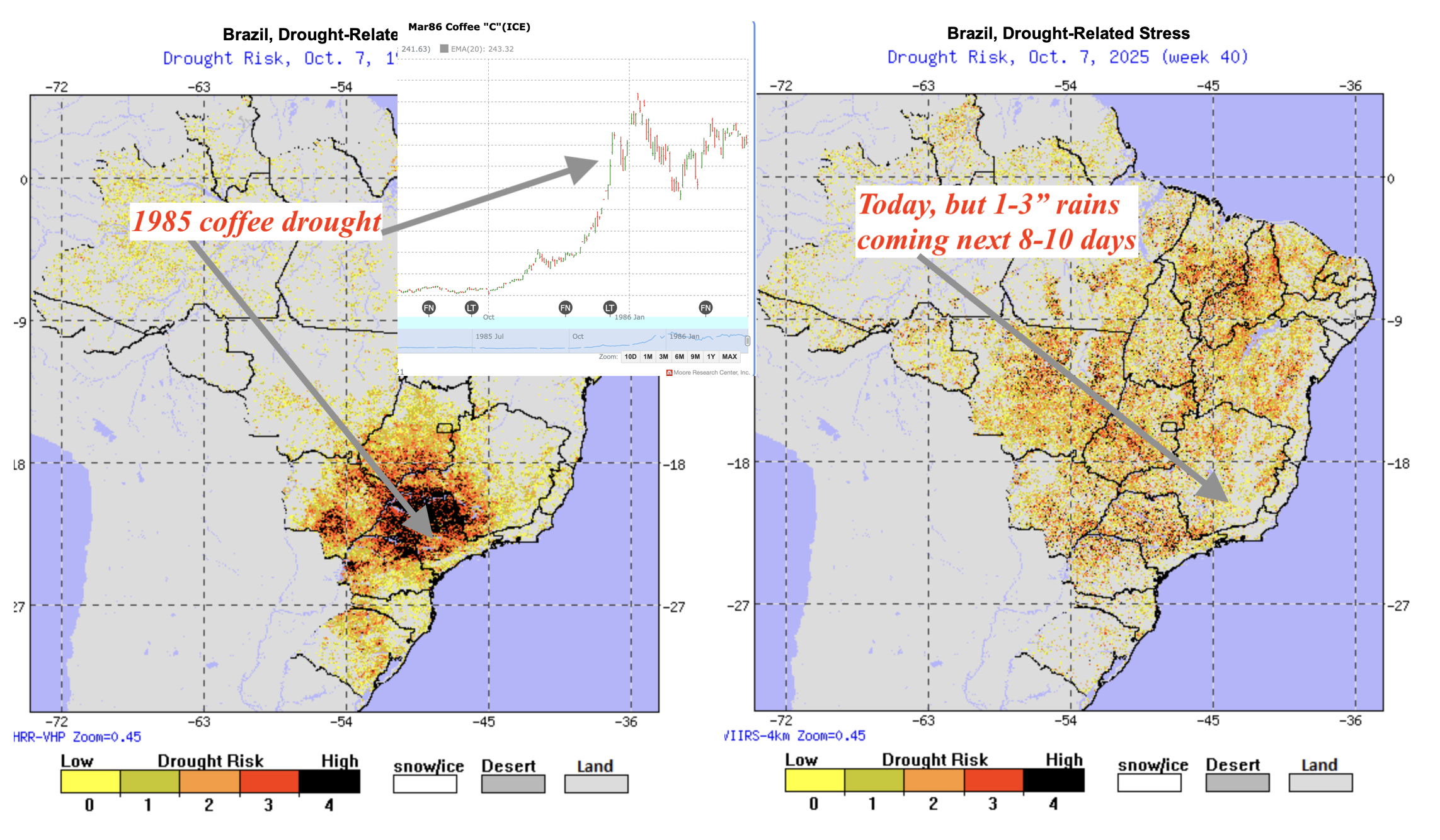

Some analysts are comparing the weather and crop situation in Brazil to the severe drought and major coffee bull market of 1985. However, back then, most of the coffee was grown in São Paulo and Parana, where a severe drought (dark red) cut production sharply (map to the left).

