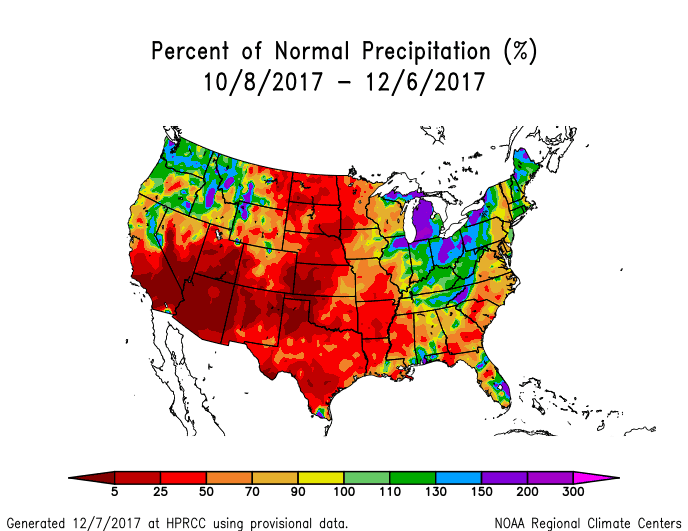

In the face of growing drought in the Plains and the historical brush fires out west, (which are causing sell-offs in certain insurance stocks and municipal bonds in parts of California are taking a hit) why has the wheat market not responded yet? The reason is due to the huge global supplies still hitting the market and the lower export prices in Russia, etc. due to record crops this past summer. Commercial grain companies and traders will “not panic” until we get into the March-May time frame and see whether the drought will expand. We are working on several studies with regards to this, but it is very early and most wheat weather markets do not begin till spring.

Global wheat stocks are significant, with the stocks to usage ratio at about 40%. Normally this means cash wheat prices below $4!! However, the developing drought will “ probably” keep us above $4 in KC July wheat this winter.

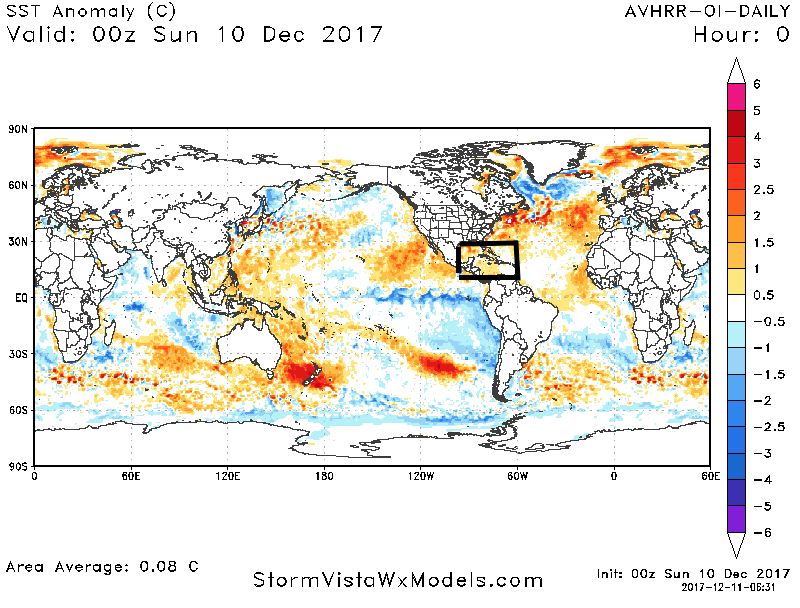

La Nina and WHWP

In the meantime, while most La Nina years would suggest dry weather in Argentina, soybean prices have taken it on the chin again due to a variety of factors. One of them has to do with the dryness in Argentina and southern Brazil being short-lived because of what we call the Western Hemispheric Warm Pool Index. A positive WHWP signal is almost unheard of during a La Nina. As Climatech shows towards the bottom of the page, late last week we issued a “caution flag” potentially increasing our more medium term outlook for Argentina grains to potentially wetter again.

A positive WHWP (box above) signal is almost unheard of during a La Nina . This is one of the few teleconnections that suggest wetter weather for Argentina again.