In this Report:

Introduction

What are Atmospheric Rivers?

What usually happens to U.S./Canadian grain weather with unprecedented California winter rain and snowfall?

Looking at the best snowfall and winter ski seasons out west

When were Argentina’s worst soybean droughts?

Weakening La Niña events that had a negative PDO

Bringing it all together: What these three studies may portend for agricultural and natural gas commodities this spring/summer

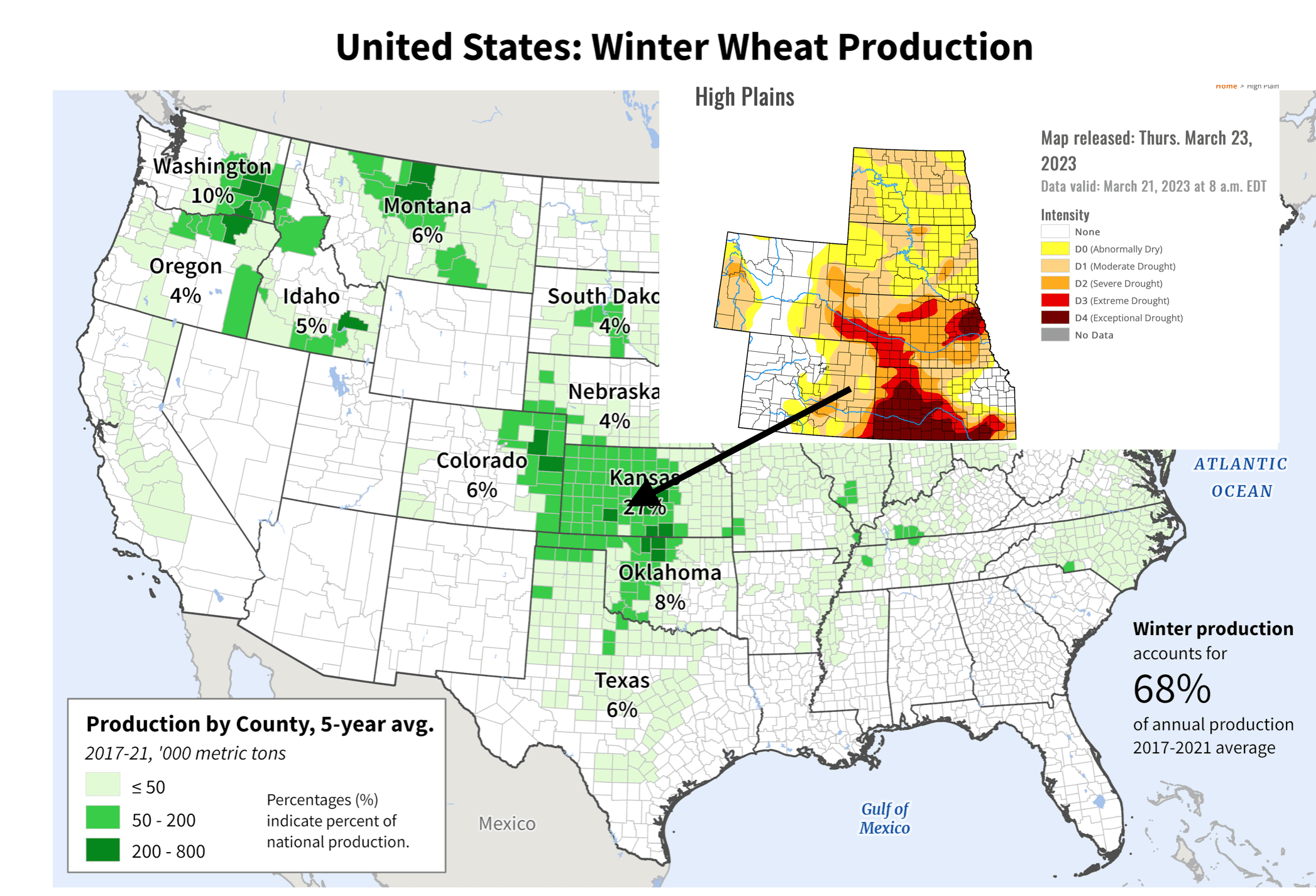

How Russia’s war on Ukraine and the worsening drought in Kansas have helped wheat price spreads soar

WeatherWealth Trade Ideas (bottom of the report)

Introduction:

In the weeks and months ahead I will be updating my longer-term view regarding spring and summer global weather (fall and winter in Australia). I will also try to forge ahead with investment views for various commodities.

This report focuses on how I predict long-range weather and some of my early opinions. I present four different studies, which I studied all of last week. In addition, I use our proprietary in-house analytic weather tool, Climatepredict.com, which I query in order to verify these studies, once it updates in early April, May and June.