There are still some crop concerns in Brazil, and my weather forecast for good rains for the next 10-15 days still holds. However, it remains to be seen if: a) the Trade War with Brazil will be resolved; b) whether or not crop problems will occur later after this rain.

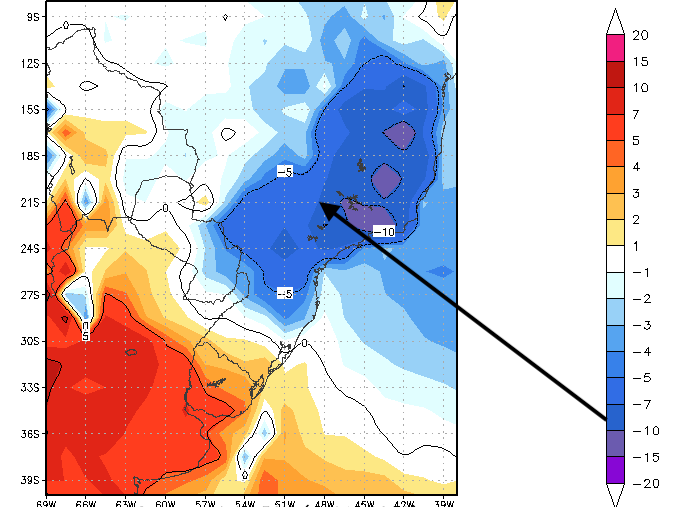

One reason why I was recently bearish on coffee was due to this cooler weather you see here during the critical time of Brazil’s coffee bloom stage.

You can see to the right the drought monitor map still illustrating some recent concerns from several years of Brazil’s crop problems, droughts, frosts, etc. This is creating wild market volatility.

Rains will hit key Brazil coffee areas this weekend, with some places in southern areas seeing 1-2″ of rain. The rains will move north early to mid-next week, but is it enough? Some models are turning dry after this, and this, too, has kept coffee prices from falling again. A lot is still unknown about the 2026-27 crop. However, I want to stick to my guns and second-guess models that with time, rains will improve crop conditions for Brazil coffee based on my long-range research.

I am bearish coffee longer term and my spider should become at least a -5 to -7 if there is a Trade Tariff resolution later.

Using potentially longer-term short $5.00, March call options from a month ago and long March 2026 put options spreads were/are the only way to play this market. If you did sell futures earlier this week or late last week, my trading advice was that you had to risk a stop to $4.00, which is too risky for the average trader. Could prices fall to $3.00-$3.30 at some point in 2026? It is possible. Again, unless you can stomach enormous volatility and $12,000 risk to $4 you may just want to scratch the trade as we are down 300-500 points in coffee as of this writing.

