THE FOLLOWING IS SUBSCRIBER POST FROM FEBRUARY 15, 2024 WEATHERWEALTH MEMBERSHIP

How To Trade Parabolic Commodity Moves, A Potential New Bull Market & Early Season Grain Weather

April 8, 2024

How To Trade Parabolic Commodity Moves, A Potential New Bull Market & Early Season Grain Weather

In this Report:

Introduction

History of some note-worthy supply squeezes and parabolic price moves

The Parabolic SARS indicator

When to sell a Parabolic move

WeatherWealth Trade Ideas & discussion of grain, natural gas, and soft Commodity markets

I will have a video and some weather spiders, if not by Thursday this week, then Sunday night would be my next update.

Introduction:

This report discusses historic parabolic moves.

It is very difficult to judge when mass hysteria often ends in a market. However, usually, hyped-up parabolic prices last for less than 8 months to a year before a major collapse in prices ensues.

This should mean that once La Niña forms, cocoa prices could enter a longer-term bear market deeper in 2024 and/or 2025. However, global cocoa production has to rebound.

I think that Robusta coffee prices could go parabolic if Vietnam’s heat and dryness do not ease by May or June. I also think at some point (not sure of timing) the cocoa market will end its parabolic price rise.

At the bottom of my report, I have various weather maps and market discussions about why wheat prices have rallied, Midwest corn belt weather, and more.

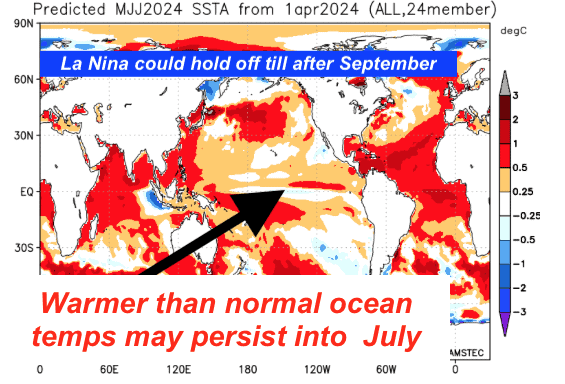

Finally, I think these warm ocean temps may mean that El Nino lasts a bit longer than others feel. This would be potentially bearish corn futures later with decent spring planting and summer weather in the Midwest. Again, it is also potentially bullish coffee.

Enjoy–Jim Roemer

History of some note-worthy supply squeezes and parabolic price moves

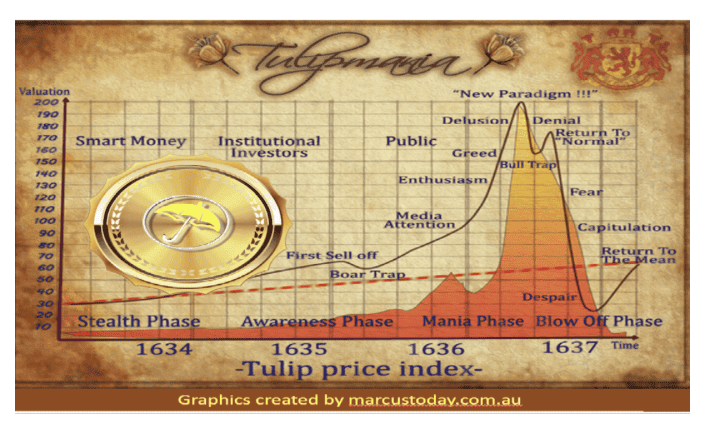

Historic parabolic price moves in commodity markets are not uncommon and have occurred for various reasons, including supply shocks, political turmoil, and speculative bubbles. The Tulip Mania, which crashed in the 1600s, is the first one that has been recorded.

Here are some notable instances over the last 50-100 years:

1. **Oil (1973, 1979, 2008)**: The oil market experienced dramatic price increases during the 1973 OPEC oil embargo and the Iranian Revolution of 1979. As oil production was drastically cut, prices soared, resulting in a severe price spike globally.

2. **Silver (1979-1980)**: Known as the Silver Thursday, the Hunt brothers attempted to corner the silver market, causing prices to skyrocket from around $6 per ounce in early 1979 to a peak of $49.45 per ounce in January 1980. The market collapsed spectacularly afterward.

