More than 3 months ago, we began predicting a slide in cocoa prices in the $3000/ton area. Prices have since collapsed close to 30% on a variety of factors. While the main impetus in the free-fall in cocoa has been the stronger dollar and worries about Brexit and less European demand and grind data, global weather has been at least as important.

However, given the stocks to usage ratio still at a historically tight level, prices much below these levels for now ($2100) could be difficult in the short term. Most specs have been forced out of the market and the committment of traders is showing the biggest net short position in years. This means that a short covering rally could occur for a while, as at these prices, demand could pick up.

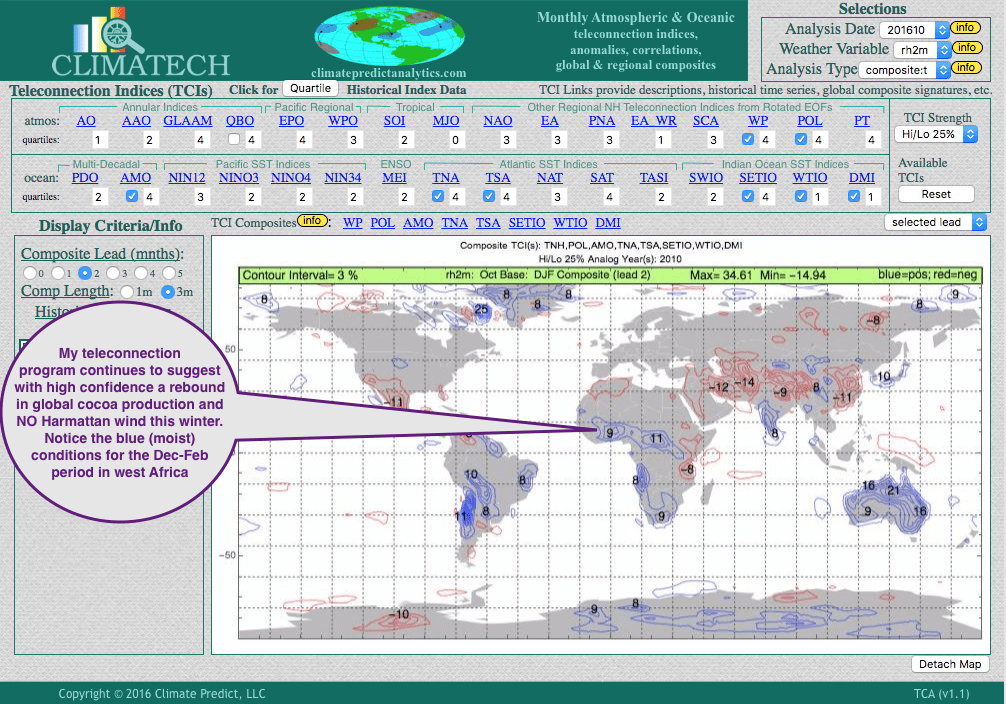

Last summer, we began using our analysts program to predict a healthy end to the west Africa main crop and a good mid-crop. We began forecasting a “rebound” in global cocoa production for this next year and possibly a surplus (not a deficit) in supplies, in contrast to many bullish forecasting out there.

The one saving grace for cocoa prices would be a strong winter west Africa Harmattan. The occasional strong, dusty Sahara wind could sap cocoa trees in winter and lower west African production. This occurred a year or so ago and was partly responsible for the rally in cocoa prices. However, as my Climatech program has been showing for months, these important teleconnections portend above normal rainfall (blue) this winter and a low chance for a Winter Harmattan. You can see how we predicted this back in October, when cocoa prices were 20% higher than where they are now. Hence, any demand related rally at these cheap prices may be met, later this winter and next spring with selling if global weather developments continue ideal.

Climatech has blown away the competition when it comes to forecasting tropical commodities such as cocoa