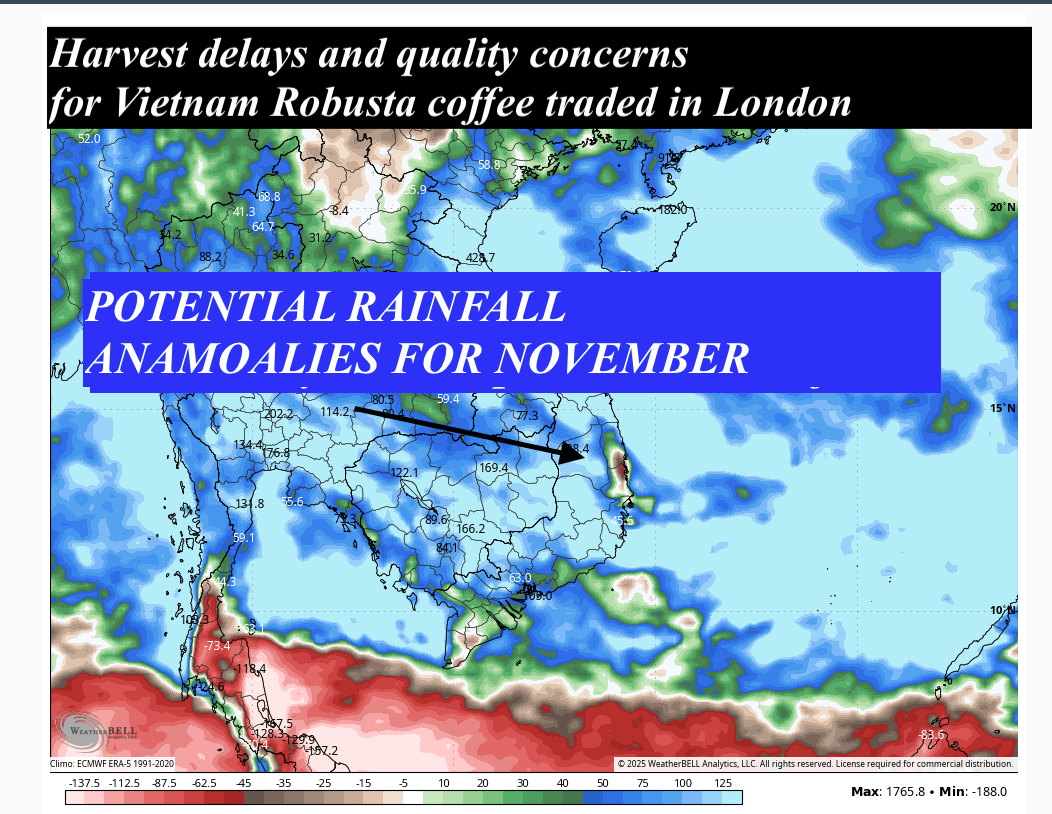

Yes, I may be wrong, and crop problems could resume for Brazil later on, and prices will soar. However, again most of my earlier studies did suggest a rebound in global production next year. In addition, the Robusta harvest in Vietnam appears to be improving.

Drier weather for Vietnam and a big crop is potentially bearish Robusta London coffee prices, longer-term. However, La Niña type wetness may return by November and be a background supportive factor later.