3. **Gold (1970s and 2000s)**: Gold saw a significant increase in the late 1970s due to high inflation, geopolitical uncertainties, and changes in U.S. monetary policy, peaking at around $850/oz in 1980. Another notable rise happened in the 2000s, culminating in a peak of around $1,900/oz in 2011 amid the financial crisis and subsequent recovery.

4. **Wheat (2007-2008)**: Global wheat prices doubled from 2007 to 2008 due to droughts in major production areas, rising oil prices, and increased demand. This led to food riots and contributed to global economic distress.

5. **Natural Gas (2021)**Leading into the winter of 2021, natural gas prices in Europe and Asia saw unprecedented spikes due to low storage levels, high demand, and supply constraints, exacerbated by geopolitical tensions.

6. **Coffee (Frost of 1975 and 1994)**: Severe frosts in Brazil, the largest coffee producer, have historically led to soaring prices worldwide. The frosts of 1975 and 1994 had a significant impact on supply, leading to a significant increase in prices in a short period of time.

7. **Sugar (1974)**: The global sugar market experienced a historic boom and bust in 1974, with prices rising tenfold in a year due to supply shortages and speculative trading, only to collapse subsequently.

8. **GameStop (2011)**

9. **Bitcoin (2007)**

These examples underscore the volatility inherent in commodity markets, driven by a complex interplay of weather phenomena, geopolitical issues, and market speculations.