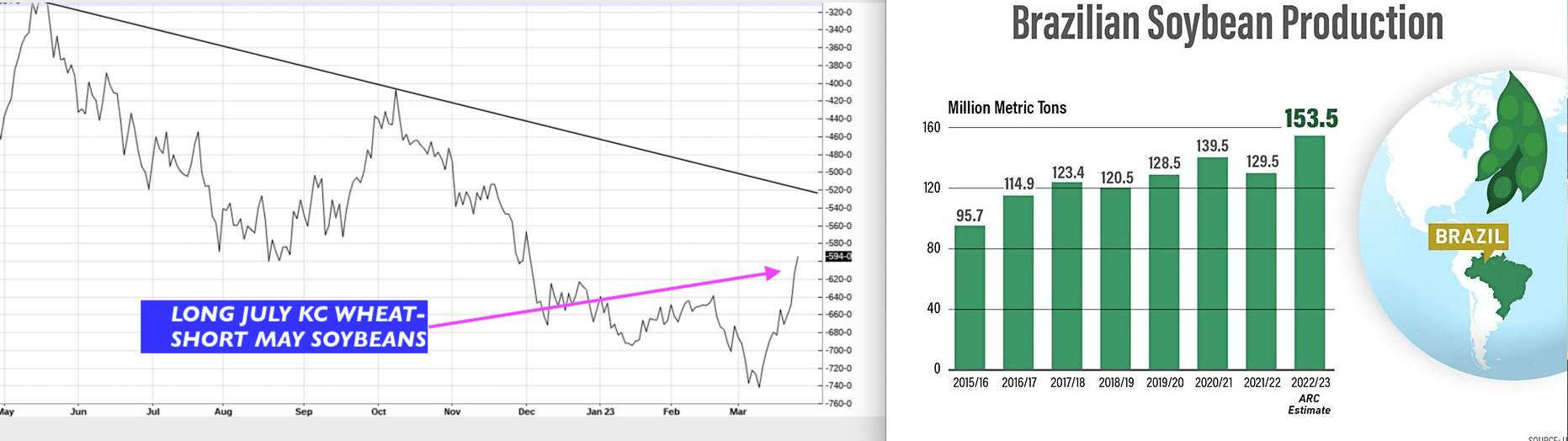

Currently, it is KC July wheat that has the most potential in grains due to the drought. I also am leaning towards a bearish summer view for new crop corn and soybeans, in which prices could collapse 15-30% by July and August.

It is possible corn and soybeans are oversold , but the huge Brazil soybean crop created a massive spiral down in prices, given the record long position in soybean meal.

Video about Atmospheric Rivers?

Click on the youtube video below

study #1

- The 1952 California flood: one of the most significant floods in California’s history, caused by a series of storms that hit the state between December 1951 and January 1952. It resulted in over 20 inches of rainfall in some areas.

- The 1969 Southern California floods: a series of storms that hit Southern California in January and February 1969, causing significant flooding and mudslides. It resulted in over 10 inches of rainfall in some areas.

- The 1986 California floods: a series of storms that hit California in February and March 1986, causing severe flooding and landslides throughout the state. It resulted in over 10 inches of rainfall in some areas.

- The 1995 California floods: a series of storms that hit California in January and February 1995, causing significant flooding and mudslides. It resulted in over 10 inches of rainfall in some areas.

- The 2017 California floods: a series of storms that hit California in January and February 2017, causing severe flooding and mudslides throughout the state. It resulted in over 10 inches of rainfall in some areas.

What usually happens to U.S./Canadian grain weather with unprecedented California winter rain and snowfall?

Study #1: Looking strictly at the wettest winters ever in California (shown above).

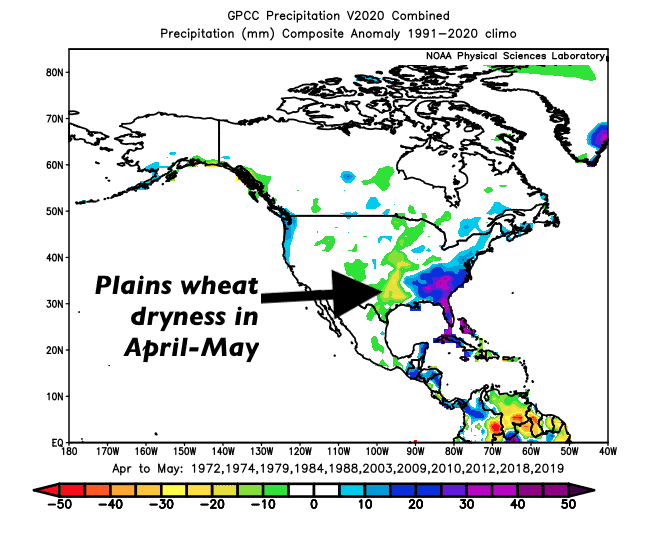

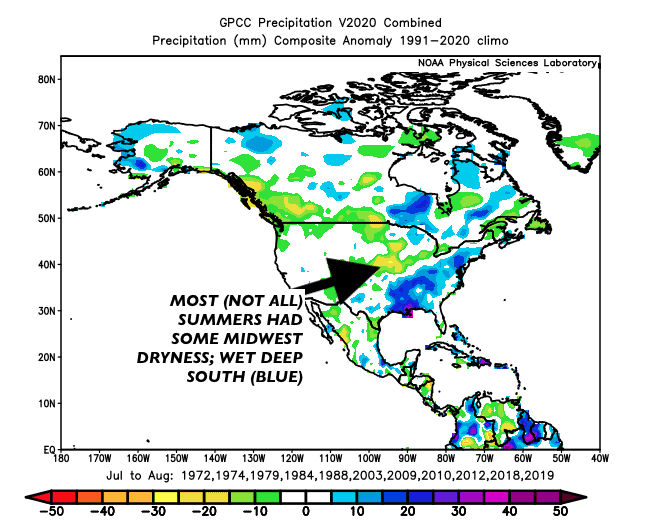

This study provides an analysis of the current state of the Plains wheat market, revealing that the prevailing drought conditions would subside during the spring season. This development would have an anticipated to have a bearish impact on the wheat market. Additionally, the study suggests that the upcoming summer weather may exhibit mixed trends for corn and soybean, with occasional bullish indicators. Furthermore, the research findings indicate that the natural gas market may experience slightly elevated temperatures during the summer season.