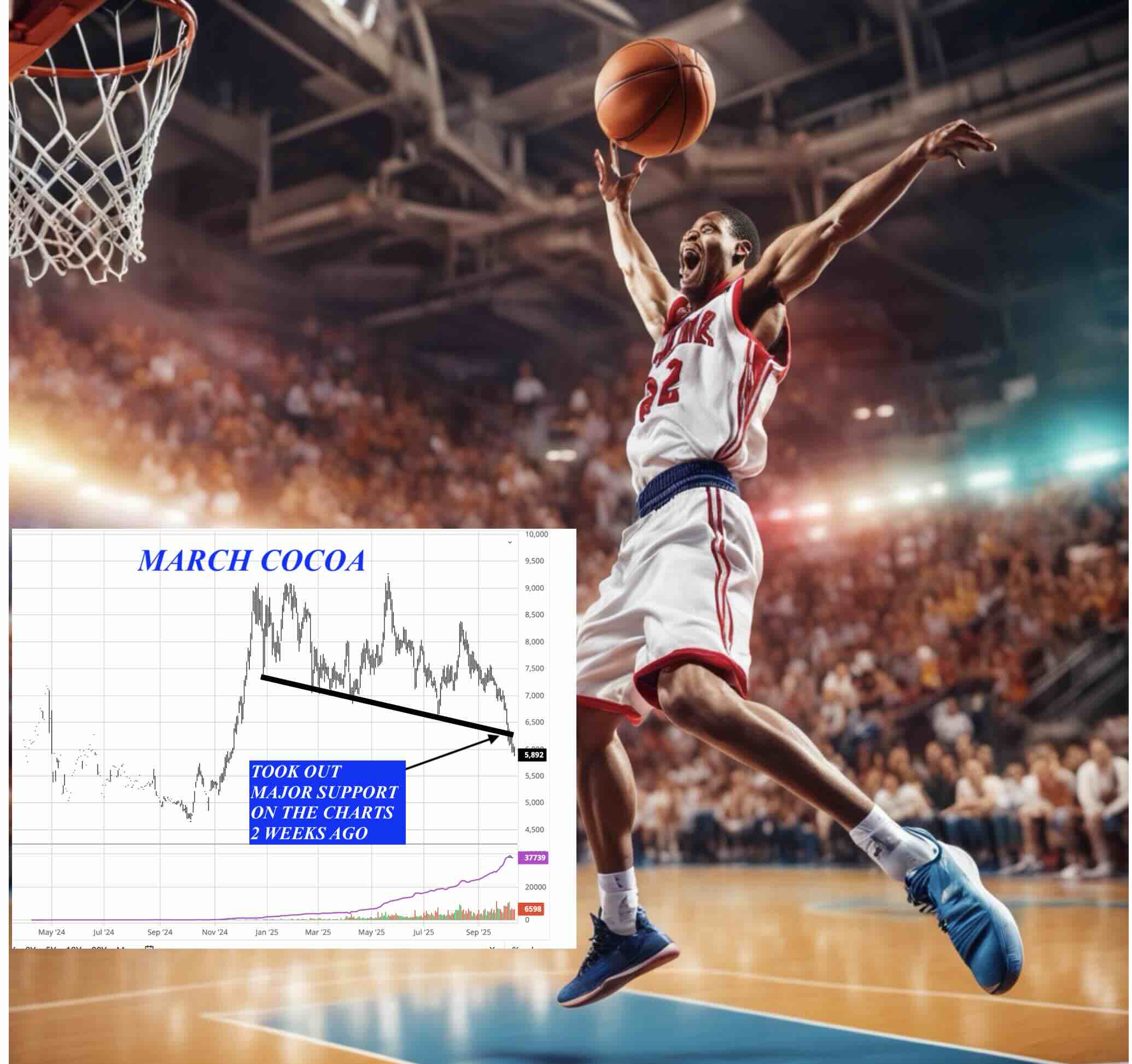

Cocoa (-4): Poor demand, seasonal bearish factors and improved West African weather created a 25% collapse in prices. Market may be over-sold now.

The score is not quite as bearish as it was three to four weeks ago, as we already had a massive 20% break in prices I predicted. But just because a market is cheap is NO reason to buy something, but we could see some short-covering.

Given generally dry weather for the main crop harvest, poor demand, and the chart pattern, all I see is some occasional short-covering. However, longer-term with La Niña, if there is no West African Harmattan wind this winter, cocoa prices might reach $5,000 sometime next year (not sure).

I cannot say with any great confidence that one should bottom pick and buy this market just based on the weather… it is tempting, so do that at your own risk.

This report that I published a couple of weeks ago, was a “slam dunk” sell in cocoa, just before the additional 10-15% collapse in prices.

September 22nd

Corn (+2): Biding its time with mixed fundamentals and no clear-cut direction.

The lower US corn crop due to disease issues has this Spider neutral to friendly.

However, due to harvest pressure and questions still about Trade Tariffs, I have had new advice for several months. The last big trade was shorting corn last April or May on my longer-term view of a big summer crop and ideal yields.