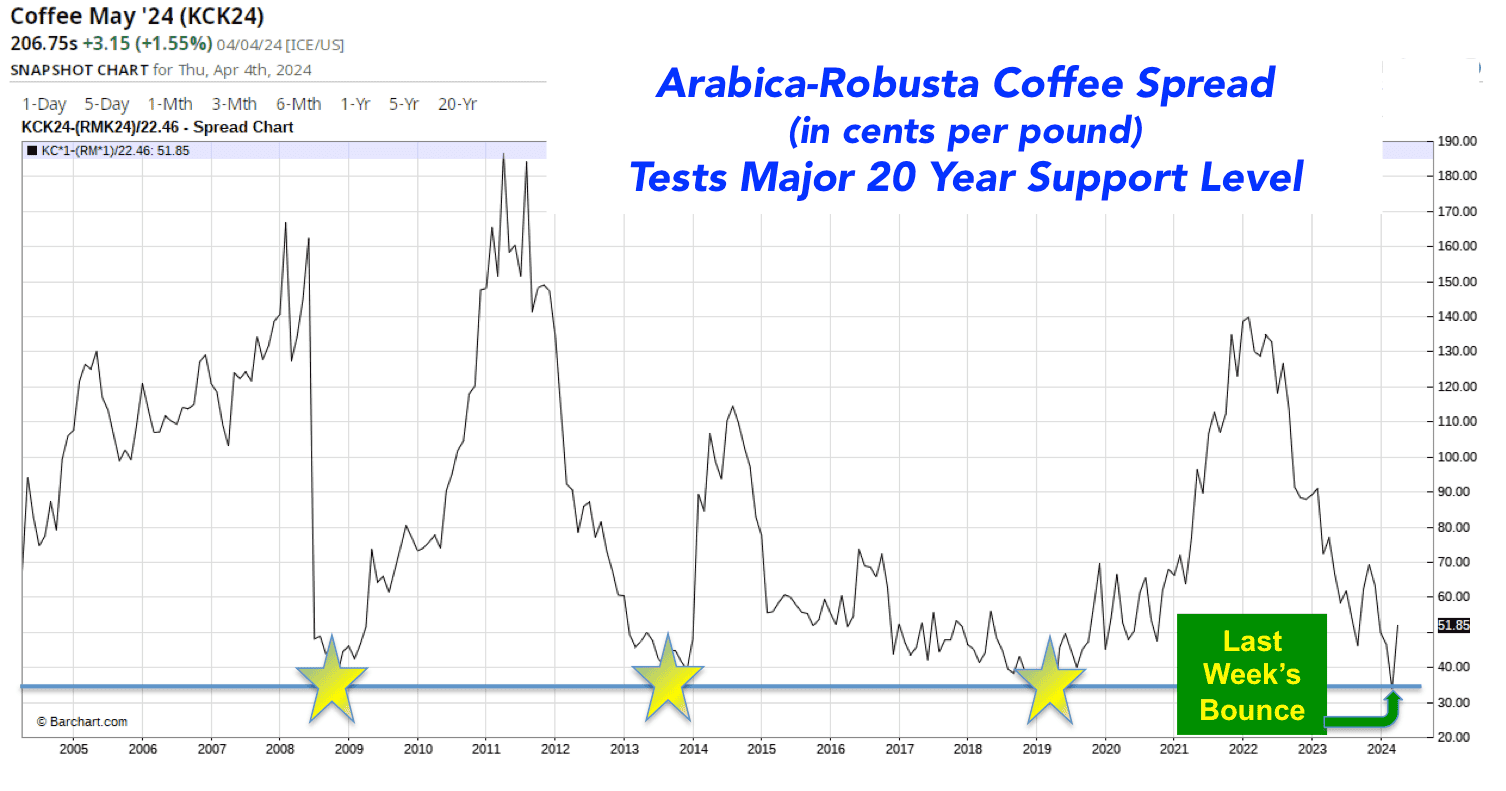

Coffee prices may be moving towards parabolic patterns

Robusta coffee gave up some gains late last week as demand is beginning to shift away from cheap Robusta coffee to higher-quality Arabica beans.

As you can see, the price of Arabica was extremely cheap compared to Robusta coffee, which is likely testing a major support level. Then, that spread bounced the other way. However, weather problems for the Vietnam crop are becoming severe with record heat and low irrigation levels.

BOTTOM LINE: It is possible we are entering into a parabolic price move in Robusta coffee, just like we did in cocoa the last few months. I am unsure at this point whether Arabica coffee prices will continue to gain against Robusta. The bounce-off support late last week may not hold.

What Is the Parabolic SAR Indicator?

- The parabolic SAR indicator, developed by J. Welles Wilder Jr., is used by traders to determine trend direction and potential reversals in price.

- The technical indicator uses a trailing stop and reverse method called “SAR,” or stop and reverse, to identify suitable exit and entry points.

- The parabolic SAR indicator appears on a chart as a series of dots, either above or below an asset’s price, depending on the direction the price is moving. It often follows the 200-day moving average.

In my opinion, the 5-day vs 20-day moving average is a superior indicator.

When to sell a parabolic commodity move?

For me, I need to see a change in the “fundamentals” of the market, ahead of time, to justify entering a short position in a market.

Here are four examples in which the weather or other fundamentals caused a major collapse in commodity prices.

Bottom line: A change in fundamentals and the 5-day moving average going below the 20-day often signal a major trend-change. However, almost all examples of parabolic moves presented in this report lasted for less than 8-12 months. It is possible that (based solely on history) cocoa prices will peak soon and enter a deeper bear market in 2024-2025. This would be especially true if La Niña results in a slight surplus of cocoa next year.

Below are some of the technical indicators to call potential tops in markets. This is extremely sophisticated. Typically, I use fundamental analysis when the 5-day moving average goes above or below the 20-day moving average (see cocoa, below).

- Look for Divergences:

- Examine indicators like RSI, MACD, or momentum indicators for divergences between the price action and the indicator.

- When the price is making new highs but the indicator fails to make a new high, it can signal the parabolic move is losing steam.

- Identify Overextension:

- Use technical tools like Bollinger Bands or standard deviation channels to identify when the price has moved too far, too fast, and is becoming overextended.

- Parabolic moves often reach levels 2-3 standard deviations above the mean, signaling a potential reversal.

- Examine Volume Patterns:

- Look for a sharp drop-off in trading volume as the parabolic move progresses. (This is beginning to occur in cocoa)

- Declining volume can indicate waning enthusiasm and buying pressure to sustain the move higher.

- Apply Fibonacci Retracement Levels:

- Draw Fibonacci retracement levels (23.6%, 38.2%, 61.8%) from the start of the parabolic move.

- One of these common Fibonacci retracement levels is where significant reversals often happen.

- Watch for Blow-Off Tops:

- Identify capitulation-type price spikes with extremely high volume at the end of the parabolic move.

- These “blow-off top” patterns can signal the final exhaustion of buyers before a sharp reversal.