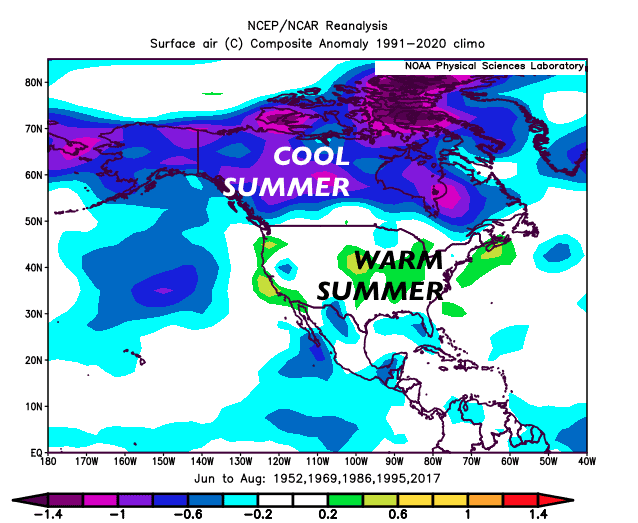

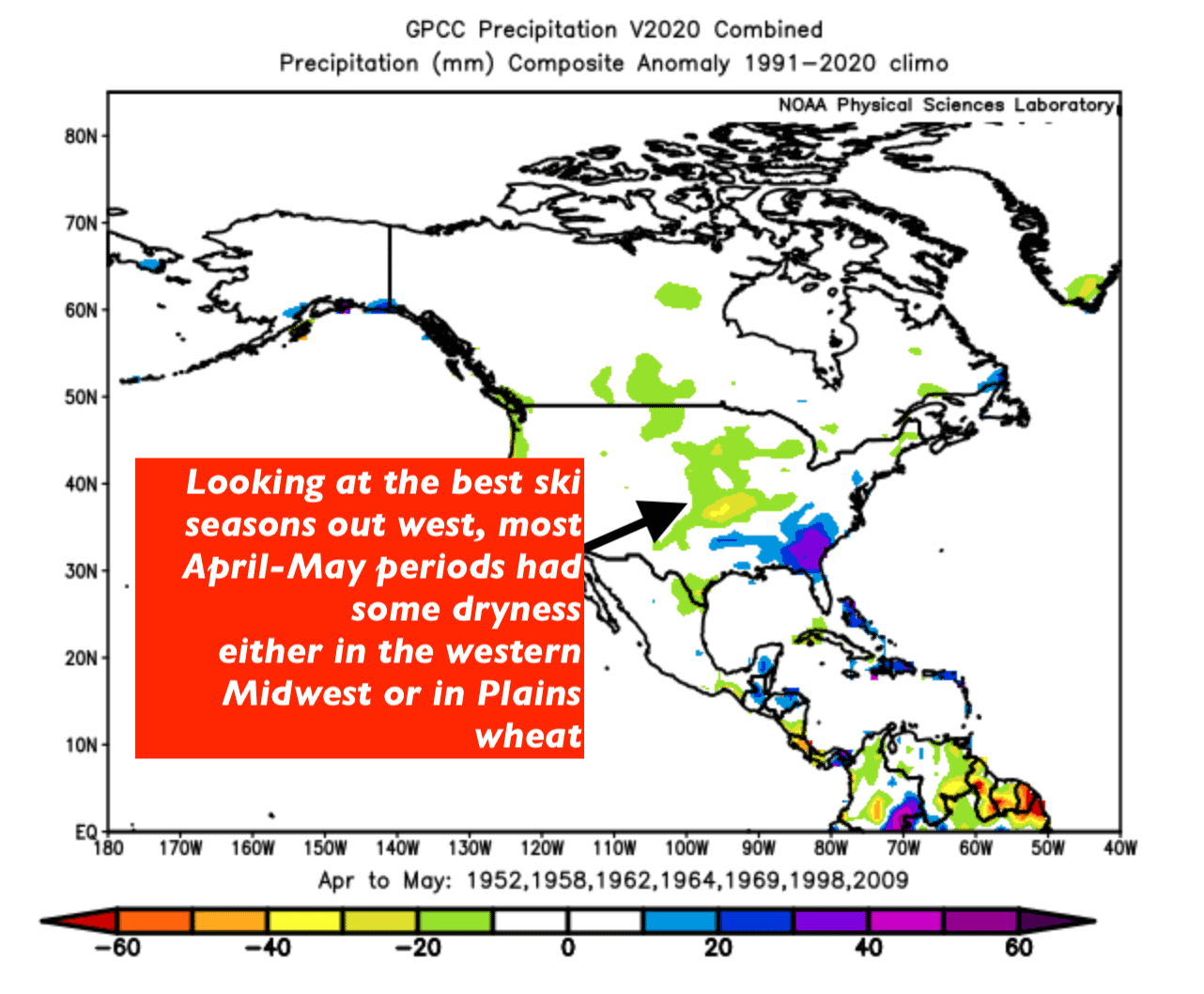

Looking at the best ski seasons out west

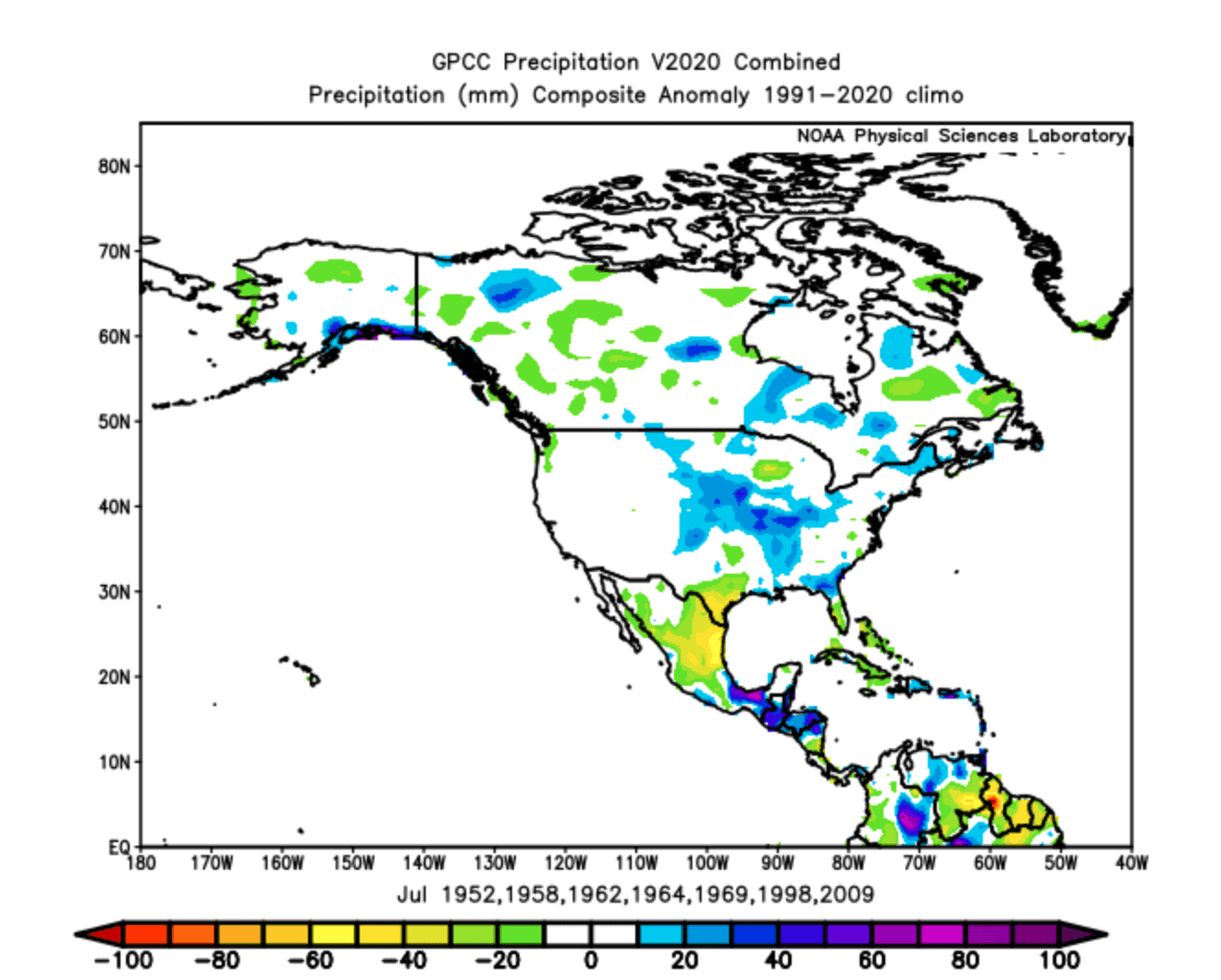

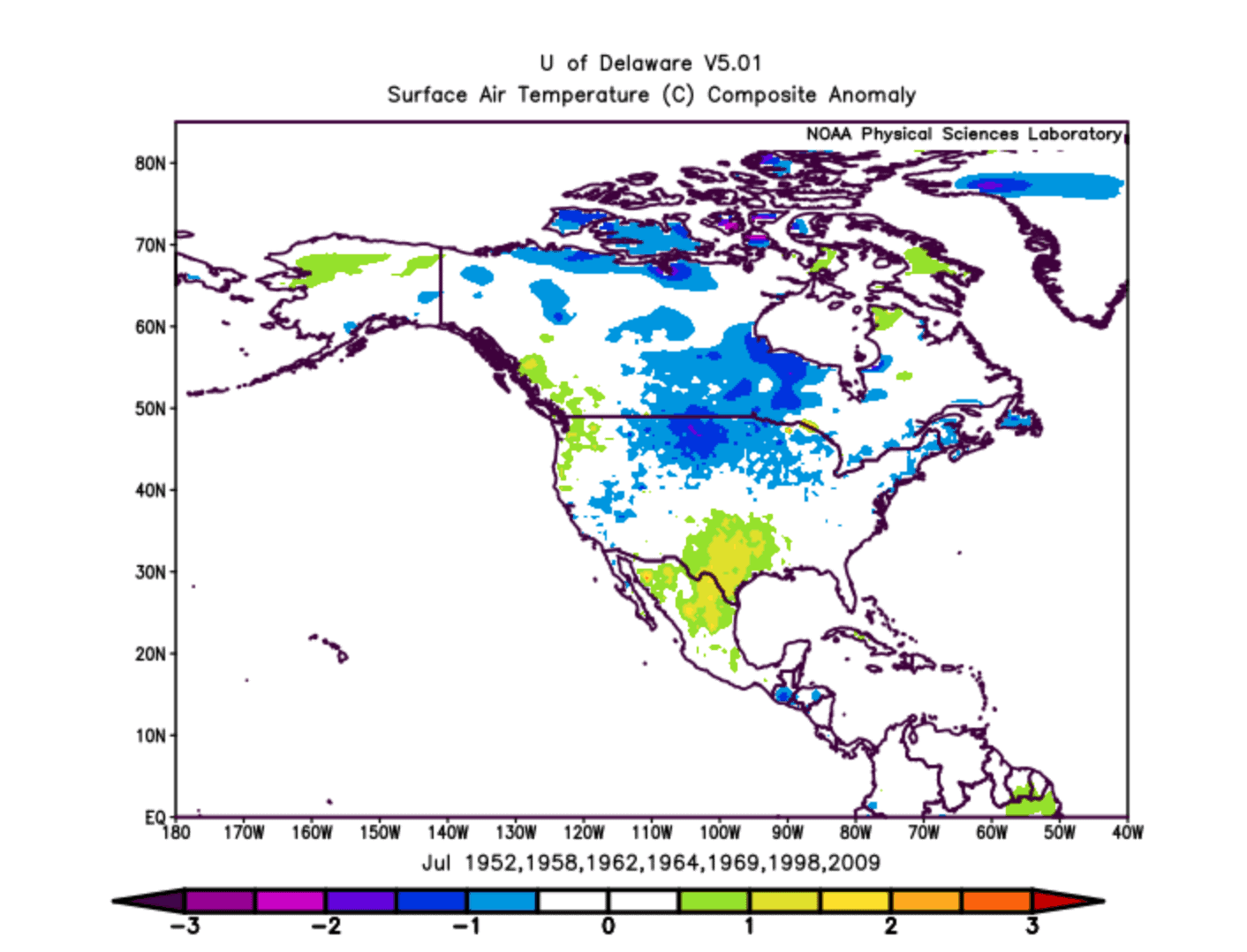

Study #2: This study portends continued dryness for Plains wheat, but a good summer for corn and soybean crops.

Just based on the heaviest winter snows out west and the best ski seasons, the two maps above illustrate July rainfall and temperatures. Generally, it points to a bearish July outlook for corn with cool wet weather over much of the Midwest