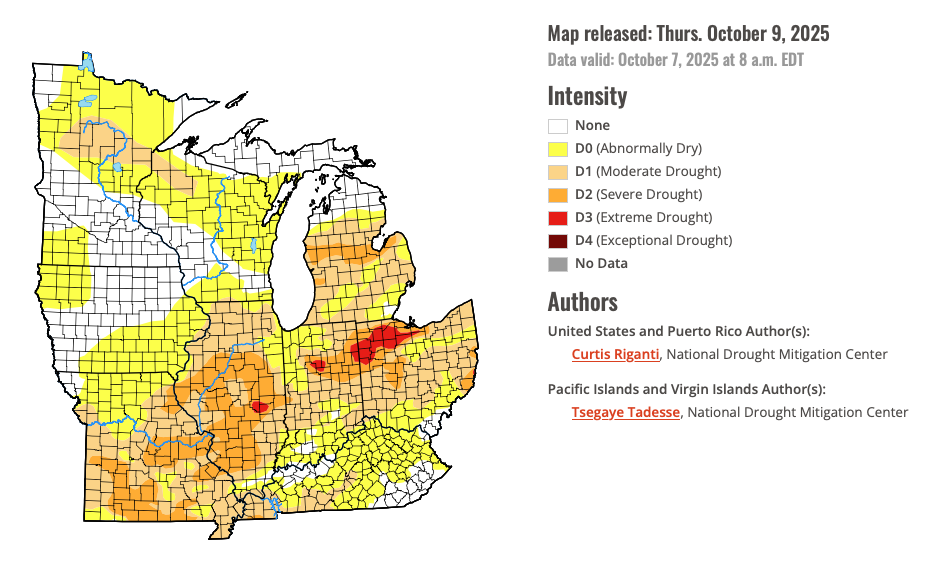

The drought monitor below will be a potential bullish factor if La Niña lasts well into next year. Is that still questionable? Of more importance after the US harvest will be the South American weather.

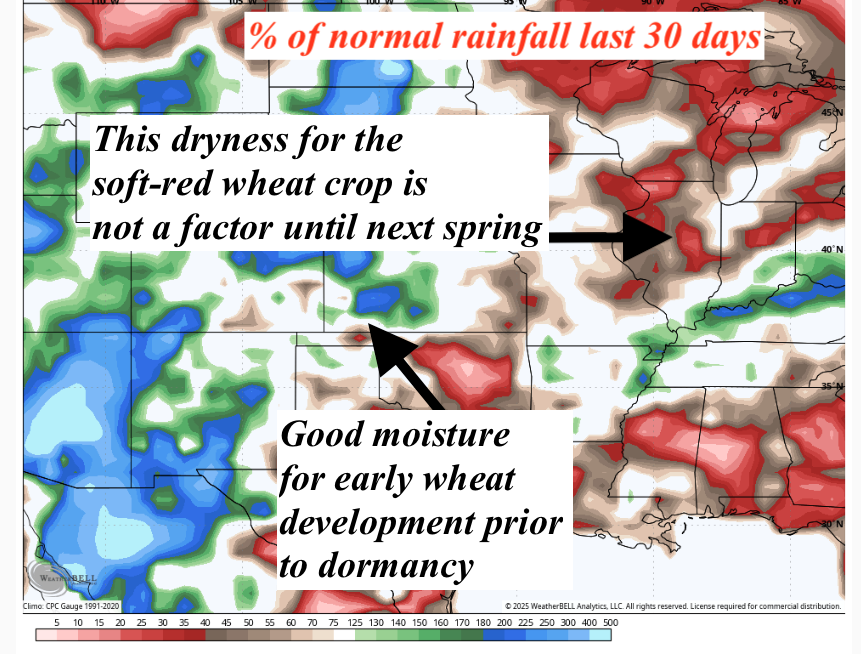

Wheat (-2): A decent Australian crop, recent good moisture for Plains wheat, and the bearish chart pattern

The chart formation and demand worries continue to keep this market in a longer-term downtrend. For the most part, I have been bearish on this market again since spring and summer, with generally good global crops.

However, I have had no new specific advice until we see how La Niña plays out, the charts look better, and demand picks up.