MAY COCOA CHART

Still in a parabolic up-trend though weather should improve in West Africa. I expect a potential bear market later on, but not sure of the exact timing. Right now, we are still in a squeeze situation and the charts are bullish.

WEATHERWEALTH

Trade sentiment—April 10th, 2024

Bullish:

Robusta coffee, crude oil, silver, and gold (I do not make trade recommendations in non-Ag markets, but the charts and fundamentals are positive in these other markets)

Bearish:

Corn, cotton, wheat

Neutral or unsure:

cocoa, natural gas, coffee (neutral to bullish), and sugar

Coffee: Special flash update last Tuesday about global weather problems; then prices soared.

My flash update last Tuesday before the coffee price explosion

If you bought coffee on my flash update early last week, you would be sharply ahead right now, so put stops in. However, I have been more emphatic about being long with Robusta coffee rather than Arabica coffee lately without a specific trade recommendation. This could be the next parabolic bull market

Cocoa: A Wild Market: Tight Supplies Vs Possible Demand Worries and Improved West African Weather.

The mid-crop harvest begins soon. A return of wet weather could cause some minor harvest delays deeper into April, but also be a benefit to the main crop.

Cocoa prices collapsed early last week on spec selling, but it is the “panic” by commercial firms and end users that cannot get enough supply. They are buying on dips.

This market is too volatile to make a new recommendation. Nevertheless, I DO NOT recommend buying this market at these prices, with my potential longer-term bearish bias, later. However, tight global supplies are still bullish in the short-term until the charts change.

Wheat: Worries about Russia’s war on Ukraine and some global crop concerns help prices again

Europe is too wet and dryness may be beginning to hurt the crops in Ukraine and western Russia.

I do see some improvement coming to Europe and Ukraine deeper into April. While Kansas needs more rain, recent moisture should improve crop prospects in Oklahoma and Texas.

Traders may have been stopped out of short July CBOT wheat above $5.80 close only last Friday with a $750-$1,000 loss. I have no interest in recommending buying this market on the weather. I am probably bearish, later. My spider has been cautiously bearish for a month. I think the Plains wheat crop is decent and will improve with time with more rains deeper in April. I would say the chances are 65% that wheat prices will break 10-20% by later this spring or summer.

Soybeans: Weak demand and Brazil harvest pressure hit the market recently

I have no new advice in this market until we get into the North American growing season. My longer-term view probably remains bearish, but it is a long US growing season.

Natural gas: Demand is weak globally, but very low prices may be curtailing U.S. demand.

Despite not making any specific updates to my spider in the past two weeks, the temperature score has been slightly bearish (-1 TO -3) for the most part.

Several times over the last month, I “casually” mentioned my slightly bearish attitude toward natural gas and possibly selling near resistance. Otherwise, I have had no specific advice. However, see my chart and comments, below. The pattern recognition score would go to a +1 or +2 if we get above $2.09 in June natural gas. That would make my total spider score neutral to slightly bullish.

Corn: Ample corn supply and favorable midwest planting weather should limit price rally

My bias will likely turn more bearish corn with a potential move to $3.50 later this summer. I suggest selling out-of-the-money Dec, corn options, or buying puts longer term (small position till we get into the late spring or early summer). Some firms are talking about a summer drought and La Niña, but this is premature and possibly unlikely. The season is just beginning so stay tuned.

Sugar: Slightly lower 2024 crop estimates in India and Thailand cap rallies

I will try to look more closely at this market and the global weather coming up in the next few weeks.

Presently, I have no advice and not watching this market.

Cotton: Technical Break-Down As Chinese Demand Worries And Rains Hitting Texas Hurt Prices

I have no advice in this market, but a previous big long spec position and potential bigger 2024 crops could portend lower prices through summer.

WEATHERWEALTH

With Jim Roemer

2 week free trial

• Weekly global commodity weather and crop outlooks

• Weather Trade of the month recommendation for either coffee, corn, soybeans, natural gas or one other market

• Detailed information on how global weather may affect commodity prices

• Email Jim Roemer (one question a month) about your market position

• Encompassed crop analysis and special weather maps from around the world

• CLIMATE PREDICT long-range weather forecasts used by major hedge funds and commodity traders

• Grain, Soft and Energy Commodities—Know before the crowd where the weather extremes will be