When were Argentina’s worst soybean droughts?

Study #3—This study looks strictly at the worst Argentina droughts. This year (2022-23) was actually the worst soybean drought in the last 50 years.

This study illustrates the likelihood for the Plains drought to continue. Most Argentina droughts did have Midwest summer corn and/or soybean weather problems, as shown below. However, a lot will depend on the timing of whether El Niño develops or not.

Source: Jim Roemer (CHAT GTP)

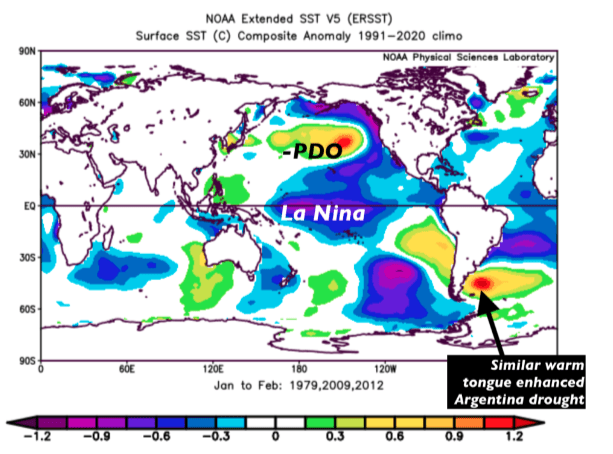

Weakening La Nina events that had a -PDO.

Study #4: Weakening La Niña events and the negative PDO

La Niña, El Niño, and the PDO in the northern Pacific have huge impacts on spring and summer weather for commodities. I will discuss more of this in due time. Currently, three years were the most similar to today, regardless if there were atmospheric rivers and a big western ski season, or not.