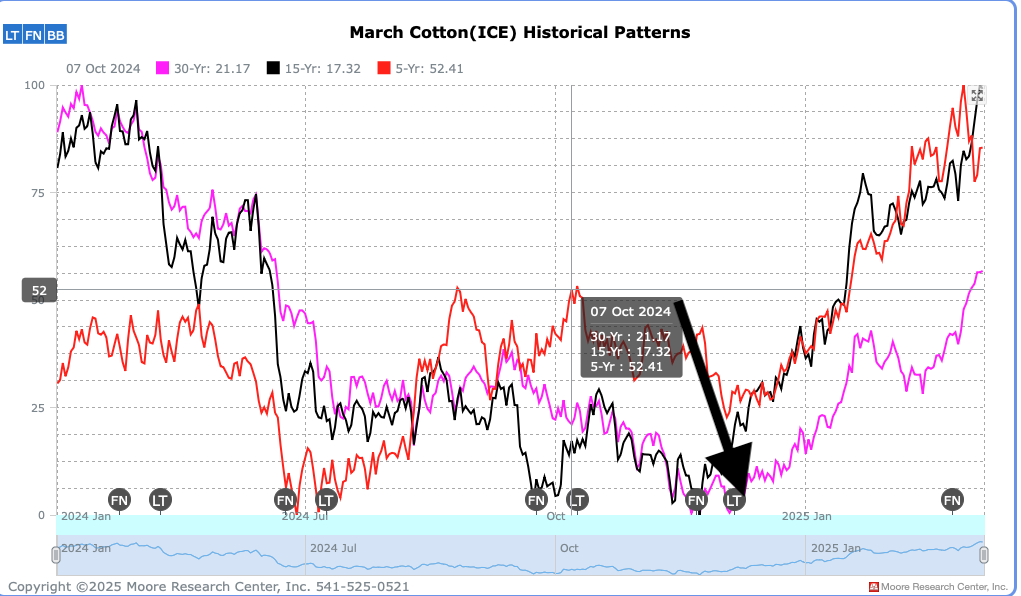

Cotton (-2): Market breaks support on low crude prices, Trade Tariffs, and seasonal factors.

I have no advice in this market all spring and summer. My Weather Spider has been neutral for six months. Notice how the narrow chart pattern with no market direction was indeed the case. In commodity markets with choppy price action but in a narrow price band, the way to play these markets is by selling strangles. This catches the price movement between two strike prices.

Nevertheless, I have not been focusing on this market and really have no advice.

Seasonally, prices go lower by early October into late November. Hence, the chart pattern is turning bearish for the first time, and concerns about low crude prices and Trade Tariffs have my Spider slightly bearish.

Soybeans (-2): Too many different fundamentals to digest

Trade Tariff concerns, most analysts not really lowering their US crop estimate even with a dry late Midwest summer (it was not hot), and harvest pressure continues to keep any rally at bay. We will need to see a trade agreement with China, demand pick up, and weather problems in South America to warrant any chance for a bull market. For now, that is not in the cards just yet

I have no new advice in this market. The last few trades were mostly short call options last summer that were profitable on my prediction of big US crops.

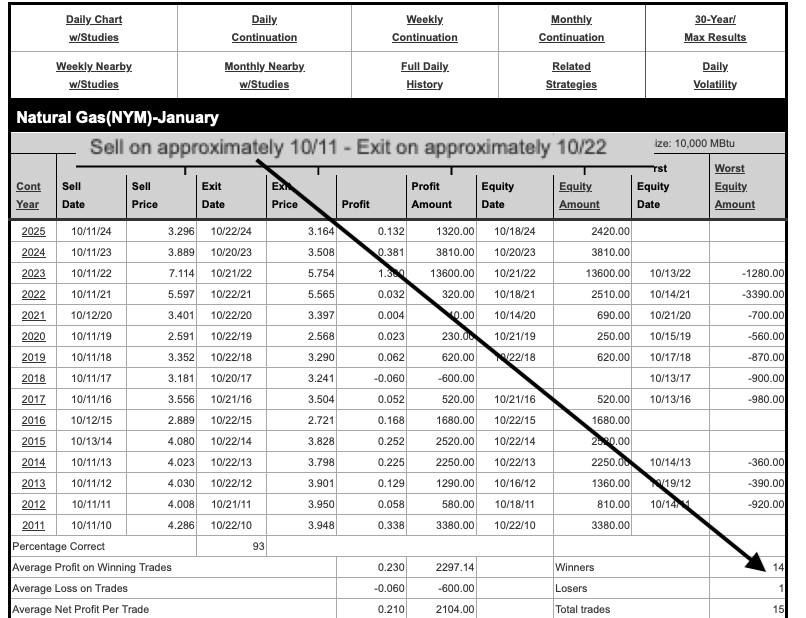

Natural Gas (-6): Prices collapse as I predicted two to three weeks ago. Warm U.S. October weather almost always means lower prices due to weak demand. I do not recommend selling the market on a 40¢ break in the hole.