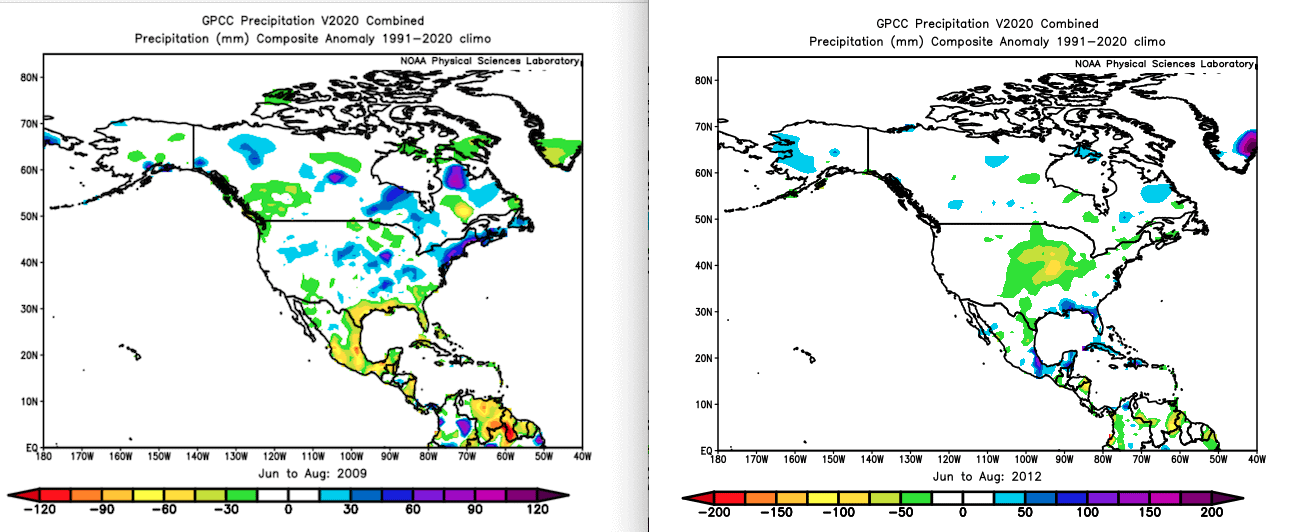

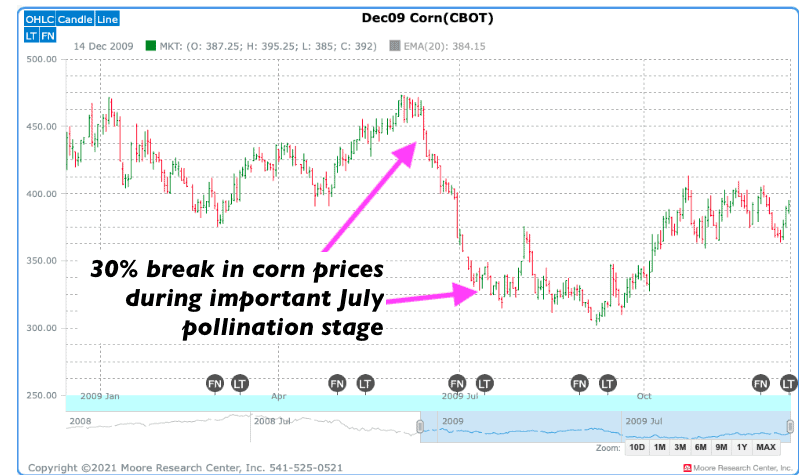

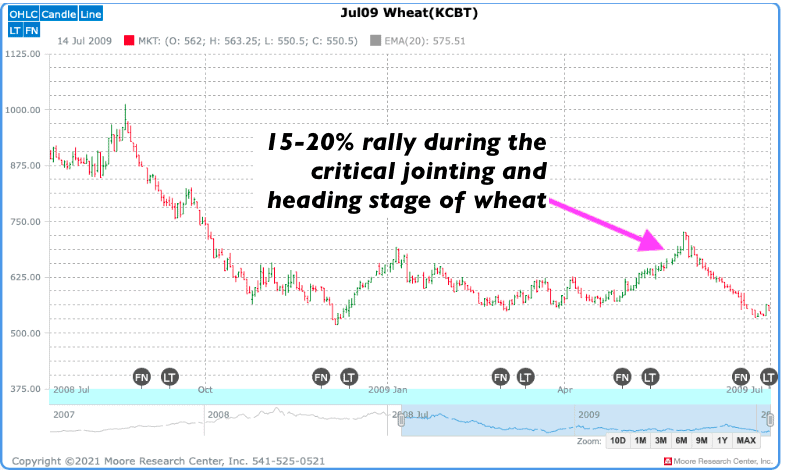

Out of these three years (1979,2009 and 2012), March of 2009 and 2012 had similar weakening La Niña events. In fact, like today, 2012 was the third consecutive year of La Niña–something that has only happened three other times since 1950.

Notice the difference in the weather patterns for summer grains. On the left, a wet and cool Midwest summer (blue) and sharply lower corn and soybean prices. On the right, is the infamous corn belt summer drought and heat wave.

June to August rainfall: Bearish (left) 2009 & bullish (right) 2012 Midwest drought

Hence, these are two different scenarios for summer grain production.

Bringing it all together: What these four studies may portend

Identifying the most reliable study for predicting long-range weather patterns is a complex task. The potential impact of a warming climate on weather patterns makes it difficult to accurately predict future trends based solely on analog years. However, by analyzing available data, we can discern general indications regarding long-range weather. Therefore, the question of the most reliable study for predicting long-range weather remains a challenging and multi-faceted issue. I will have more details soon.

However, it appears to me that 2009 might be the closet analog, with respect to: a) A drought in Argentina; b) A good ski season out west; c) Several big California winter storms (nothing like today); d) A weakening La Niña and a negative PDO in the Pacific. I will discuss many commodities and my longer-term view soon

How global weather and Russia’s war on Ukraine are affecting wheat spreads

The news regarding Russian grain export manipulation, coupled with the challenge of monitoring global weather patterns, poses a significant challenge to market analysts. The upcoming season will require close monitoring of weather conditions in both Europe and Russia, which adds a layer of complexity to the already intricate task of forecasting grain markets. Despite these challenges, it is my professional opinion that the market is poised for a bullish trend in KC wheat.

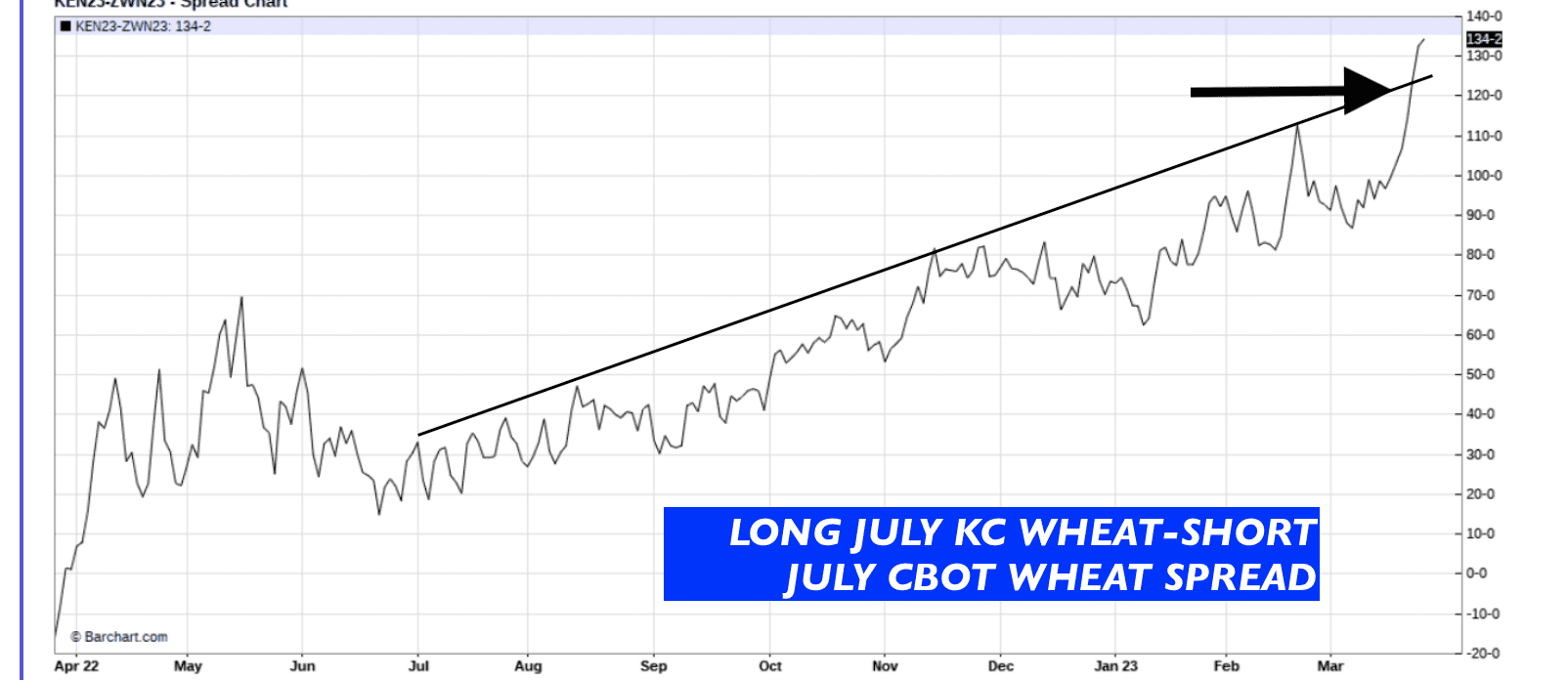

This spread has already soared to record levels. KC wheat is now about $1.40 above Chicago wheat.

WEATHERWEALTH TRADE IDEAS

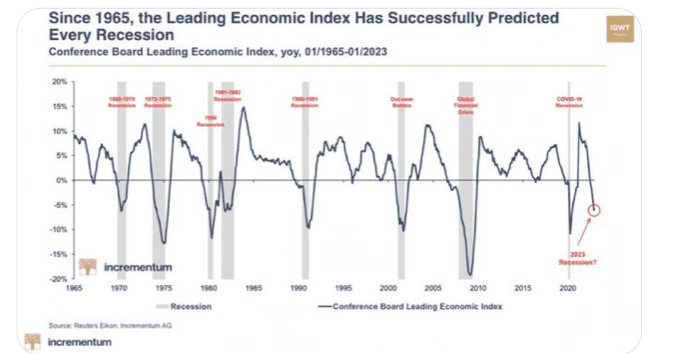

I am more concerned about the global economy and the banking system. It is my belief that global government actions to shore up bank problems are just a band-aid. With that said, potentially bearish outside markets and most of my studies above about decent corn/soybean belt summer weather should be bearish grains, longer term.

While I do not claim to be an economist, the table above is worrisome. What happens with the economy, various items regarding Russian grain exports (or not), plus the U.S. dollar (and, of course, weather) will have a big impact on commodities.

Stay tuned as we get into the Northern Hemisphere planting season.

GRAINS—Soybean prices collapse on bigger Brazil crop and improved harvest weather, while KC wheat trying to rally on Plains drought

If you read my updates last week I mentioned my more bearish attitude toward soybeans with prices some 70 cents higher than this, as well as a longer-term bearish summer view for December corn.

Unfortunately, I caught wind of the new weather problems for Indian wheat (not just the Plains drought) on Thursday. WeatherWealth is usually sent out twice a week and before that.

In addition, Russia may cut off wheat exports again. Earlier last week, I mentioned NOT to be short wheat and did advise premium clients about my more bullish attitude in KC July wheat.

Two to three weeks ago, I advised to take decent profits on short wheat positions. At this point, given the political uncertainty in Russia and the fact that they can make announcements about grain exports (or not) at any moment causing huge moves in wheat futures, it is risky to trade grains.

Two weeks ago, traders may have liquidated short July KC wheat with at least a $2,000-$3,000/contract profit and were stopped out of long May soybeans at $14.90 with about a $400 loss. My bias is bullish KC July wheat, especially if we see some sort of 10-20 cent price break.

I also mentioned a potential longer-term bearish attitude in the new crop December corn a few weeks ago and prices collapsed. I think the odds would favor $11 Nov beans at the end of the summer and possibly $4.00 Dec. corn. However, the growing season has not even started yet and there could be many important trading opportunities in the months ahead.

NATURAL GAS—Slightly colder than normal late winter, but huge global supplies and warm European winter continue to pressure prices

Around $2.50, I advised having a break-even stop a few weeks ago on any long ETF (UNG/BOIL) or mini-futures contract. On the colder than normal late winter, I did recommend more than a month ago, selling the April for $2.50 put option for 22 cents ($2,200 a contract).

The short $2.50 April put expires shortly and, as of this writing, traders who did this may be out about $800-$1,300 a contract. Following several successful big trades, (earlier this winter or last fall), short call options, mini futures, or the inverse ETF (KOLD) in the last month or so we have had some small losing trades from the long side. My confidence is low in this market, but I expect a major short covering rally deeper into spring and ahead of summer.