As mentioned over the last week, I was a bit early two to three weeks ago with my overall bearish view on warm Fall weather. I pointed out many times, this seasonal trade is short when October is warmer than normal !!

There may be some signs of colder early November weather later, so even though my spider has been quite bearish recently DOES NOT imply selling natural gas in the hole. The spider may become more neutral soon due to the big short position and seasonal bearish tendencies.

Seasonal to be short natural gas ends shortly, especially if there are some signs of cooler November weather.

Too many specs and commercials got all excited about a hot late summer and strong LNG exports overseas.

We have already seen the nearby November contract collapse 10-15% in less than a week. That is a shame because three weeks ago, I recommended aggressive traders sell November natural gas, only to be stopped out.

Conservative traders were advised to take a long position two weeks ago in the inverse ETF (KOLD). At one point, the trade was behind 10% and as of this writing now up more than 15%. Take the profits short this natural gas ETF and walk away. I also recommended selling the December $4.20 call option in the face of a big rally a couple of weeks ago. That trade is up around $1,000 a contract.

The historic bull market in silver

Click on the video below

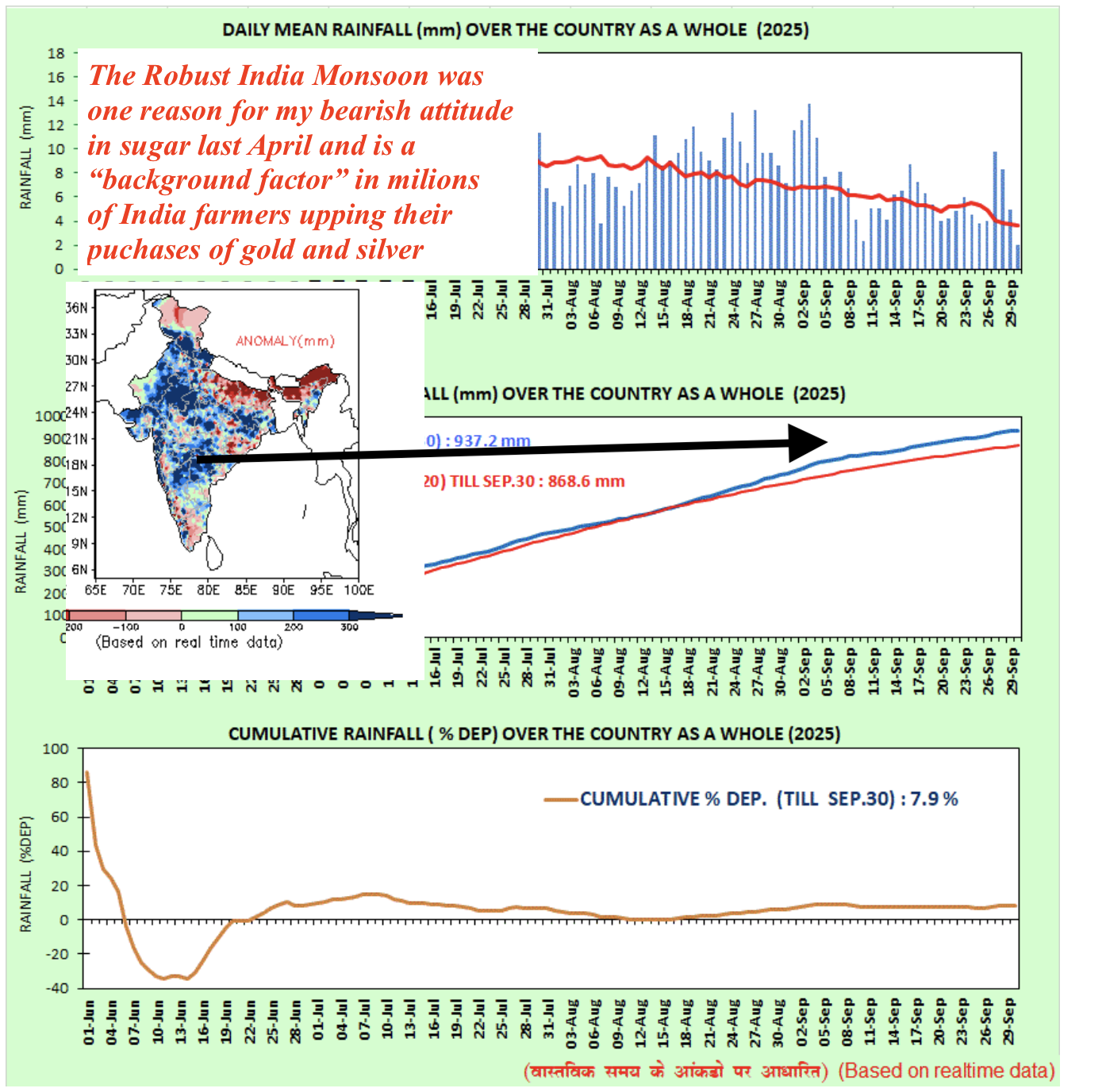

Silver prices have risen sharply in October 2025 due to a combination of high industrial demand, increasing investor interest in precious metals as safe havens, and a persistent supply deficit. I normally do not advise in precious metals, but this was a trade I was pretty confident about. The weather is a slight background factor.

A positive Indian monsoon season, which can boost rural demand for silver during the festive season, is a contributing factor, though it is one of several key drivers.

It is for these reasons and given the chart formation, that back in April. I mentioned that I thought silver prices would soar.

Factors driving silver prices in October 2025:

High industrial demand

- Renewable energy: The clean energy transition, led by the growth of solar photovoltaic (PV) technology, is a primary driver. Silver is a critical component in solar panels, and increased global installation has significantly boosted demand. This is something pretty close to my heart.

- Electronics and vehicles: Demand for silver is also rising in other industrial applications, including electric vehicles (EVs), 5G technology, and high-tech electronics.