COFFEE—Following the outside markets and bidding time with respect to 2023 global coffee weather and production

Traders have been in a July option strangle for 1-2 months (The short July $2.10 call and short the July $1.50 put). This trade is ahead about $1000

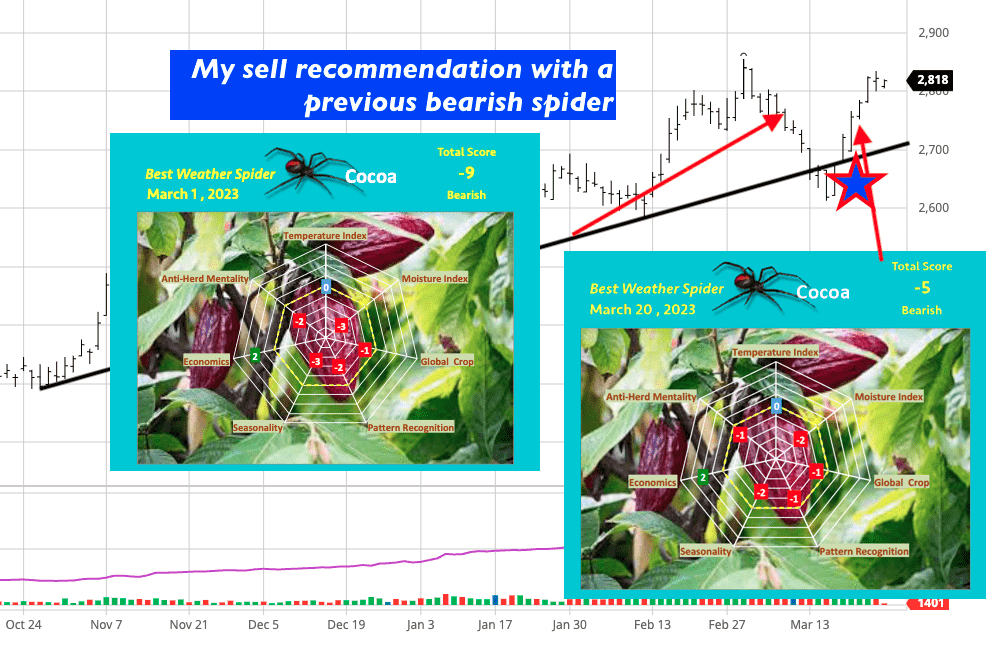

COCOA-–Other factors other than weather driving this market

Tight supplies and the worries over a lack of fertilizers for farmers have helped prices soar. We did not participate in this 20% rally the last few months in the ETN (NIB) or long futures because the weather is generally beneficial in west Africa.

On the first day of March, I advised selling May or July cocoa for around $2,800; at one point this trade was up $1,500 a contract. When trading, always put trailing stops in. Look how cocoa got below the trend line on improving West African weather but then came back above it (star). This is where one could have put trailing stops to preserve profits. However, I basically mentioned risking a break-even stop, last week.

El Niño talk, strong chocolate demand ahead of Easter, and very tight nearby stocks helped cocoa prices soar again last week.

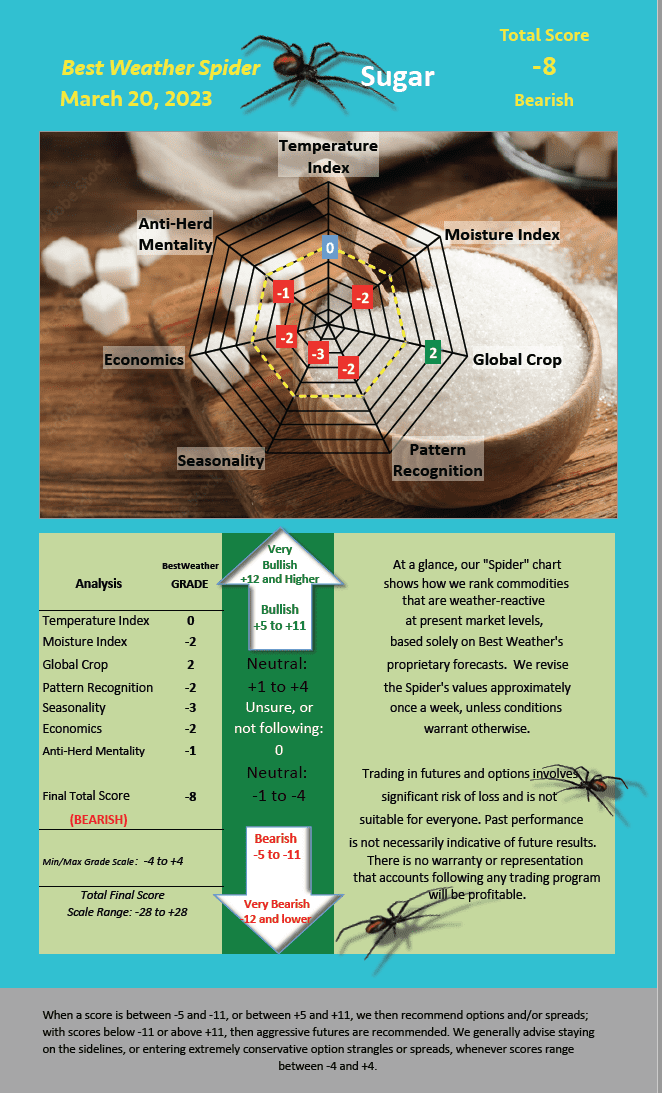

SUGAR—Strong seasonal factors for lower April prices. Whether El Niño forms this summer or autumn could have huge price implications.

Given the collapse in crude oil and the potential for global sugar production in 2023 to reach 180.4 MMT (a record), I am surprised that this market has not begun a downtrend.

Two months ago, I expressed my concern about a lower 2022 Indian crop, due to a delayed reaction to a combination of summer and fall droughts and floods. Nevertheless, my focus has been so much on the coffee, nat gas, and grain market that I really did not come out with any investment strategy.

Notice my Weather Spider a week ago. The economics are bearish (-2) due to lower crude prices and the dollar. Why is the moisture index bearish (good harvest weather for Brazil sugar) vs. my bullish (+2) for global crops? The lower Indian and European crop from 2022 has tightened nearby supplies helping prices rally.

Until we get into the 2023 growing season in Europe, Brazil and India, I am not following this market much. If the 2009 analog year I discussed above occurs, this could cause world weather problems for sugar, later. For now, my recent bias was to sell rallies in July sugar with low-moderate confidence.