Safe-haven investment

- Geopolitical and economic uncertainty: Escalating global tensions and concerns over a growing U.S. fiscal deficit have prompted investors to seek refuge in precious metals.

- Inflation hedge: With persistent inflationary pressures and the potential for a weaker U.S. dollar, investors are turning to silver as a store of value.

- Amplified movement: As a more volatile asset than gold, silver has historically seen larger price swings during bull runs, which can attract momentum-driven investors.

Structural supply deficit

- Production lagging demand: For several consecutive years, the global silver market has experienced a supply deficit, meaning demand is consistently outpacing mine production and recycling.

- Byproduct production: The supply issue is compounded by the fact that roughly 70% of silver is a byproduct of mining other metals like zinc, copper, and gold. This limits how quickly silver output can increase in response to higher prices.

- Inventory drawdown: Visible inventories in key trading hubs, such as London, have dwindled as industrial and investment demand have absorbed available supplies.

Indian monsoon and festive season demand

- Monsoon’s effect on rural income: India is a major consumer of silver, especially in rural areas. A strong monsoon, as experienced in 2024, boosts agricultural yields and, consequently, rural incomes.

- Increased purchasing power: This higher disposable income often translates into increased purchases of precious metals for personal consumption, weddings, and as a store of value.

- Coincides with peak demand: The monsoon season’s end coincides with India’s peak festival and wedding seasons (September–December), a period of strong traditional demand for precious metals like silver.

- A supporting, not primary, driver: While a positive monsoon contributes to robust seasonal demand, particularly in the Indian market, it is a smaller piece of the puzzle compared to the fundamental issues of global industrial demand and the persistent supply-demand imbalance.

In summary, while the monsoon’s positive effect on rural demand in India helps, the significant surge in silver prices is fundamentally driven by a combination of booming global industrial usage, safe-haven investment during economic uncertainty, and a structural deficit in the worldwide market. Again, as I mentioned back in April, I think prices will reach $100 an ounce within two years. At present, there is a “short squeeze” at play, grabbing headlines in the commodity sphere.